FOREX: Greenback Through Support, GBP Still Primary Beneficiary

Aug-13 09:14

- The greenback is softer against all others in G10, prompting the USD Index to fall for a second session. The price is now through last week's lows of 97.945 further erasing the rally posted off the late July low. Yesterday's CPI print remains the primary driver here, as the data cleared the last hurdle to the Fed resuming an easing cycle from September. OIS markets are now effectively fully priced for a cut, with more than another 25bps cut set to follow before year-end.

- The resultant USD weakness has aided recent rallies in the major pairs. GBP remains a key beneficiary here as the recent hawkish shift at the BoE further contrasts with the Fed. GBP/USD is now cleared of the 50-dma and appears to be building a base toward 1.3589, the mid-July highs. Clearance here would further firm the S/T outlook and keeps the YTD cycle highs in consideration across the medium-term - last traded back at 1.3789 on July 1st.

- EUR/NZD trades under pressure, with NZD outperformance across the board. The cross is fading off the monthly August of 1.9680. Further weakness through 1.9525 would be a bearish signal, and go further in erasing the rally posted at the beginning of this month. Moves come ahead of the RBNZ rate decision set for next week, with a further 25bps rate cut largely expected.

- Focus for the duration of the session remains on the speaker schedule, with data releases sparse. Fed's Barkin, Goolsbee and Bostic are all set to speak - with markets looking to complete the expected layout of votes into September after Fed nominee Miran spoke earlier this week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

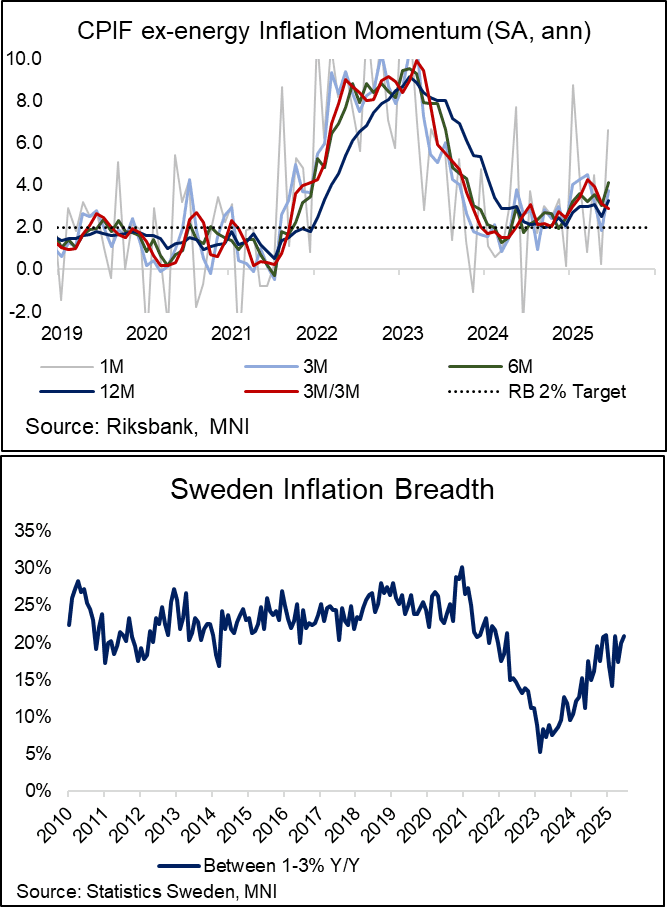

SWEDEN: 3m/3m Inflation Momentum Eases In June Despite Upside Surprise

Jul-14 09:13

Swedish seasonally adjusted core inflation momentum eased in June despite the NSA upside surprise to the Riksbank’s June MPR projection. While the chance of an August Riksbank cut has certainly fallen following the print, it cannot be fully ruled out yet. There is still another inflation print due on August 7 (flash, final on 14th) before the August 20 decision and even then, weak growth data may tilt the Executive Board in favour of further easing.

- MNI’s 3m/3m seasonally adjusted annualised inflation measure fell below 3% for the first time this year at 2.90% (vs 3.14% prior). However, other annualised seasonally adjusted measures did move higher alongside spot NSA rates.

- Splitting apart CPIF ex-energy, we calculate 3m/3m services momentum little changed at 2.75% (vs 2.77% prior), while core goods momentum was weak at -0.41% (vs 0.20% prior). Core goods momentum may rebound next month though, when January’s 1.04% M/M reading falls out of the 3m/3m calculation.

- Turning back to Y/Y NSA rates, the proportion of sub-components with annual rates between 1-3% Y/Y (i.e. broadly target consistent) ticked up to 21% from 20% in May and 17% in April. 63% of components had annual inflation rates below 3% in June, unchanged from May.

MNI EXCLUSIVE: MNI looks at the BOJ's internal policy calculations

Jul-14 09:13

MNI looks at the BOJ's internal policy calculations. -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

EGBS: Citi Recommend 10s30s BTP Flattener Vs. Bunds Or RAGBs

Jul-14 09:04

Citi recommend 10-/30-Year BTP flatteners boxed vs. Bunds or RAGBs.

- They suggest ongoing long-end BTP demand (expectations for foreign demand persistence amid calm politics and primary budget surpluses, calling for a lower risk premium) and limited supply should help flatten the BTP curve.