MNI US MARKETS ANALYSIS - Tsys Tilted Back Toward CPI Highs

Highlights:

- Treasuries tilted back toward CPI highs

- USD Index through support, GBP/USD narrowing in on key resistance

- Data schedule is light, keeping focus on suite of Fed speakers

US TSYS: Back Close To Post-CPI Highs, Fedspeak and Trump Watched

- Treasuries have steadily firmed throughout London hours as they push back towards post-CPI highs, reversing the EGB-led post-data retracement that was hard to square away at the time.

- Treasuries underperform EGBs but outperform Gilts.

- Today sees focus on further FOMC reaction to yesterday’s CPI release whilst Trump headlines can as always have an impact, especially with such a light data calendar today.

- Trump makes an announcement at The Kennedy Center at 1115ET, which we believe should be focused on announcing Honors recipients but we’ll monitor for any surprises.

- Cash yields are 2.5-4bp lower, with the front end lagging declines.

- The modest flattening sees curves ease away from post-CPI steeps. That includes 5s30s at 105.4bps (-0.4bp) after yesterday’s 107.6bps came close to ytd highs of 108.5bps.

- TYU5 has lifted to 112-02 (+ 08) at typing but remains within yesterday’s CPI-induced range of 111-19+ to 112-06. Cumulative volumes are higher than recent overnight sessions but still limited at 250k.

- The contracts hold its ground from a technical perspective, with resistance at 112-15+ (Aug 4/5 high depending on timezone) and support at 110-10+ (Jul 24 low).

- Data: MBA mortgage applications (0700ET).

- Fedspeak: Barkin (0800ET), Goolsbee (1300ET) and Bostic (1330ET) – see STIR bullet

- Bill issuance: US Tsy to sell $65B 17-W bills (1130ET)

- Politics: Trump visits The Kennedy Center and makes announcement (1115ET), Trump signs executive orders (1600ET)

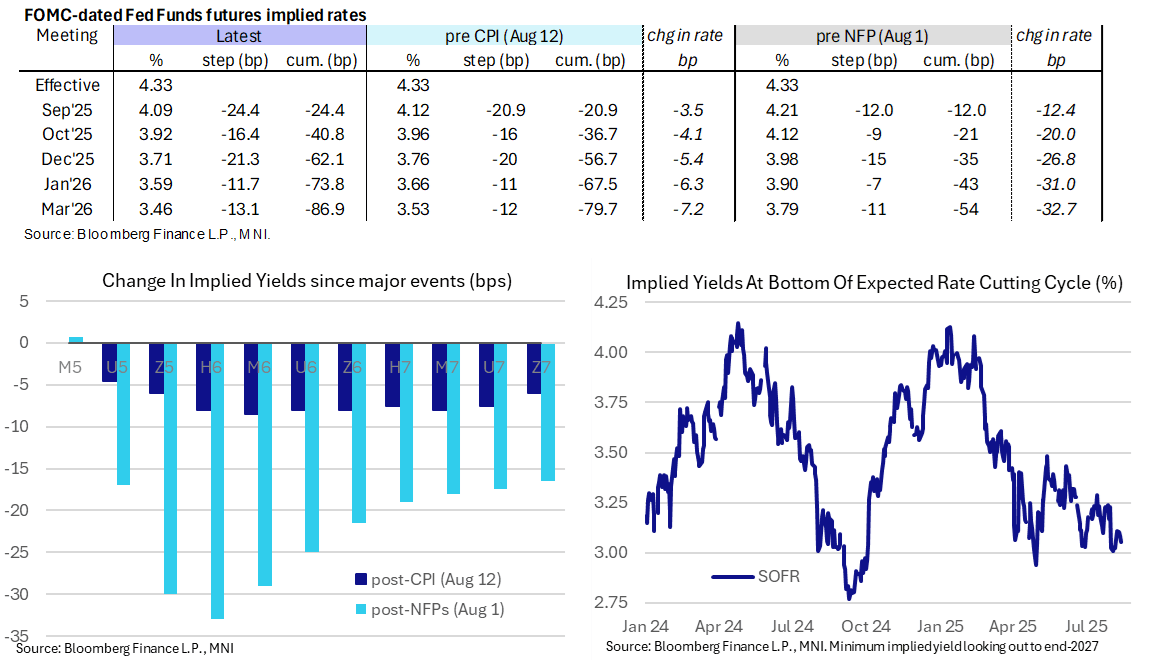

STIR: Fed Rate Path Split Between Two and Three Cuts For 2025

- Fed Funds implied rates are unchanged on the day for the September meeting after yesterday’s CPI report (25bp cut essentially fully priced) but are up to 2.5bp lower out to 1Q26 amidst a broader FI rally.

- Cumulative cuts from 4.33% effective: 24.5bp Sep, 41bp Oct, 62bp Dec, 74bp Jan and 87bp Mar.

- The 62bp for the year compares with 56.5bp pre-CPI and 35 pre-NFP. The now outdated June SEP median had 50bp of cuts with seven members looking for no cuts at all.

- The SOFR implied yield of 3.055% (SFRH7) is 3bp lower on the day, back to fully pricing five cuts for the cycle.

- Bessent late yesterday suggested the Fed ought to be open to a 50bp rate cut next month. The Fed “could have been cutting in June, July” had it had the revised [payrolls] figures in hand at the time. He said the CPI report showcased that economists had misread the likely effect of tariffs.

- Analysts continue to shift towards market pricing for the September FOMC, with Nomura and TD Securities yesterday joining a sizeable list of those now looking for a 25bp cut next month.

- Today's scheduled Fedspeak sees Goolsbee and Bostic in focus:

- 0800ET - Barkin (non-voter) repeats a speech on the economy. Subsequent Q&A might be watched but unlikely to say anything new - he said yesterday the "balance" between dual mandate variables is "still unclear".

- 1300ET - Goolsbee ('25 voter, dove) speaks at a monetary policy luncheon. It's been an unusually long time since Goolsbee last spoke, on Jul 11 saying that he has seen "surprisingly little" impact from tariffs but that new tariff threats (at the time) could delay rate cuts.

- 1330ET - Bostic (non-voter) speaks on the economic outlook (Q&A only). This should be a useful update from Bostic, who said after the July nonfarm payrolls report that he still saw only one rate cut this year. He wants to see how things evolve over the coming months and warned that it might take twelve months for businesses to adjust their prices.

US OUTLOOK/OPINION: Core PCE Estimates Ease To 0.25% M/M For July

- Yesterday’s CPI report has seen core PCE estimates for July center on 0.25% M/M (across eight analysts) vs a tentative 0.31% M/M prior to CPI (across five analysts).

- It implies a very similar pace to the 0.26% M/M in latest data for June and would see the Y/Y firm to 2.87% for its fastest since February.

- There’s a relatively narrow range of 0.22-0.28% considering PPI is still to come tomorrow.

- Wells Fargo: 0.22%

- JPM: 0.24%

- Nomura: 0.24% (vs 0.33 pre-CPI)

- NWM: 0.24%

- TDS: 0.25%

- UBS: 0.25% (vs 0.33 pre-CPI)

- GS: 0.26% (vs 0.31 pre-CPI)

- BofA: 0.28%

US TSY FUTURES: Mix Of Positioning Swings Seen Tuesday

OI data points to a mix of net short cover (TU), long setting (FV), short setting (TY & WN) and long cover (UXY & US) as the curve twist steepened on Tuesday.

- There was a very modest bias towards cover in DV01 equivalent terms, although positioning swings on both the curve and within individual contracts were contained.

| 12-Aug-25 | 11-Aug-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,510,070 | 4,560,629 | -50,559 | -1,856,120 |

FV | 7,056,967 | 7,019,753 | +37,214 | +1,592,387 |

TY | 5,226,061 | 5,205,642 | +20,419 | +1,351,125 |

UXY | 2,458,179 | 2,465,186 | -7,007 | -615,355 |

US | 1,765,899 | 1,774,368 | -8,469 | -1,188,285 |

WN | 2,005,682 | 2,001,889 | +3,793 | +695,636 |

|

| Total | -4,609 | -20,611 |

SOFR: Positions In Futures Built On Tuesday, Fly Activity Noted

OI data points to fresh positions being added across much of the SOFR futures strip on Tuesday, with net long setting dominating through SFRU7, before net short setting moved to the fore from SFRH8 as the strip twist steepened.

- The biggest net OI swing came in the SFRM7 contract, boosted by turnover in the SFRZ6/M7/Z7 fly, which saw ~55K lots trade on the session (dominated by selling of the structure).

| 12-Aug-25 | 11-Aug-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,207,638 | 1,212,400 | -4,762 | Whites | +45,580 |

SFRU5 | 1,289,070 | 1,263,172 | +25,898 | Reds | +96,526 |

SFRZ5 | 1,379,475 | 1,369,756 | +9,719 | Greens | +197,924 |

SFRH6 | 1,048,865 | 1,034,140 | +14,725 | Blues | +8,133 |

SFRM6 | 902,484 | 879,824 | +22,660 |

|

|

SFRU6 | 887,145 | 878,066 | +9,079 |

|

|

SFRZ6 | 1,008,205 | 963,204 | +45,001 |

|

|

SFRH7 | 742,222 | 722,436 | +19,786 |

|

|

SFRM7 | 932,061 | 818,075 | +113,986 |

|

|

SFRU7 | 584,935 | 575,220 | +9,715 |

|

|

SFRZ7 | 577,909 | 517,765 | +60,144 |

|

|

SFRH8 | 343,794 | 329,715 | +14,079 |

|

|

SFRM8 | 272,917 | 267,105 | +5,812 |

|

|

SFRU8 | 206,036 | 207,858 | -1,822 |

|

|

SFRZ8 | 223,373 | 219,403 | +3,970 |

|

|

SFRH9 | 152,276 | 152,103 | +173 |

|

|

EUROPE ISSUANCE UPDATE

German auction results

- The latest Bund auction was on the weaker side, extending the recent theme.

- The 1.44x bid-to-cover represented a marginal deterioration from the already soft 1.49x seen at the prior offering of the 2.60% Aug-35 Bund.

- However, the lowest accepted price of 99.20 comfortably topped 99.163 pre-auction mid.

- The line saw some incremental cheapening in immediate reaction to the auction, but the solid enough pricing side of the auction limited that move, with yields back to pre-auction levels soon after.

- E5bln (E3.885bln allotted) of the 2.60% Aug-35 Bund. Avg yield 2.69% (bid-to-offer 1.12x; bid-to-cover 1.44x).

FOREX: Greenback Through Support, GBP Still Primary Beneficiary

- The greenback is softer against all others in G10, prompting the USD Index to fall for a second session. The price is now through last week's lows of 97.945 further erasing the rally posted off the late July low. Yesterday's CPI print remains the primary driver here, as the data cleared the last hurdle to the Fed resuming an easing cycle from September. OIS markets are now effectively fully priced for a cut, with more than another 25bps cut set to follow before year-end.

- The resultant USD weakness has aided recent rallies in the major pairs. GBP remains a key beneficiary here as the recent hawkish shift at the BoE further contrasts with the Fed. GBP/USD is now cleared of the 50-dma and appears to be building a base toward 1.3589, the mid-July highs. Clearance here would further firm the S/T outlook and keeps the YTD cycle highs in consideration across the medium-term - last traded back at 1.3789 on July 1st.

- EUR/NZD trades under pressure, with NZD outperformance across the board. The cross is fading off the monthly August of 1.9680. Further weakness through 1.9525 would be a bearish signal, and go further in erasing the rally posted at the beginning of this month. Moves come ahead of the RBNZ rate decision set for next week, with a further 25bps rate cut largely expected.

- Focus for the duration of the session remains on the speaker schedule, with data releases sparse. Fed's Barkin, Goolsbee and Bostic are all set to speak - with markets looking to complete the expected layout of votes into September after Fed nominee Miran spoke earlier this week.

CEE FX: USD/CE3 Pairs Targeting Fresh Multi-Year Lows Amid Broad Dollar Weakness

The USD Index has fallen for a second consecutive session, prompting USD/CE3 pairs to extend recent pullbacks. Yesterday's CPI print remains the primary driver for the greenback, as the data cleared the last hurdle to the Fed resuming an easing cycle from September. OIS markets are now effectively fully priced for a cut, with more than another 25bps cut set to follow before year-end.

- USDHUF is trading just above July’s 2-year low at 336.64, a break of which would resume the bearish price sequence of lower-lows and lower-highs, signalling scope for an extension lower towards the 2023 low at 331.45. A break of this level would put spot at its lowest since April 2022.

- Meanwhile, USDPLN has now pared the bulk of the late-July rally. The July 1 low at 3.5844 marks key support, and a break would put the pair at a new 7-year low. Similarly, USDCZK is probing the July multi-year low at typing.

GBP/USD Set to Test Key Resistance

Latest stretch higher in GBP is putting GBP/USD on course for a test of the major resistance we've flagged at 1.3589: clearance here puts prices at the highest since mid-July fully reverses the fade into the early August lows.

- GBP has been the primary beneficiary of the USD-led weakness in recent weakness - with the contrast between BoE and Fed policy cemented on the hawkish BoE cut last week, limiting the pricing of UK rate cuts into year-end, and through to the Autumn Budget - the next major macro event in the medium-term (likely late October/early November).

- Growth numbers due tomorrow are expected to show a sharp slowing in quarterly growth to 0.1% from 0.7% in the prior quarter - but an upside surprise here would catalyse a move north of the current range and extend the spell of not-as-bad-as-feared UK economic data.

- The downtick in front-end implied GBP vols coincides with improving net risk reversals - likely implying a cheapening of put vol that covers both the Sept and Nov MPC, priced for a cumulative 11bps of cuts across both meetings.

- On GBP, Rabobank write that they see GBP's recent better tone running out of steam, with the BoE cutting in November - with this week's growth data possibly confirming stagflationary fears.

OPTIONS: Expiries for Aug13 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-20(E3.2bln), $1.1570-80(E1.1bln), $1.1600(E851mln), $1.1650(E693mln), $1.1700(E1.3bln)

- USD/JPY: Y146.75-85($1.4bln), Y147.00($1.1bln), Y147.40-50($515mln) Y150.25($1.5bln);

- AUD/USD: $0.6550(A$597mln), $0.6575(A$646mln)

- USD/CAD: C$1.3725($555mln), C$1.3835-55($724mln)

EQUITIES: E-Mini S&P Trading at Fresh Cycle High

- The bounce off post-NFP lows in global equity indices has held, with the Eurostoxx 50 future still above the 50-day EMA. Additional strength refocuses attention on 5486.00, the May 20 high. To the downside, recent impulsive weakness did result in a temporary breach of the bear trigger - this makes the April 30 hi/lo range at 5078-5138 the area of downside interest.

- E-mini S&P prices recovered well Friday, meaning the bulk of the bounce off the NFP low is holding firm, keeping the underlying uptrend intact. The index holds above support at the 20-day EMA, at 6371.43 and is at a fresh cycle high. Through recent phases of weakness, the 50-day EMA at 6249.46, has held as support - and will be important on any intraday declines. Clearance of this average is required to signal a stronger reversal. The primary trend remains up, leaving key short-term resistance and the bull trigger at 6468.50, the Jul 31 high.

COMMODITIES: WTI Futures Remain Weak After Break of Bear Trigger

- WTI futures traded poorly Friday, cracking the 50-day EMA and piercing the bear trigger. This keeps S/T momentum pointed lower. The clear break exposes $58.17, the May 30 low. Gains early last week marked an extension of a corrective cycle - which may now have concluded. $69.41 marks the 50.0% retracement of the Jun 23-24 downleg - an important level. A continuation higher would open $70.96 next, the 61.8% retracement point.

- Gold traded lower at the start of the week, but last week's strength returned prices toward the top-end of the recent range and supports the view that short-term weakness is corrective - for now - and a bull cycle that started Jun 30 remains intact. However, the yellow metal is within close proximity to support at $3334.75, the 50-day EMA. A clear break of this level continues to signal scope for a deeper retracement and exposes the next key support at $3248.7, the Jun 30 low. Key near-term resistance is $3439.0, the Jul 23 high.

| Date | GMT/Local | Impact | Country | Event |

| 13/08/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 13/08/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 13/08/2025 | 1700/1300 | Chicago Fed's Austan Goolsbee | ||

| 13/08/2025 | 1730/1330 | Atlanta Fed's Raphael Bostic | ||

| 14/08/2025 | - | NorgesBank Meeting | ||

| 14/08/2025 | 0130/1130 | *** | Labor Force Survey | |

| 14/08/2025 | 0600/0700 | *** | UK Monthly GDP | |

| 14/08/2025 | 0600/0800 | *** | Final Inflation Report | |

| 14/08/2025 | 0600/0700 | ** | Trade Balance | |

| 14/08/2025 | 0600/0700 | ** | Index of Services | |

| 14/08/2025 | 0600/0700 | ** | Index of Production | |

| 14/08/2025 | 0600/0700 | ** | Output in the Construction Industry | |

| 14/08/2025 | 0600/0700 | *** | GDP First Estimate | |

| 14/08/2025 | 0645/0845 | *** | HICP (f) | |

| 14/08/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 14/08/2025 | 0900/1100 | ** | Industrial Production | |

| 14/08/2025 | 0900/1100 | *** | GDP (p) | |

| 14/08/2025 | 0900/1100 | * | Employment | |

| 14/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 14/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 14/08/2025 | 1230/0830 | *** | PPI | |

| 14/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 14/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 14/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 14/08/2025 | 1800/1400 | Richmond Fed's Tom Barkin |