STIR: Fed Rates Hold Yesterday’s Hawkish Tilt, PCE Report In Focus

Dec-05 11:24

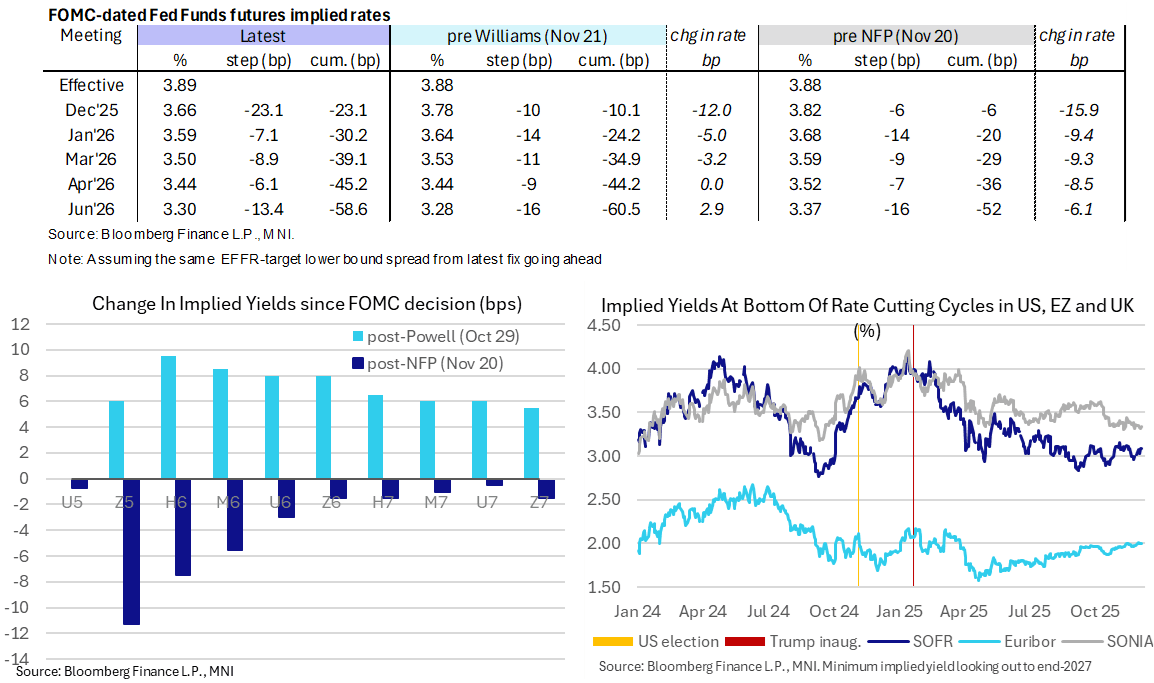

- Fed Funds implied rates are little changed overnight for meetings out to mid-2026, awaiting today’s personal income and outlays report for September at a later than usual 1000ET.

- Cumulative cuts from 3.89% effective: 23bp Dec, 30bp Jan, 39bp Mar, 45bp Apr and 58.5bp Jun.

- SOFR futures are also little changed on the day, with the terminal implied yield of 3.085% holding yesterday’s 5.5bp increase in a move aided that was supported by particularly low initial jobless claims even if they were caveated by a question mark over Thanksgiving adjustments.

- Core PCE inflation is seen increasing ~0.22% M/M in today’s September release after 0.24% in Aug and 0.26% in Jul with scope for small upward revisions there.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EGB OPTIONS: Bund Put Ladder vs Call

Nov-05 11:18

RXZ5 129/128.5/128p ladder vs 131c, bought the ladder for 5 in 3k.

EURIBOR OPTIONS: ERH6 Call Seller

Nov-05 11:17

ERH6 98.1875 call, sold for 2 in 8k

STIR: Fed Rates Steady Before Important Data Updates

Nov-05 11:15

- Fed Funds implied rates hold yesterday’s modest decline in risk-off moves ahead of a more notable docket today with the October ADP and ISM Services reports plus any spillover to front rates from Treasury’s QRA at 0830ET.

- Dec FOMC pricing still holds nearly all of the hawkish adjustment seen after Powell noted a strongly divided committee around December cut prospects at Wednesday’s press conference.

- Cumulative cuts from 3.87% effective: 17bp Dec, 26bp Jan, 35bp Mar, 41.5bp Apr and 56bp Jun.

- SOFR futures are mostly 2 ticks higher on the day looking out to end-2027, with the terminal implied yield edging a little lower to 3.075% (H7) after Monday’s 3.115% highest close since August.

- The SOFR implied terminal yield

- Today sees a pause in scheduled Fedspeak before a heavy schedule tomorrow with Barr, Hammack, Musalem, Paulson, Waller and Williams.