MNI EUROPEAN OPEN: Japan Labour Earnings Remain Negative

EXECUTIVE SUMMARY

- SUPREME COURT APPEARS SKEPTICAL OF TRUMP'S BLOBAL TARIFFS - BBG

- US ORDERS 10% FLIGHTS CUT AT MAJOR US AIRPORTS DUE TO SHUTDOWN - RTRS

- SEASONAL DEMAND BOOST TO SERVICES WILL FADE - ISM - MNI INTERVIEW

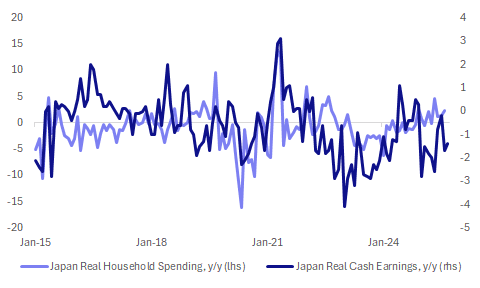

- JAPAN SEPT REAL WAGES NEGATIVE FOR NINTH MONTH - MNI BRIEF

Fig 1: Japan Real Labour Earnings Remain Negative Y/Y

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

FISCAL (MNI): The UK government could potentially close up to a tenth of its fiscal gap in the coming year by raising national insurance contributions on the self-employed closer to those paid by contracted employees, leading policy think tanks told MNI.

UKRAINE (POLITICO): “The British defense secretary has insisted Donald Trump is capable of persuading Vladimir Putin to enter peace talks on Ukraine even as negotiations continue to stall. “President Trump is the figure that can bring Putin to the table, that can potentially deliver an end to the fighting,” he said.”

PHARMACEUTICALS (TIMES): “The US ambassador has warned that pharmaceutical companies will close facilities in Britain unless changes to drug prices are made quickly.”

EU

NATO (NATO): “The 2025 edition of the NATO-Industry Forum will take place in Bucharest (Romania) on 5-6 November 2025. 08:30- 09:15: Keynote Addresses by: President of Romania Nicușor Dan; NATO Secretary General Mark Rutte; and NATO’s Supreme Allied Commander Transformation Admiral Pierre Vandier. On-the-record, livestreamed.”

NATO (POLITICO): “NATO chief Mark Rutte on Wednesday played down a U.S. announcement that it was withdrawing hundreds of troops from Romania. “This happens all the time … please don't read too much into that,” Rutte told POLITICO at a press conference. “Wherever and whenever needed we can always scale up collectively, including in Romania.””

FRANCE (BBC): “The French government says it is initiating proceedings to suspend the online platform of Asian online giant Shein. The economy ministry said under the prime minister's order proceedings would last for "as long as necessary for the platform to prove to authorities that all of its content is finally in compliance with our laws and regulations".”

RUSSIA (POLITICO): “Russian President Vladimir Putin on Wednesday ordered top officials to come up with proposals for the potential resumption of nuclear testing for the first time since the end of the Cold War more than three decades ago.”

US

TARIFFS (BBG): "The US Supreme Court appeared skeptical of President Donald Trump’s sweeping global tariffs, as key justices suggested he had overstepped his authority with his signature economic policy."

GOVERNMENT (RTRS): “U.S. Transportation Secretary Sean Duffy said on Wednesday that he would order a 10% cut in flights at 40 major U.S. airports, citing air traffic control safety concerns as a government shutdown hit a record 36th day.”

SERVICES (MNI INTERVIEW): The fastest gain in U.S. service sector activity in eight months in October was due to seasonal increases that will fade back to a modest growth pace over time, Institute for Supply Management services chair Steve Miller told MNI Tuesday.

CONSUMER (MNI BRIEF): U.S. consumers are facing high but stable delinquency rates in auto and credit card loans, according to a new report from the New York Fed.

OTHER

DEBT (BBG): "Global bond sales have soared to a record this year as borrowers take advantage of easy market conditions to fund everything from the boom in artificial intelligence projects to a revival in acquisitions."

JAPAN (MNI INTERVIEW): Ex-BOJ's Kameda Sees Dec Hike, Ueda Not Dovish. A former BOJ chief economist shares his policy rate outlook.

JAPAN (MNI BRIEF): Japan’s inflation-adjusted real wages fell 1.4% y/y in September, marking the ninth consecutive month of decline after a 1.7% fall in August, preliminary data from the Ministry of Health, Labour and Welfare showed Thursday.

JAPAN (BBG): " A Bank of Japan move to raise interest rates at a time when the government is calling on companies to invest more would likely send a mixed message on policy, according to the leader of Japan’s ruling coalition partner."

CANADA (MNI INTERVIEW): Prime Minister Mark Carney's first budget falls short on fixing damage from Donald Trump's tariff war and appealing to voters hurt by a cost of living squeeze that underpinned his electoral win of a minority government, a top fiscal expert told MNI.

CHINA

ECONOMY (YICAI): “The Yicai Chief Economist Confidence Index remained steady at 50.3 in November, as authorities remain on course to meet the 5% annual growth target. For the upcoming October data release, economists project retail sales growth of 2.7% year-on-year, slightly below September’s 3% and industrial added value growth of 5.7%, down from 6.5% in the previous month.”

BONDS (YICAI): “China’s bond market has remained subdued even after the People’s Bank of China injected a net CNY20 billion through bond trades in October, Yicai reported, noting that volumes had fallen short of expectations. “

MNI: PBOC Net Drains CNY249.8 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY92.8 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY249.8 billion after offsetting maturities of CNY342.6 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4118% at 09:41 am local time from the close of 1.4378% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Wednesday, compared with the close of 48 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0865 Thurs; +1.41% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0865 on Thursday, compared with 7.0901 set on Wednesday. The fixing was estimated at 7.1233 by Bloomberg survey today.

MARKET DATA

JAPAN SEPT. LABOR CASH EARNINGS +1.9% Y/Y; EST. +1.9%; AUG. +1.3%

JAPAN SEPT. REAL CASH EARNINGS -1.4% Y/Y; EST. -1.5%; AUG. -1.7%

JAPAN SEPT. CASH WAGES FROM SAME SAMPLE +2.4% Y/Y; EST. +2.3%; AUG. +1.9%

JAPAN SEPT. SAME SAMPLE REGULAR FULL TIME PAY +2.2% Y/Y; EST. +2.5%; AUG. +2.4%

JAPAN S&P GLOBAL OCT. SERVICES PMI 53.1; PRE. 52.4; SEP. 53.3

JAPAN S&P GLOBAL OCT. COMPOSITE PMI 51.5; PRE. 50.69; SEP. 51.3

JAPAN TOKYO OCT. OFFICE VACANCIES 2.59%; SEP. 2.68%

S.KOREA SEPT P CURRENT ACCOUNT BALANCE +$13.47 BLN; AUG. +$9.15 BLN

S. KOREA SEPT P GOODS BALANCE +$14.24 BLN; AUG. +$9.40B

AUSTRALIA SEPT. TRADE SURPLUS A$3.94B; EST. A$4.00B; AUG. A$1.11B

AUSTRALIA SEPT. EXPORTS +7.9% M/M; AUG. -8.7%

AUSTRALIA SEPT. IMPORTS +1.1% M/M; AUG. +3.3%

MARKETS

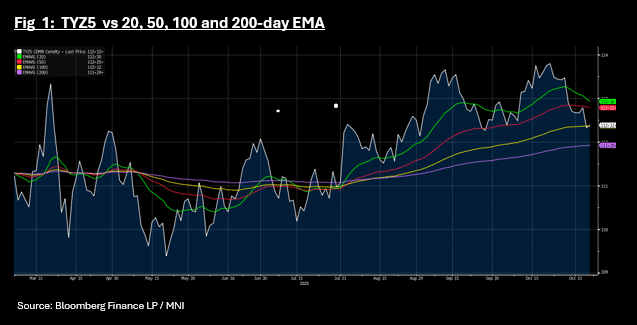

US TSYS: TYZ5 Back Above Key Tech Level

The overnight rally was sustained in Asia today with bond futures all up, albeit modestly. The 10-Yr TYZ5 is up +03 to 112-13+ in a low volume day, having trended below the 100-day EMA overnight. The rally today takes the 10-Yr back above the 100-day EMA.

Risk appetite in the Asia trading day was strong with regional bourses posting solid gains. Bonds got a bid also given the re-pricing overnight and cash down up to 1-2bps across the curve.

- The 2-Yr fell -1.2bps to 3.621%

- The 5-Yr is down -1.4bps to 3.751%

- The 10-Yr is down -1.6bps to 4.145%

- The 30-yr declined -1bps to 4.73%

The focus for issuance tonight is a US$110bn 4-week bill and a US$95bn 8-week bill auction.

Data releases are delayed tonight instead will have Fed Speakers Barr, Williams and Hammack.

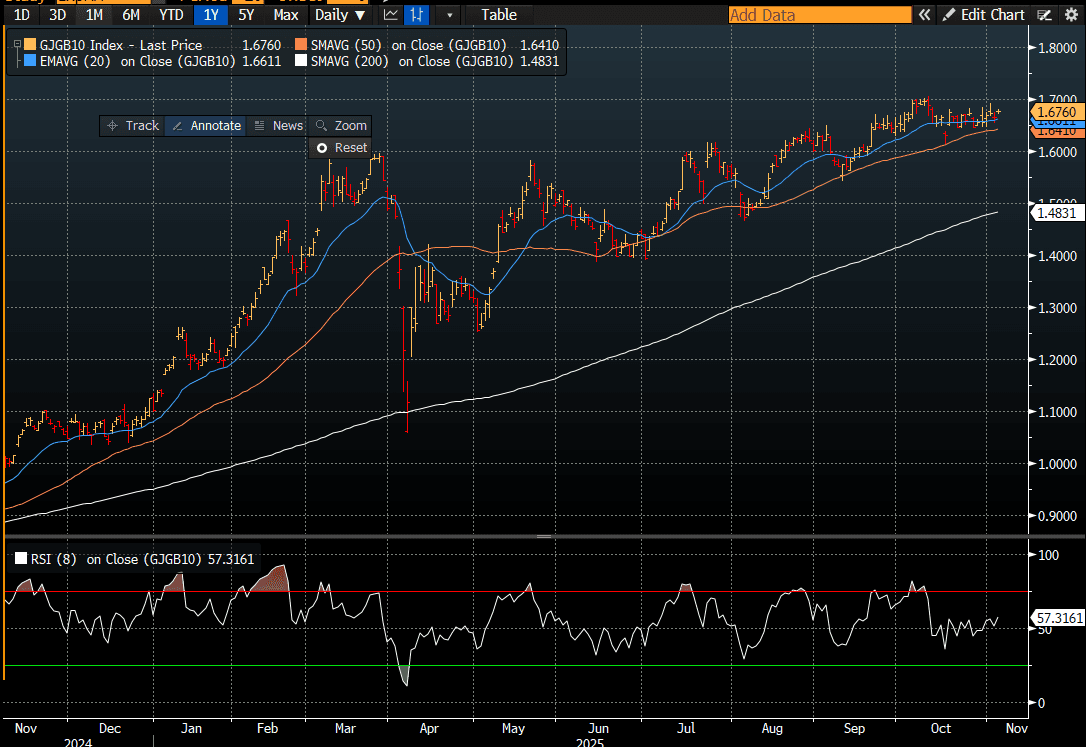

JGBS: Weaker But Off Session Cheaps

JGB futures are weaker, -12 compared to settlement levels, but well above the session's worst levels.

- MNI Brief: Japan's inflation-adjusted real wages fell 1.4% y/y in September, marking the ninth consecutive month of decline after a 1.7% fall in August, preliminary data from the Ministry of Health, Labour and Welfare showed Thursday. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Cash US tsys are ~1bp richer in today's Asia-Pac session after yesterday's sell-off. The US 10-year yield hovers near one-month highs. Fed officials such as John Williams, Michael Barr, Beth Hammack, Christopher Waller, and Anna Paulson will speak later in the US session. The market is pricing a 70% probability of a 25bps rate cut in December.

- Cash JGBs are flat to 1bp cheaper across benchmarks, with the 10-year underperforming. The benchmark 10-year yield is 1.2bps higher at 1.676% versus the cycle high of 1.705%. (see chart)

- Swap rates are flat to 2bps lower.

- Tomorrow, the local calendar will see Household Spending and Weekly International Investment Flow data alongside an Auction for Enhanced-Liquidity 5-15.5 YR.

Source: Bloomberg Finance LP

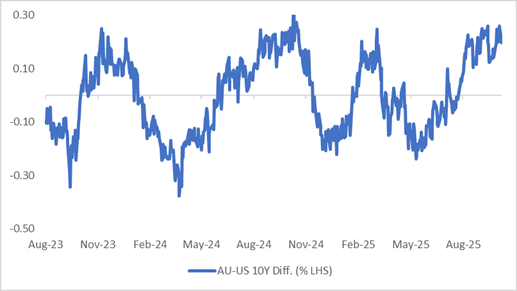

AUSSIE BONDS: Heavy Session As Market Digests A Cautious RBA

ACGBs (YM -4.5 & XM -6.0) are weaker and at or near session cheaps.

- Cash ACGBs are 4-5bps cheaper with the AU-US 10-year yield differential at +22bps. At this level, the spread has recoiled from the upper end of the 30bps range that has persisted since November 2022. (see chart)

- MNI RBA Review: The RBA Monetary Policy Board unanimously left rates at 3.6%, as was widely expected, and sounded generally cautious. Staff trimmed mean projections were revised higher over the rest of 2025 and 2026, with the important 2q/2q annualised rate returning to 3% in Q1 and 2.6% in Q4, which may allow a rate cut from May if this eventuates. Decisions remain highly data-dependent. (see link)

- The bills strip is weaker, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing is little changed following this week’s RBA Policy Decision. RBA-dated OIS pricing is showing a 25bp rate cut in December at a 10% probability, with a cumulative 18bps of easing priced by mid-2026. Notably, current pricing leaves levels some 22-26bps firmer than pre-Q3 CPI levels in late October.

- Tomorrow, the local calendar will see Foreign Reserves.

- The AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond on Friday.

Bloomberg Finance LP

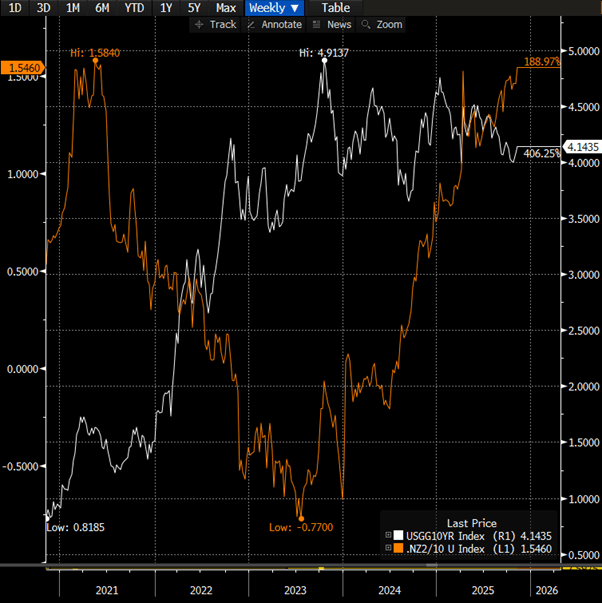

BONDS: NZGBS: Bear-Steepener Pushes Curve Towards 2021 Highs

NZGBs closed showing a bear-steepener, with benchmark yields 1-5bps higher.

- Today’s move leaves the NZGB 2/10 yield curve at 155bps and near its steepest level since 2021. When the curve was last this steep, the OCR stood at 0.25%, compared with 2.5% today. Although the NZ–US 10-year yield differential is near its 2021 level, the US 10-year yield is now 4.16%, up from 1.65% at that time. (see chart)

- The NZGB 10-year outperformed its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3bps and 1bps narrower on the day.

- Today’s weekly supply was received with solid demand. Cover ratios ranged from 3.24x (May-54) to 3.97x (Apr-29).

- Swap rates closed 1-4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 28bps of easing is priced for November, with a cumulative 36bps by February 2026.

- Tomorrow, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data on Tuesday.

Bloomberg Finance LP

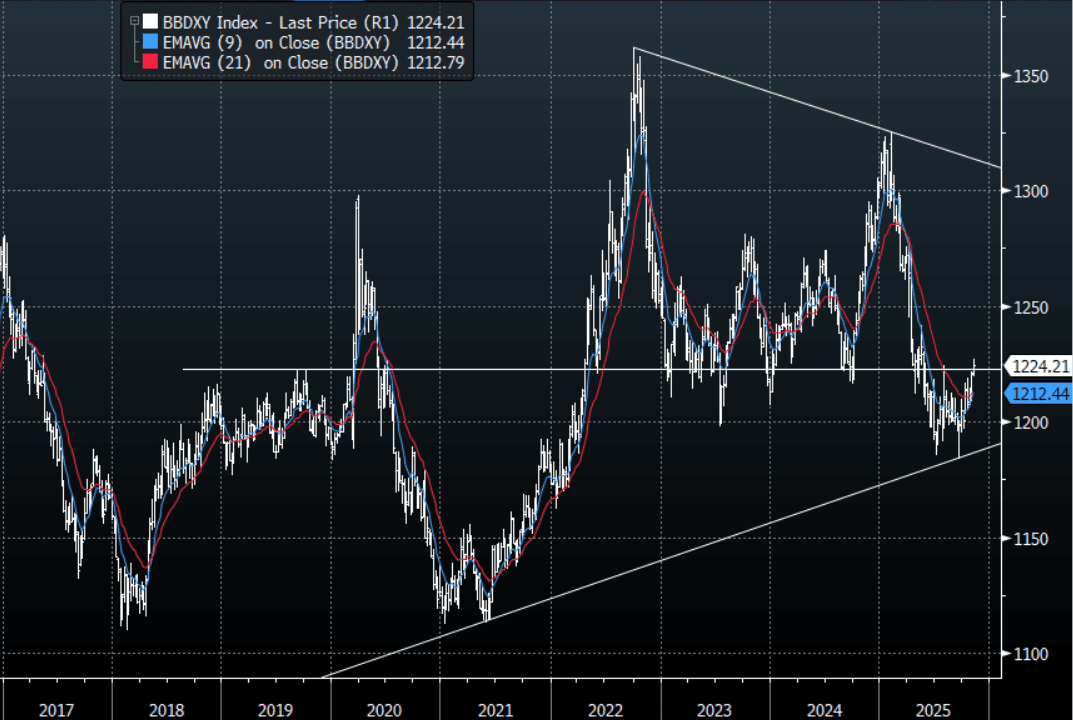

FOREX: Asia-Pac FX: USD Drifts Lower, Focus On Supreme Court Tariff Ruling

The BBDXY has had a range today of 1223.95 - 1225.11 in the Asia-Pac session; it is currently trading around 1224, -0.10%. The USD broke its run of consecutive highs as it stalled toward 1230 and has ended lower for the first time in quite a few days. The 1230 area remains tough resistance, a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made and the dips remain very shallow pointing to a reduction in shorts. The decision from the Supreme court though could have huge implications for both the USD and the Bond market. Should they reject the Trump administration's arguments, the US would have to pay back something in the region of $100 billion in tariffs collected, which would have huge ramifications on the deficit as well as funding going forward.

- EUR/USD - Asian range 1.1487 - 1.1509, Asia is currently trading 1.1505. The pair’s momentum lower stalled below 1.1500, I suspect rallies will now be sold into with the first resistance back toward the 1.1600 area.

- GBP/USD - Asian range 1.3046 - 1.3065, Asia is currently dealing around 1.3060. The pair found some support back toward 1.3000 yesterday. I continue to favor fading rallies though as GBP looks like it has put in a medium term top. First sell zone back toward 1.3150 and then the more important 1.3300 area. BOE today could provide some movement.

- Cross asset : SPX -0.05%, Gold $3985, US 10-Year 4.1450%, BBDXY 1224, Crude Oil $59.84

- Data/Events : France Private Sector Payrolls, Spain Industrial Production, Germany HCOB Germany Construction PMI, EZ Retail Sales

Fig 1: BBDXY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

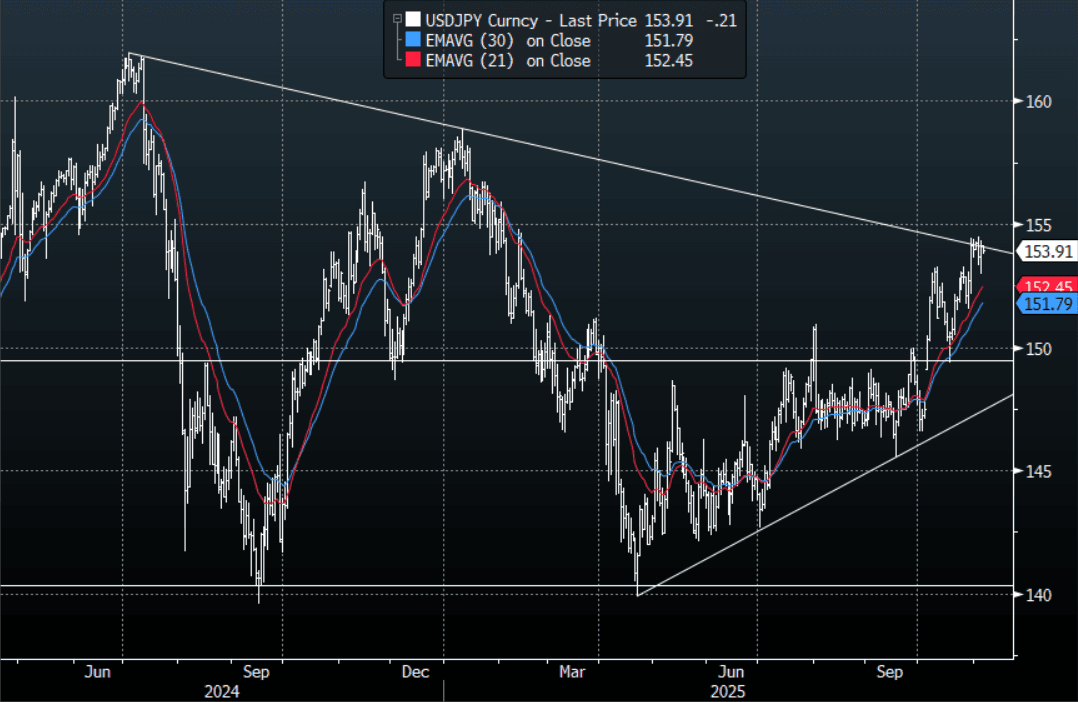

JPY: Asia-Pac: USD/JPY Struggles To Hold Above 154.00

The USD/JPY range today has been 153.80 - 154.36 in the Asia-Pac session, it is currently trading around 153.90, -0.15%. The pair bounced strongly yesterday off the 153.00 area as cross-Yen did an about face as risk recovered paring back losses overnight. A lot depends on what your view is for risk from here, should the price action of the last few days signal that we could be putting in a top and a correction of sorts plays out then I suspect the resistance around the 154/155 area should continue to offer solid resistance. If we see a similar price action to what we have all year and risk just goes straight back to make new all-time highs as we head into the year-end rally then it's highly probable this resistance gives way and we target levels closer to 160.00.

- MNI BRIEF: Japan Sept Real Wages Negative For Ninth Month. Japan’s inflation-adjusted real wages fell 1.4% y/y in September. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.14b), 155.00($1.88b), 155.35($1.38b). Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

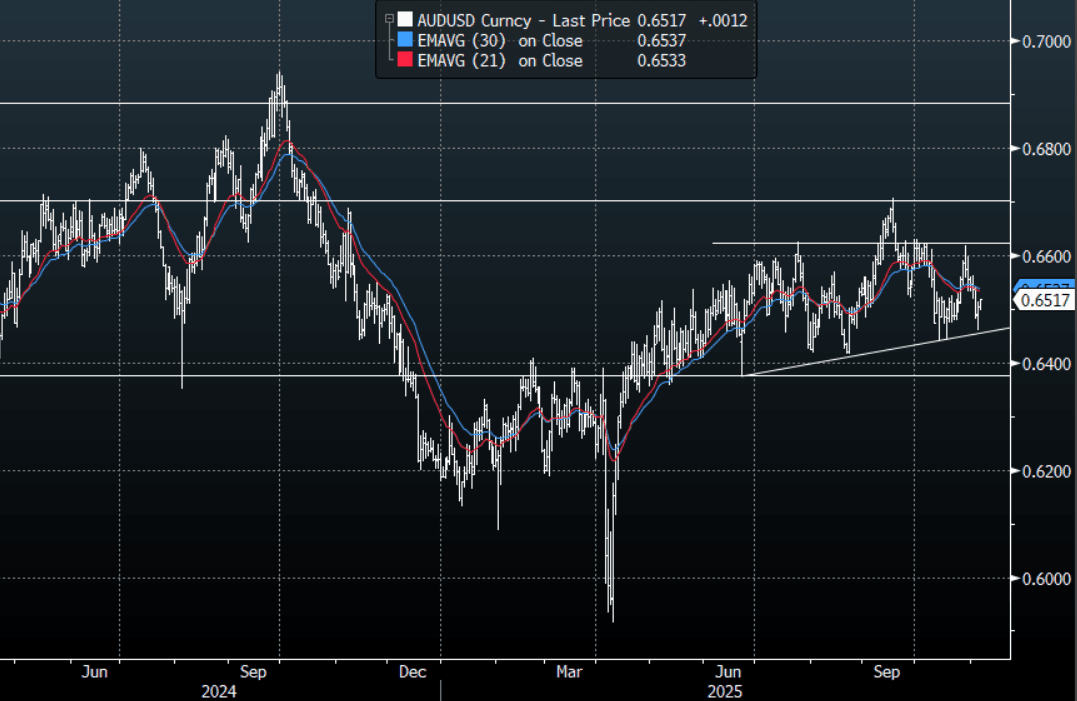

AUD: Asia-Pac: AUD/USD Recovers Back Above 0.6500

The AUD/USD has had a range today of 0.6497 - 0.6517 in the Asia- Pac session, it is currently trading around 0.6515, +0.20%. Was that it ? The dip buyers in risk look once again to be in control and what looked like the start of a correction has quickly petered out. The AUD/USD finds itself back in the middle of its now familiar range, having chopped sideways between 0.6350-0.6650 since April this year. A lot rides on how risk trades from here, should this potential correction lower play out then the USD should again come to the fore, but if that was the extent of the correction and we start building toward a year end rally for risk assets then the AUD can again start to outperform. The pivot for the AUD is around 0.6550, above there and we start to turn toward the top of the range again.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6490(AUD487m), 0.6550(AUD 479m), 0.6600(AUD567m). Upcoming Close Strikes : 0.6450(AUD544m Nov 11), 0.6500(AUD1.02b Nov 7), 0.6600(AUD682m Nov 7)- BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

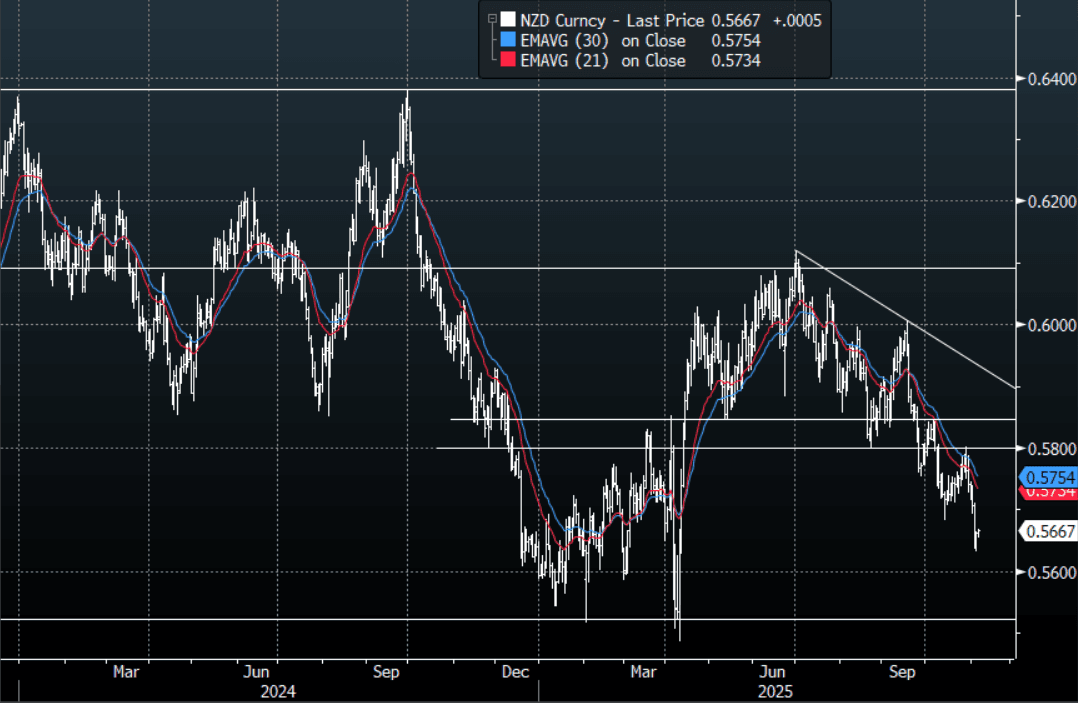

NZD: Asia-Pac: NZD/USD - Finds Bids Below 0.5650

The NZD/USD had a range of 0.5655 - 0.5668 in the Asia-Pac session, going into the London open trading around 0.5665, +0.02%. Was that it ? The dip buyers look once again to be in control and what looked like the start of a correction for risk has quickly petered out. The NZD move lower has stalled finding some demand below 0.5650 as risk stabilsed. While price remains below the 0.5800/50 area I suspect rallies will continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. The NZD stands out as a vehicle to short against a resurgent USD but it is worth noting that because of the size of the market it can very quickly become all positioned the same way. I think the USD will need to do the heavy lifting from here and break above its pivotal resistance for the NZD to test the 0.5500 lows. The first sell zone on the day would be back toward the 0.5700-0.5725 area.

- MNI AU - NZ 2/10 Yield Curve Steepest Since 2021: The NZ 2/10 yield curve has steepened to its highest level since 2021. When the curve was last this steep, the OCR stood at 0.25%, compared with 2.5% today. Although the NZ-US 10-year yield differential is near its 2021 level, the US 10-year yield is now 4.16%, up from 1.65% at that time.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5730(NZD496m), 0.5780(NZD305m). Upcoming Close Strikes : none - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Bourses Rebound as Tech Bargain Hunters Emerge

The lure of tech stocks for bargain hunters ended the two days of losses, with the NIKKEI and the KOSPI back in the positive whilst the Hang Seng led the regional bourses. The likes of SK Hynix Inc in Korea had fallen almost 8% in two days, yet has recovered half of that in today's rally. In what is often the next step in a sector rally such as this is M&A and there are reports today that Softbank Group Corp. shares rose 0.5% as it explored a potential takeover of US chipmaker Marvell Technology Inc. BBG also reports that the MSCI global stock index saw the number of Chinese companies has climbed for the first time in nearly two years, setting up the market for more inflows from passive investors.

- The HSI is up +1.64% leading the regional gains, taking it back above its 20-day EMA having bounced on the 50-day EMA. The CSI 300 is up +1.2%, Shanghai +0.88% and Shenzhen up +0.90%.

- The Nikkei fell -4.20% in two day, but has bounced on the tech rebound - up +1.3% today whilst the KOSPI rose +1.5%.

Ahead of the Central Bank decision later, the FTSE Malay KLCI is trending sideways whilst the JCI in Indonesia is up marginally and the SE Thai by +0.7%

OIL: Saudi Cuts Prices To Asia, Fed Speakers Later On Thursday

Oil prices are moderately higher but within a narrow range during today’s APAC trading after Wednesday’s 1.5% fall and mixed EIA US inventory report that suggested robust product demand. The as expected Saudi reduction in prices across its crude grades for Asian customers helped the stabilisation, as the move could increase regional demand. A softer US dollar has been supportive (BBDXY -0.1%).

- WTI is up 0.4% to $59.80/bbl after reaching $59.86 off the intraday low of $59.55. Brent is 0.3% higher at $63.72/bbl following a high of $63.78.

- The EIA reported a US crude oil inventory build of 5.2mn barrels last week after destocking of 6.86mnm. However, gasoline stocks fell 4.7mn barrels, and distillate was down 0.6mn, the fifth consecutive weekly decline for both suggesting demand remains solid. The 0.6pp decline in refining utilisation to 86%, 4.5pp below the same time last year, helped to drive the crude stock build and product drawdown.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold.

- US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

Gold Slightly Higher But Still In Range, Will Watch Upcoming Fed Speakers

Gold prices are moderately higher in Thursday’s APAC session supported by a softer US dollar (BBDXY -0.1%) and slightly lower yields. The chance of a December Fed rate cut has also risen also boosting non-interest bearing bullion. The market has been range trading this week driven by uncertainty over the outlook for the next Fed decision. Gold is up 0.2% to $3987.0 today off the high of $3990.43.

- With US data scarce due to the government shutdown, ADP October employment was watched closely. With a 42k rise after two consecutive falls, it signalled that the labour market remains soft but may have stabilised. Looking forward, the swathe of Fed speakers on Thursday will be monitored for thinking regarding upcoming decisions.

- Silver is 0.5% higher at $48.24 after reaching $48.263 following a low of $47.738. Like gold it has traded between resistance at $49.456, 23 October high, and support at $46.089, 50-day EMA. The trend in the metal remains bullish and any declines are considered corrective.

- Equities are generally stronger with the Nikkei up 1.4% and CSI 300 +1.3% but S&P e-mini flat. Oil prices are higher with WTI +0.4% to $59.86/bbl. Copper is up 0.6%.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold. US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/11/2025 | 0700/0800 | ** | Industrial Production | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0700/0800 | *** | Flash Inflation Report | |

| 06/11/2025 | 0800/0900 | ** | Industrial Production | |

| 06/11/2025 | 0800/0900 | ** | Unemployment | |

| 06/11/2025 | 0810/0910 | ECB Schnabel At ECB Money Market Conference | ||

| 06/11/2025 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 06/11/2025 | 0830/0930 | ECB De Guindos On Natixis Webinar | ||

| 06/11/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 06/11/2025 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 06/11/2025 | 1000/1100 | ** | EZ Retail Sales | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 06/11/2025 | 1230/1230 | BOE Press Conference | ||

| 06/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 06/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 06/11/2025 | 1330/0830 | ** | Preliminary Non-Farm Productivity | |

| 06/11/2025 | 1400/1400 | Decision Maker Panel Data | ||

| 06/11/2025 | 1500/1000 | * | Ivey PMI | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1500/1000 | ** | Wholesale Trade | |

| 06/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 06/11/2025 | 1530/1030 | BOC Governor Macklem testifies at Senate. | ||

| 06/11/2025 | 1600/1100 | NY Fed's John Williams | ||

| 06/11/2025 | 1600/1100 | Fed Governor Michael Barr | ||

| 06/11/2025 | 1630/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 06/11/2025 | 1630/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 06/11/2025 | 1700/1200 | Cleveland Fed's Beth Hammack | ||

| 06/11/2025 | 1830/1930 | ECB Lane At IMF Conference | ||

| 06/11/2025 | 1900/1400 | *** | Mexico Interest Rate | |

| 06/11/2025 | 2030/1530 | Fed Governor Christopher Waller | ||

| 06/11/2025 | 2130/1630 | Philly Fed's Anna Paulson | ||

| 06/11/2025 | 2230/1730 | St. Louis Fed's Alberto Musalem | ||

| 07/11/2025 | 2330/0830 | ** | Household spending | |

| 07/11/2025 | 0700/0800 | ** | Trade Balance | |

| 07/11/2025 | 0745/0845 | * | Foreign Trade | |

| 07/11/2025 | 0800/0300 | New York Fed's John Williams | ||

| 07/11/2025 | 1110/1110 | BOE Saporta At ECB Money Market Conference | ||

| 07/11/2025 | 1200/0700 | Fed Vice Chair Philip Jefferson | ||

| 07/11/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 07/11/2025 | - | *** | Trade | |

| 07/11/2025 | - | BOE MPG Agenda Published | ||

| 07/11/2025 | 1330/0830 | *** | Labour Force Survey | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/1430 | ECB Elderson At Bundesbank Event |