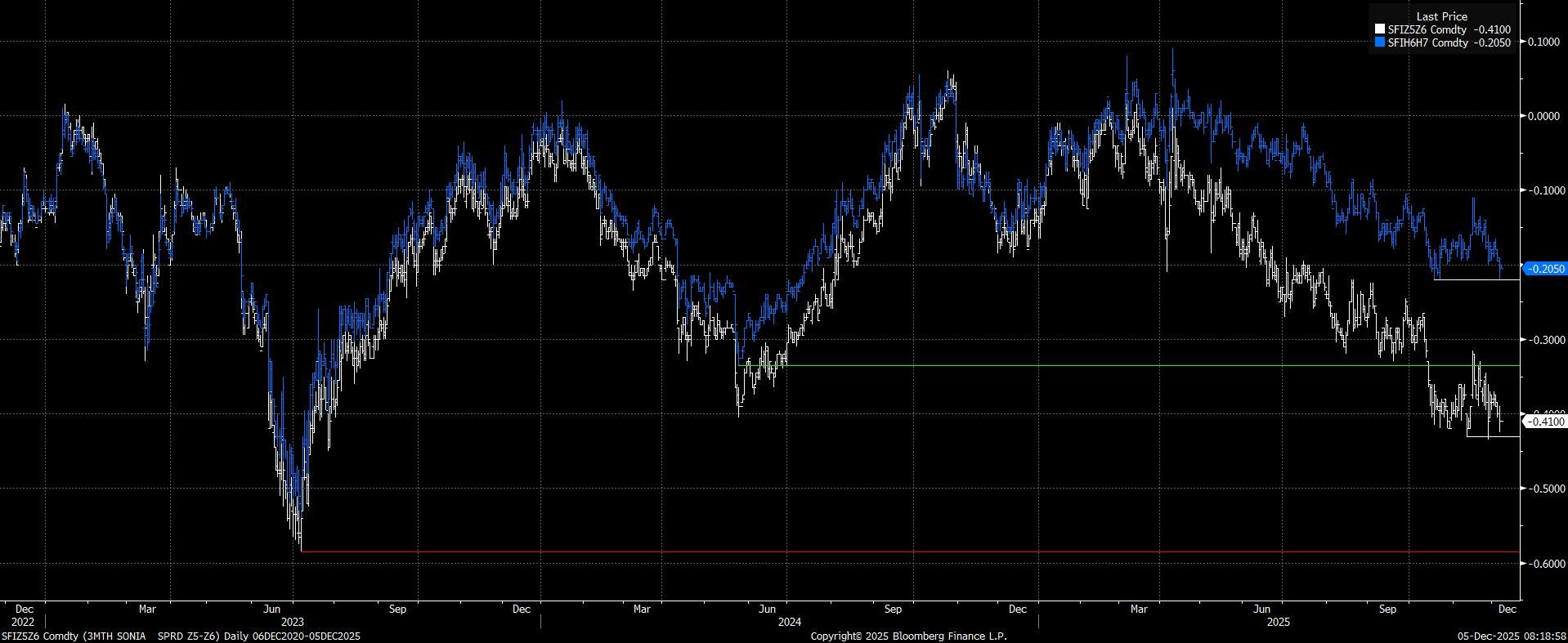

STIR: Recent Lows Holding In Front SONIA 12-Month Spreads

Pre-existing cycle lows in SFIZ5/Z6 and SFIH6/H7 (-43.0 & -22.0, respectively) continue to provide support despite the recent flattening of the strip amid firmer odds of a Dec BoE rate cut, with any breaches proving short-lived and limited in nature.

- A break lower would expose ’23 lows in SFIZ5/Z6 (-58.5) & ’24 lows in SFIH6/H7 (-33.5)

- Potential catalysts for a fresh dovish move include dovish messaging alongside the almost fully discounted December BoE rate cut, further deterioration in labour market data (as seen in yesterday’s BoE DMP survey) and swifter than envisaged progress towards the Bank’s inflation target.

Fig. 1: SONIA Dec ‘25/Dec ’26 (SFIZ5/Z6) & Mar ‘26//Mar ’27 (SFIH6/H7) Spreads

Source: MNI - Market News/Bloomberg Finance L.P.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GILTS: Bullish Theme Intact, BoE In View

Gilts edge higher at the open, taking cues from core global FI markets overnight.

- Note that a recovery from overnight lows in equity benchmarks has pushed both TY & Bund futures away from Asia-Pac eyes.

- Gilt futures little changed at 93.62.

- The bullish technical trend remains intact. Initial support and resistance located at 93.15 & 93.98.

- Yields ~1bp lower in a parallel shift across the curve.

- October lows continue to provide initial yield support levels, with only 30s piercing last month’s base yesterday.

- Final services PMI data is due today, but the bulk of the focus remains split between tomorrow’s BoE decision and local fiscal matters.

- On the former, we have characterised our view as 50/50 (when it comes to a cut or a hold), which is more dovish than current market pricing (~7bp of easing).

- We would have more confidence in a cut if the Budget was not coming into view, particularly given the soft food CPI reading in the latest monthly inflation release.

- Our full preview of the decision will be published later today.

- Elsewhere, the NIESR has suggested that the Budget should include GBP50bln of fiscal consolidation, with the aim of building fiscal headroom of ~1.5% of GDP.

SPAIN DATA: October Services/Composite PMI: More Solid Domestic Demand Signals

Spanish domestic demand remains solid according to the October PMI round, with today’s stronger-than-expected services reading building on the signals from Monday’s manufacturing print. The services and composite readings reached year-to-date highs in October

- MNI: SPAIN OCT SERV PMI 56.6 (54.5 FCAST, 54.3 SEP)

- MNI: SPAIN OCT COMP PMI 56.0 (54.3 FCAST, 53.8 SEP)

Key notes from the release:

- “Panellists linked growth of activity to a mixture of commercial actions, work on existing contracts and increased levels of incoming new work”

- “New business gains were principally driven by domestic clients as new export work rose only slightly. There were reports of an uncertain international environment weighing on foreign demand.”

- “Higher new work encouraged firms to take on additional workers, with employment reported to have risen again during October in line with a trend that stretches back over three years”

- “Panellists are forecasting an uplift in demand and are planning to expand their commercial activities. Overall, sentiment rose to its highest level since March”

- “Input cost inflation dropped to a three-month low”….“ In response to higher input costs, firms sought to protect their operating margins in October by increasing their own selling prices.”

EGBS: Bunds Better Bid Overnight, But Fade Through European Open

- Bund futures posted a decent trading range across the APAC session and through the European cash open, helping trigger some early volatility for European equities. Futures markets are lower on the continent, with DAX and Eurostoxx 50 futures underperforming - off 0.7% apiece - however weakness appears contained for now.

- Softer equities come on the back of further concerns over valuations in the tech sector, with follow-through selling in Palantir shares (down 3% at the close) a nominal trigger, helping lead global markets since the beginning of the week.

- US stock futures are similarly off lows - helping drag Bunds and Treasuries off their respective highs into early European trade. Technically, this leaves support in focus for Bunds into 129.13 - a level pierced on Monday - but not cleanly broken for now. Any further equity weakness could instead prompt a test of resistance, today crossing at 129.73.

DATA: Private sector data is in focus for the US today given the extended government shutdown. US ADP Employment Change will be seen as a proxy for NFP, while ISM Services and the Treasury Quarterly Refunding announcement could prove key. Services PMIs will be final readings for France, Germany, EU, UK and the US.

SUPPLY: Germany look to sell 15s, 20s (equating to a combined 25k Bund) which could weigh into the bidding deadline.