US INFLATION: MNI US Inflation Insight: Messy And Misleadingly Soft

We've just published our review of the latest US CPI data - Download Full Report Here

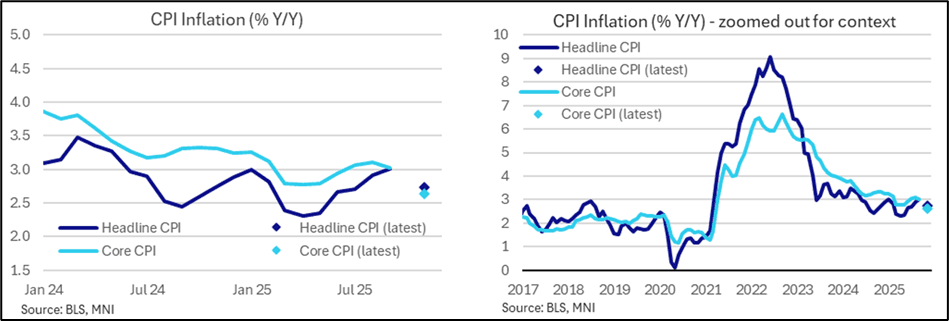

- The November CPI report was even messier than had been feared coming into its delayed release, leaving several lingering questions in its wake.

- On the surface, the inflationary pressures from the report appeared much softer than expected.

- The two-month change in core CPI (Nov vs Sept; the October release was effectively skipped) came in at 0.159% SA, which roughly speaking translates into an 0.08% M/M average for each of Nov and Oct - well below the 0.24% M/M average expected for those two months (and 0.23% M/M in September).

- The average implied monthly change across Oct and Nov for key core CPI items were softer than expected across the board, most notably for housing.

- Headline CPI came in around 0.10% M/M on average in Oct and Nov (2-month rise was 0.20%). Both food and energy inflation softened on an average M/M pace compared with September though dynamics vs expectations varied.

- But the unusual collection period of late November and methodological choices made by BLS appear to have downwardly biased the readings in the report, and look poised to distort readings for months to come.

- This interpretation appears to be borne out by regional Feds’ extremely soft readings across the relevant underlying metrics which were based on the CPI data.

- Fed Chair Powell had warned this month regarding the latest CPI report that “data was not collected in October and half of November. So, we're going to get data, but we're going to have to look at it carefully and with a somewhat skeptical eye.”

- NY Fed President Williams reinforced this notion in downplaying the signal from the data, confrming that the FOMC will interpret these readings with extreme caution, using the December CPI report due out before the January meeting to make more sense of underlying price dynamics.

- Analysts have sharply downwardly revised expectations for core PCE in October and November (and indeed, Y/Y for several months to come) following the CPI report. All acknowledge that the downside surprise to key aggregates was probably driven by serious methodological issues/choices that may reverse to the upside in the coming months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

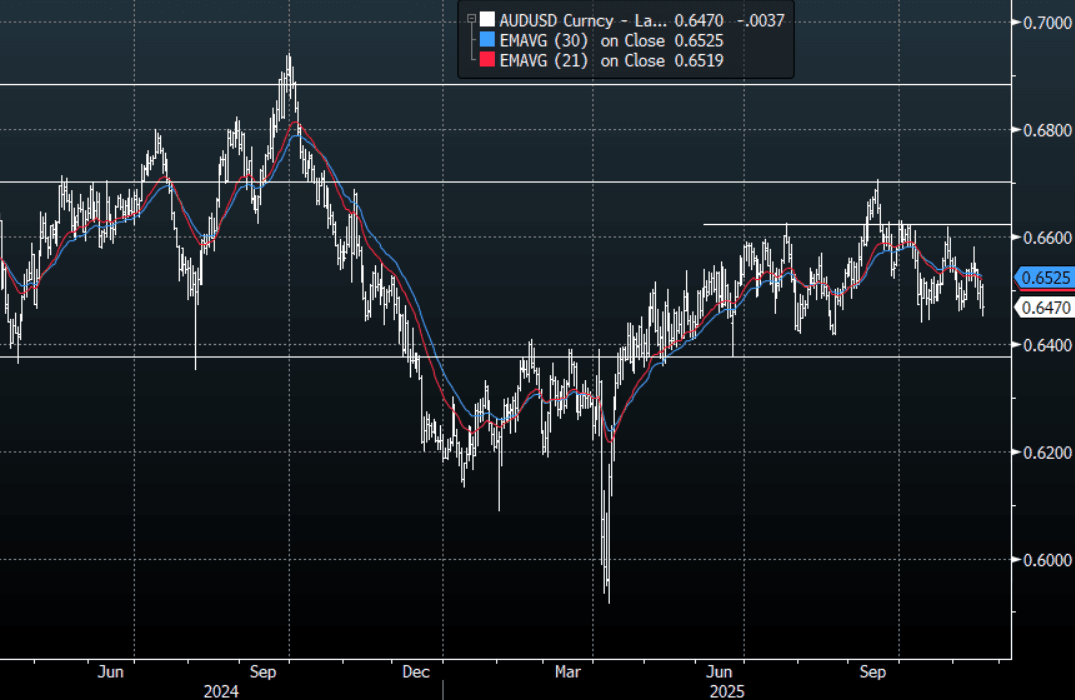

AUD: AUD/USD - Testing 0.6450 Support As USD Breaks Higher

The AUD/USD had a range overnight of 0.6451-0.6497, Asia is trading around 0.6470. Fed members strongly differed on a December cut in the minutes and the BLS said it won’t publish an October jobs report. This has seen the market pull further back on hopes of a December cut and has seen the USD break higher and Crypto have another leg lower. The AUD/USD drifted lower in sympathy and is testing its recent support around the 0.6450 area. The AUD/USD continues to chop around within its wider 0.6350-0.6650 range, the first support is right here around 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think. The market waits for the Nvidia results with bated breath as risk feels like it could rollover if the market does not get the stellar results its looking for,

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD736m), 0.6530 (AUD422m), 0.6550 (AUD739m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 51 Points

- Data/Event: RBA’s Sarah Hunter speaks at the Australia Industry Group in Sydney

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUDUSD TECHS: Bearish Threat

- RES 4: 0.6660 High Sep 18

- RES 3: 0.6644 76.4% retracement of the Sep-Oct bear leg

- RES 2: 0.6618 High Oct 29 and a key near-term resistance

- RES 1: 0.6524/6580 20-day EMA / High Nov 13

- PRICE: 0.6452 @ 17:36 GMT Nov 19

- SUP 1: 0.6452 Low Nov 19

- SUP 2: 0.6440 Low Oct 14 and key support

- SUP 3: 0.6415 Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

Recent weakness in AUDUSD highlights a clear bear threat. This also reinforces a short-term bearish signal on Nov 13 - a shooting star (inverted hammer) candle formation. Note too that moving average studies are in a bear-mode position, highlighting a dominant downtrend. Key short-term pivot resistance has been defined at 0.6580, the Nov 13 high. A continued sell-off would expose 0.6440, the Oct 14 low.

FED: FOMC Minutes: Eyeing More Bills On The Balance Sheeet

One of the least contentious aspects of the October FOMC meeting was on the decision to end QT: "almost all participants noted that it was appropriate to conclude the reduction in the Committee's aggregate securities holdings on December 1 or that they could support such a decision." And even those who didn't quite agree with the decision may be those who thought QT should end immediately rather than a month later (Gov Miran said Wednesday that was his preferred outcome).

- A large portion of the October minutes are devoted to a balance sheet management discussion, beginning with the SOMA manager's recommendation that the FOMC consider stopping runoff "soon" amid "recent changes in money market conditions [that] indicated that the level of reserves could be approaching ample". Participants took that advice to heart: "Participants agreed that the recent tightening in money market conditions indicated that it would soon be appropriate to end balance sheet runoff and that reinvestments of principal payments received on agency securities holdings should be directed into Treasury bills."

- We note for future reference that the SOMA manager eyed repo vs IORB and EFFR vs IORB spreads, and some of the peripheral indicators previously flagged by the NY Fed including a rising share of domestic banks borrowing in the Fed funds market, and rising elasticity of repo rates to changes in repo volumes.

- They discussed the future profile of the Fed balance sheet too, and unsurprisingly a majority wanted the composition to reflect Treasuries outstanding, with a majority wanting to see a larger share of Treasury bills than the current miniscule portion - with a notable minority wanting a relatively large TBill proportion: "Most participants favored a long-run composition of the SOMA portfolio that matched the composition of Treasury securities outstanding, indicating that a proportional allocation would provide enough flexibility and may be simpler to communicate. Some participants indicated that they favored a larger-than-proportional share of Treasury bills, citing the benefits of having even greater flexibility than available under a proportional allocation. Various participants noted that it was not necessary to decide on the long-run composition of the SOMA portfolio at this time, as the shift toward a long-run composition would take place over a number of years."

- On that note, "The presentation noted that the current share of Treasury bills in the SOMA portfolio was smaller than the bill share of total Treasury securities outstanding. The staff also noted that if the Committee preferred a SOMA portfolio with a proportional or greater share of Treasury bills relative to total outstanding, policymakers could wait to make that decision because the current share of Treasury bills in the portfolio was small and the monthly amounts of principal payments received on the Federal Reserve's holdings of agency securities that would need to be reinvested once balance sheet runoff stopped were modest."

- And there didn't seem to be too much opposition to buying bills in future: "Some participants indicated that during a transition phase, purchases to reach a larger share of Treasury bills in the SOMA portfolio could reduce the availability of short-term Treasury securities to the private sector and potentially affect market functioning. They thus favored a measured approach to purchasing Treasury bills. A couple of other participants noted the absence of market functioning problems in past episodes when purchases focused on Treasury bills. A number of participants noted that the expected pace of paydowns of agency securities in the near term was around only $15 billion to $20 billion per month, and that redirecting these proceeds into Treasury bills once balance sheet runoff ended likely would not adversely affect market functioning."

- Elsewhere, the FOMC discussed the Standing Repo Facility in fairly noncommittal fashion, with several looking to study central clearing more closely (" almost all noted that the SRF supports the effective implementation and transmission of monetary policy as well as smooth market functioning, and that central clearing of SRF transactions could improve the effectiveness of the facility").