SECURITY: US Secretary Of State Rubio Talks On Ukraine, Venezuela & Gaza

Secretary of State Marco Rubio speaking at an end-of-year press conference (livestream).

- Regarding the state of talks on a Ukraine-Russia peace plan framework, Rubio claims that "We've made progress but we have a ways to go," adding that "Talks to end the Ukraine war are not about imposing a deal on anybody." Rubio: "What we're trying to figure out is what can Ukraine live with and what can Russia live with...Wars end one of two ways. Surrender by one side to another or a negotiated settlement. We don't see surrender by either side...Only a negotiated settlement gives us the opportunity to end this war."

- On Venezuela: "One place that doesn't cooperate [on drug control]. The illegitimate regime in Venezuela. They ultimately cooperate with terrorists and criminal elements. Invite Hezbollah and Iran to operate from their territory, and the dissidents not just to operate inside but to control Venezuelan territory unimpeded."

- Asked by a reporter about the International Stabilisation Force that is due to act as a peacekeeping force in Gaza, Rubio says "I think we owe [potential contributors] a few more answers before we can ask anybody to firmly commit. But I feel very confident that we have a number of nation-states acceptable to all sides in this conflict who are willing to step forward and be a part of that stabilisation force..." On the US-mediated Lebanese/Israeli talks: "We are hopeful the talks create outlines and a way forward that prevents further conflict."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: FOMC Minutes Preview: QT, IORB Tweak, Reserve Management Purchases (3/3)

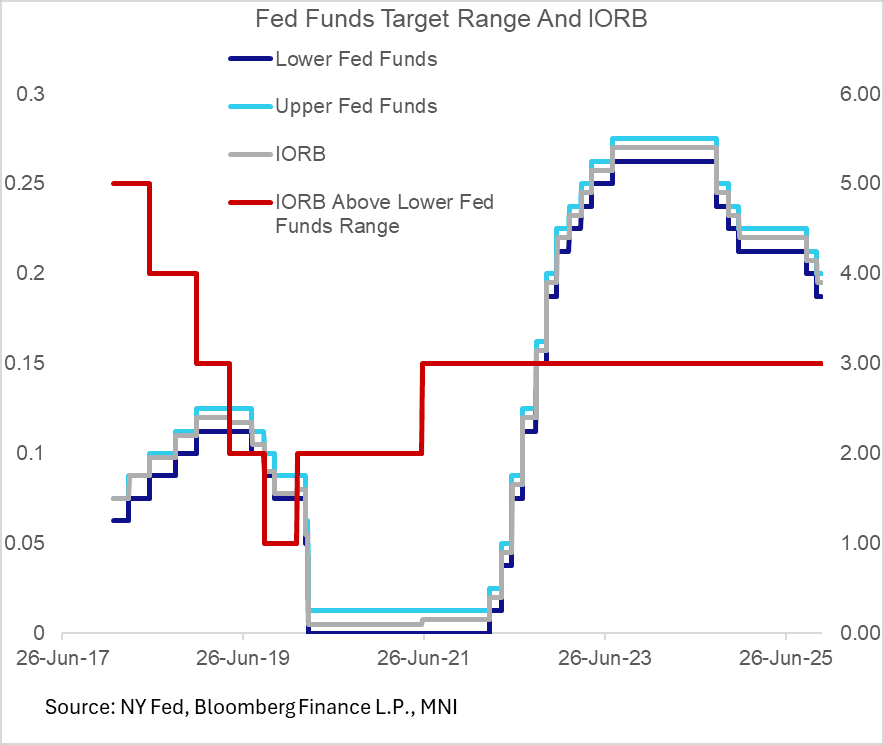

Outside of the debate over the path of policy rates in the Minutes, we will be eyeing the discussion around balance sheet and rate management given the meeting's decision to end QT effective December 1.

- While that decision wasn’t a major surprise, we will be watching in particular whether there was mention of potential timing to start reserve management purchases, or lower the administered IORB rate within the Fed funds range in response to funding rate pressures evident in October.

- There is increasing speculation that IORB could be lowered as soon as the December meeting, while reserve management purchases (probably in bills) are expected to start in the first half of 2026 as the Fed rebuilds its balance sheet to meet the underlying growth in liability demand.

- The Fed has lowered interest on reserve balances (now called IORB, previously referred to as IOER) relative to the Funds range in previous episodes as it navigated a pullback in reserves. The FOMC ratcheted the administered rate lower by 5bp relative to the policy rate in each of June and Dec 2018, and May and Sep 2019, from 25bp above the lower bound to just 5bp above it, before increasing it again in 2020-21 back to 15bp.

- The FOMC may well have discussed this last month: KC Fed Pres Schmid last week mentioned lowering IORB, a technical adjustment which would see repo rates fall and in theory allow the Fed to hold fewer reserves than it otherwise would: "Another possible action could be to lower the interest rate that the Fed pays on reserves within the target band. Currently this rate is 15 basis points above the bottom of the band. Lowering the rate within the band would allow more space for other interest rates to move before bumping up against the top of the band. This would allow for a greater range of private intermediation of reserve demand before the Fed would feel the need to take action."

US STOCKS: Midday Equities Roundup: Mostly Higher

- Major US equity indexes are mostly higher Wednesday, off early session highs with focus on this afternoon's Q3 earnings for Nvidia, not to mention the October FOMC minutes release that may be sidelining traders ahead midday.

- Currently, the DJIA trades down 133.06 points (-0.29%) at 45959.84, S&P E-Minis up 7.5 points (0.11%) at 6648, Nasdaq up 103.4 points (0.5%) at 22537.29.

- Communication Services and Information Technology sector shares led advances in the first half, media & entertainment stocks buoyed the former: Alphabet +4.45%, TKO Group Holdings +1.89%, Warner Bros Discovery +1.03% and Fox +0.67%.

- Supporting tech sector shares: Lam Research +3.68%, ON Semiconductor +3.34%, Broadcom +3.33%, Seagate Technology +2.99%, Teradyne +2.93%, Applied Materials +2.79% and NVIDIA +2.40%.

- Conversely, Energy and Consumer Staples sector shares led declines by midday, a drop in crude prices (WTI -1.37 at 59.37) weighing on oil and gas stocks: APA Corp -3.99%, Valero Energy -3.41%, Marathon Petroleum -3.15%, Phillips 66 -3.09%, ConocoPhillips -2.32% and Occidental Petroleum -2.23%.

- Meanwhile, broadline retailers weighed on the Consumer Staples sector: Dollar General -2.68%, Costco Wholesale -2.08%, Archer-Daniels-Midland -1.90% and Molson Coors Beverage -1.55%.

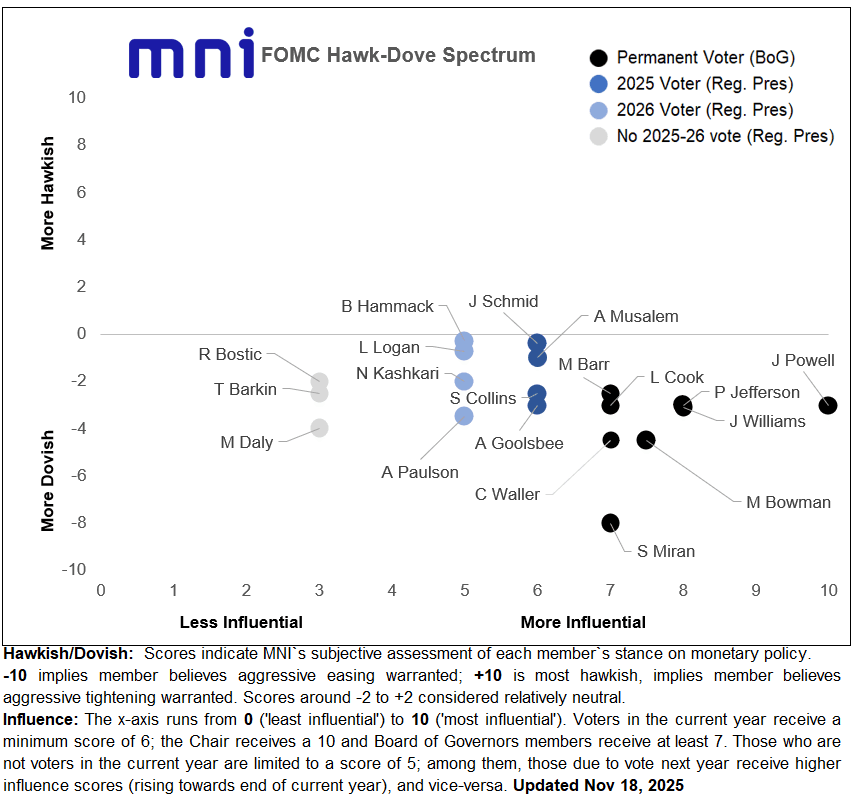

FED: FOMC Minutes Preview: Participants Lean Hold, Voters Lean Cut (2/3)

We now see 10 (of 19) members who would go into the December meeting supportive of a hold to varying degrees. In terms of the 12 voters, though, we think it’s currently 7-5 in terms of favoring a cut, with a core bloc of 4 members including Chair Powell set to sway the Committee in one direction or another. Coming out of the September meeting, there was a fine division between the number of participants who saw 3 or more cuts (10 of 19) and those who saw 2 or fewer (9) in their Dot Plot submissions. That overall division has persisted, but it sounds to us as though the relative hawks now slightly outnumber the doves.

- There are now at least two current voters – Boston’s Collins and KC's Schmid - who could outright oppose a follow-up easing in December. It would not surprise us if their fellow regional Fed voters, Chicago’s Goolsbee and St Louis’s Musalem, were to resist another cut.

- While Collins had previously sounded as though she could increasingly resist a December cut, her inter-meeting comment that “it will likely be appropriate to keep policy rates at the current level for some time” brought one of the most hawkish market reactions. Kashkari has had the most surprising shift overall, going from a 3-cuts-in-2025 proponent just after the September meeting, to opposing cuts in Oct and Dec.

We would categorize the current state of play as:

- 6 Definite December holders: We have heard explicitly from Cleveland’s Hammack, Dallas’s Logan, Schmid (voter), Collins (voter), Kashkari, and Atlanta’s Bostic that they would prefer to hold rates in December and/or indefinitely.

- 4 Likely leaning hold: Gov Barr (voter), Musalem (voter), and Richmond’s Barkin have sounded consistently patient on the cutting front to varying degrees. To our ear, Goolsbee (voter) sounds like he is in favor of a “dovish hold” (signalling further cuts in 2026 while taking a break in December) having expressed increasing concerns over inflation and set a higher bar to a December cut than the one he supported in October though we do acknowledge he’s very much on the fence and could end up going with an eventual majority that votes for a cut.

- 3 Definite December cutters, all voters: Gov Waller (voter) has reiterated the case for further easing, with Gov Miran (voter) continuing to argue for 50bp cuts; we have no reason to think Gov Bowman (voter) has changed her mind on the need for more easing.

- 2 Likely December cutters: SF’s Daly and Philadelphia’s Paulson (no commentary since October FOMC) have previously expressed support for Sep/Oct/Dec cuts and we have no reason to think they’ve changed their minds.

- 4 permanent members in a Bloc lean to a cut: We haven’t heard at all from Chair Powell since the October meeting, but we think that he, Cook, Jefferson, and Williams will vote as a bloc. Right now we would guess all of these permanent FOMC voters would support a cut.