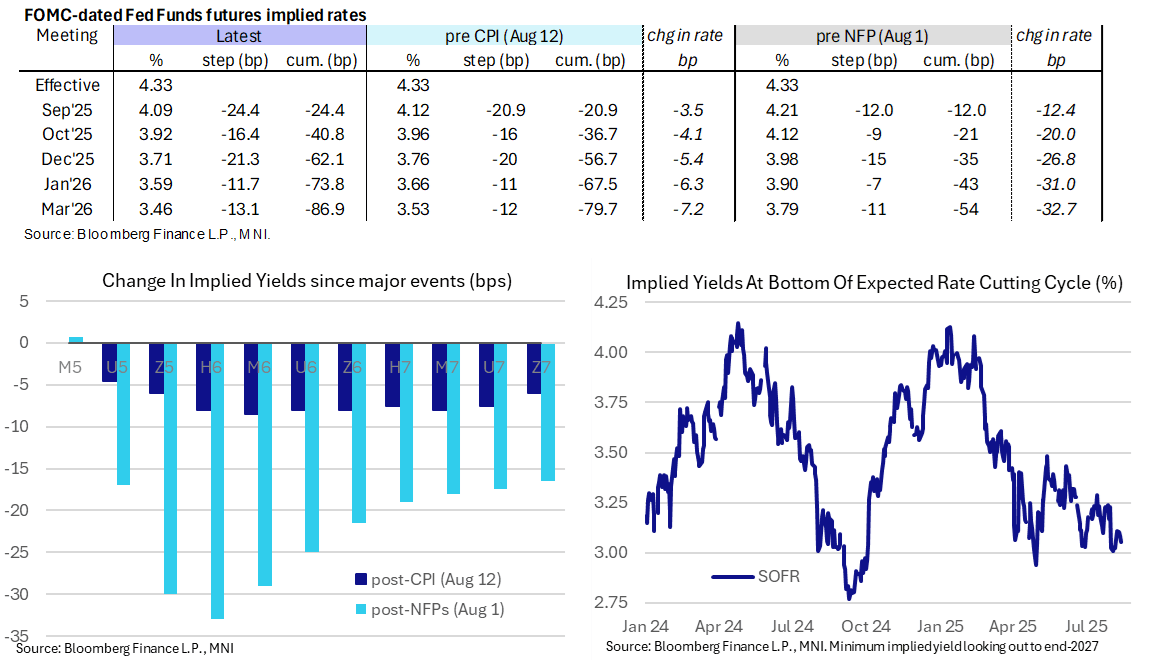

STIR: Fed Rate Path Split Between Two and Three Cuts For 2025

Aug-13 10:37

- Fed Funds implied rates are unchanged on the day for the September meeting after yesterday’s CPI report (25bp cut essentially fully priced) but are up to 2.5bp lower out to 1Q26 amidst a broader FI rally.

- Cumulative cuts from 4.33% effective: 24.5bp Sep, 41bp Oct, 62bp Dec, 74bp Jan and 87bp Mar.

- The 62bp for the year compares with 56.5bp pre-CPI and 35 pre-NFP. The now outdated June SEP median had 50bp of cuts with seven members looking for no cuts at all.

- The SOFR implied yield of 3.055% (SFRH7) is 3bp lower on the day, back to fully pricing five cuts for the cycle.

- Bessent late yesterday suggested the Fed ought to be open to a 50bp rate cut next month. The Fed “could have been cutting in June, July” had it had the revised [payrolls] figures in hand at the time. He said the CPI report showcased that economists had misread the likely effect of tariffs.

- Analysts continue to shift towards market pricing for the September FOMC, with Nomura and TD Securities yesterday joining a sizeable list of those now looking for a 25bp cut next month.

- Today's scheduled Fedspeak sees Goolsbee and Bostic in focus:

- 0800ET - Barkin (non-voter) repeats a speech on the economy. Subsequent Q&A might be watched but unlikely to say anything new - he said yesterday the "balance" between dual mandate variables is "still unclear".

- 1300ET - Goolsbee ('25 voter, dove) speaks at a monetary policy luncheon. It's been an unusually long time since Goolsbee last spoke, on Jul 11 saying that he has seen "surprisingly little" impact from tariffs but that new tariff threats (at the time) could delay rate cuts.

- 1330ET - Bostic (non-voter) speaks on the economic outlook (Q&A only). This should be a useful update from Bostic, who said after the July nonfarm payrolls report that he still saw only one rate cut this year. He wants to see how things evolve over the coming months and warned that it might take twelve months for businesses to adjust their prices.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

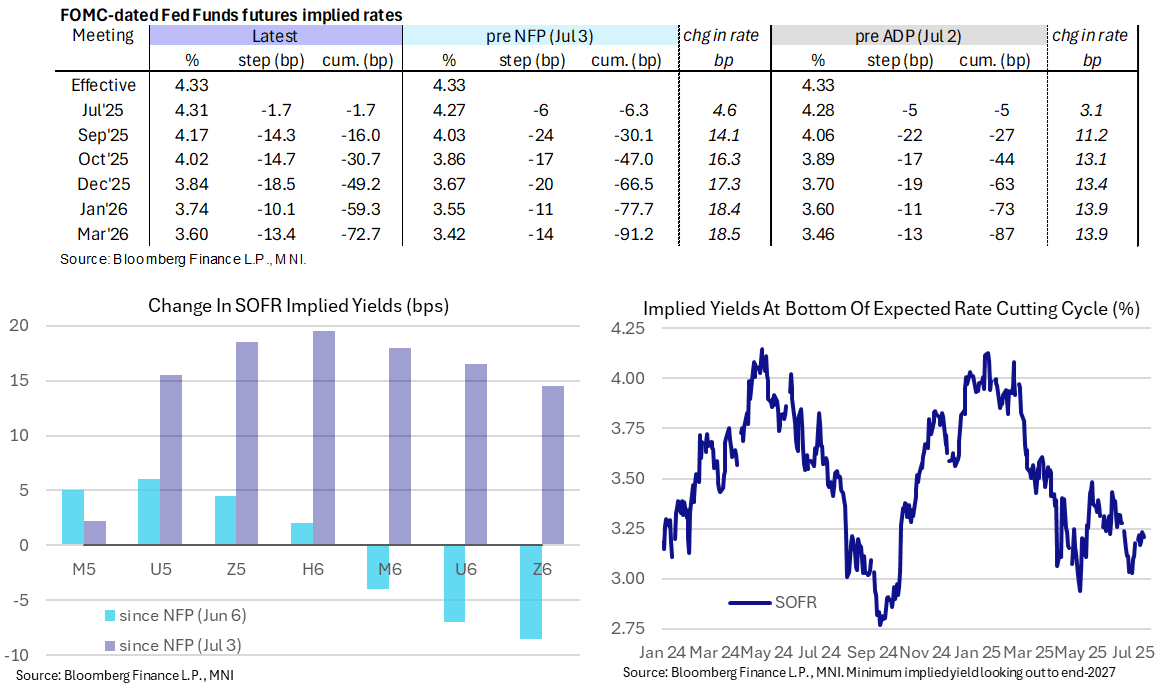

STIR: Least Conviction On Sept FOMC Cut In A Month

Jul-14 10:33

- Fed Funds implied rates are up to 1.5bp higher from Friday’s close for near-term meetings after President Trump’s weekend threats of 30% tariffs on the EU (the largest source of US imports) ahead of a Aug 1 deadline.

- Trump talking up an upcoming “Major Statement” on Russia has also supported oil futures.

- Increases in implied rates are quickly limited further out the curve owing to the associated growth concerns, with the Mar 2026 rate just 0.5bp higher for example.

- Cumulative cuts from 4.33% effective: 1.5bp Jul, 16bp Sep, 30.5bp Oct, 49bp Dec, 59bp Jan and 73bp Mar.

- Similarly, SOFR futures trade flat to 3 ticks firmer on the day.

- The SOFR implied terminal yield of 3.21% (SFRZ6, -2.5bp) inches lower after Friday’s close of 3.235% was the highest since Jun 20.

- It's a particularly thin docket today, with no notable data or Fedspeak. US CPI looms large tomorrow - the MNI Preview will be out later today but we currently see unrounded estimates for core CPI with a median of 0.24% or average of 0.26% M/M, suggesting downside risk to broad Bloomberg consensus of 0.3%.

OUTLOOK: Price Signal Summary -Monitoring Support in GBPUSD

Jul-14 10:32

- In FX, a corrective cycle in EURUSD remains intact. The primary trend condition is bullish with moving average studies continuing to highlight a dominant uptrend. Support to watch is 1.1660, the 20-day EMA. It has been pierced, a clear break of it would signal scope for a deeper retracement, potentially towards the 50-day EMA at 1.1495. For bulls, a resumption of gains would signal scope for a climb to 1.1851, the Sep 10 2021 high.

- A softer short-term tone in GBPUSD remains in place for now. Price has pierced a key support around the 50-day EMA, at 1.3481. A clear break of this level would undermine a bull theme and signal scope for a deeper retracement. Note that a trendline support - drawn from the Jan 13 low - lies at 1.3419. A break of this support would strengthen a bearish threat. Initial firm resistance to watch is 1.3681, the Jul 4 high.

- USDJPY is trading at its recent highs and a short-term bull cycle remains intact. The pair has recently breached resistance at the 50-day EMA, highlighting a stronger reversal. Note too that 146.77, 76.4% of the Jun 23 - Jul 1 bear leg, has also been cleared, exposing 148.03, the Jun 23 high. Support to watch is 145.20, the 50-day EMA. A clear breach of the average would be bearish.

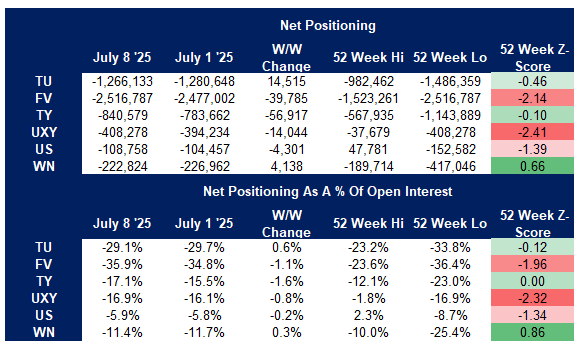

US TSY FUTURES: CFTC: Asset Managers Add To Longs In Wings, Funds Add To Short

Jul-14 10:31

The latest CFTC CoT report revealed the following positioning swings in the week to Tuesday July 8.

- Asset managers added to existing net longs in the wings of the curve (TU, US & WN), while trimming net longs in the belly/intermediates (FV, TY & UXY). They remain net long across the curve, adding a little over $1mn of net curve-wide DV01 exposure on the week.

- Leveraged funds added to net shorts across longer dated contracts, TY, UXY, US & WN, while the cohort trimmed net shorts in TU & FV. They remain net short across the curve and added ~$3.5mn of net curve-wide DV01 exposure on the week.

- Broader non-commercial net positioning was dominated by net short extensions in FV, TY, UXY & US futures, while there was more modest trimming of net shorts in TU & WN. They remain net short across the curve.

Source: MNI - Market News/CFTC/loomberg Finance L.P.