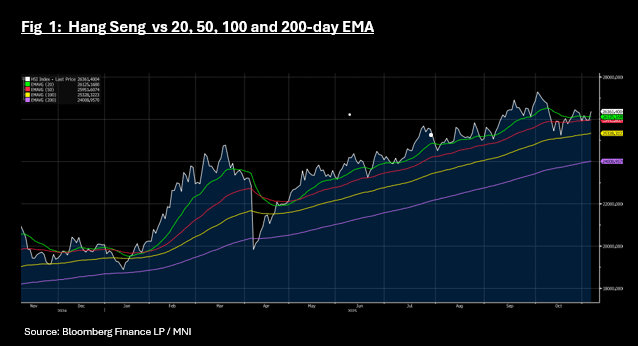

ASIA STOCKS: Bourses Rebound as Tech Bargain Hunters Emerge

The lure of tech stocks for bargain hunters ended the two days of losses, with the NIKKEI and the KOSPI back in the positive whilst the Hang Seng led the regional bourses. The likes of SK Hynix Inc in Korea had fallen almost 8% in two days, yet has recovered half of that in today's rally. In what is often the next step in a sector rally such as this is M&A and there are reports today that Softbank Group Corp. shares rose 0.5% as it explored a potential takeover of US chipmaker Marvell Technology Inc. BBG also reports that the MSCI global stock index saw the number of Chinese companies has climbed for the first time in nearly two years, setting up the market for more inflows from passive investors.

- The HSI is up +1.64% leading the regional gains, taking it back above its 20-day EMA having bounced on the 50-day EMA. The CSI 300 is up +1.2%, Shanghai +0.88% and Shenzhen up +0.90%.

- The Nikkei fell -4.20% in two day, but has bounced on the tech rebound - up +1.3% today whilst the KOSPI rose +1.5%.

Ahead of the Central Bank decision later, the FTSE Malay KLCI is trending sideways whilst the JCI in Indonesia is up marginally and the SE Thai by +0.7%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

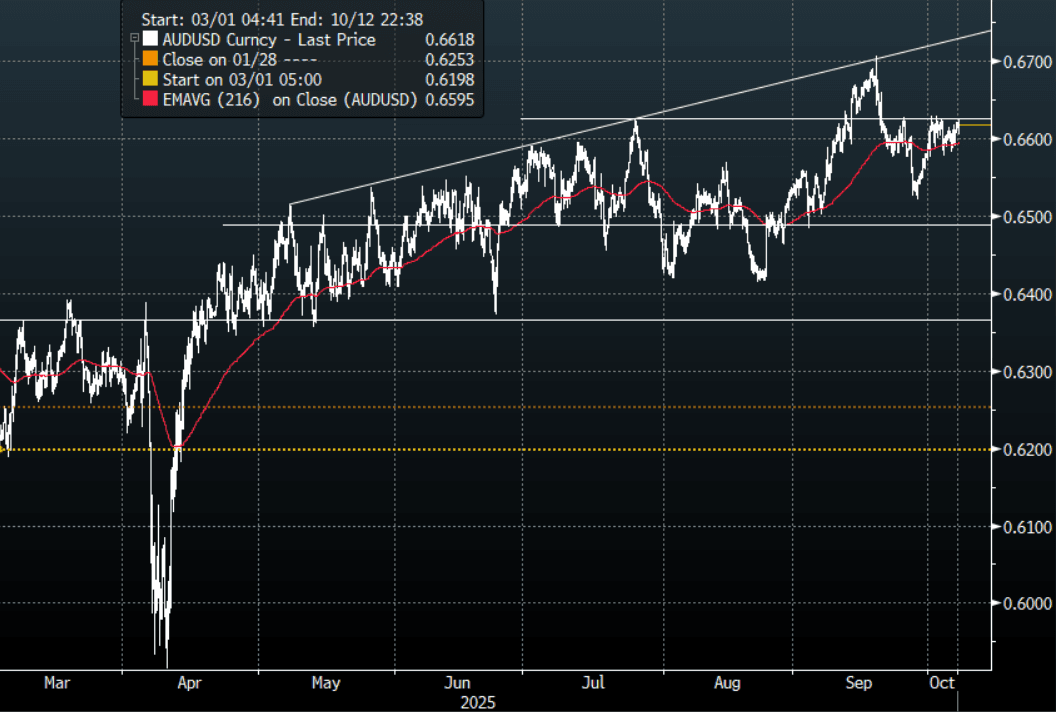

AUD: Asia Wrap - AUD/USD Consolidates Gains Above 0.6600

The AUD/USD has had a range of 0.6604 - 0.6624 in the Asia- Pac session, it is currently trading around 0.6620, +0.05%. The AUD has drifted higher, helped by the way risk continues to surge and probably some AUD/JPY demand as the JPY crosses look to break some big levels and look to regain the trend higher. A move back through the 0.6625/50 area is needed to gain the momentum to have another look toward the pivotal 0.6700 area.

- MNI AU - Stall In Disinflation Weighing On Consumer Confidence. Westpac consumer confidence fell for the second straight month in October as higher inflation prints appear to have weighed on assessments of family finances and the economy. Thus, Q3 CPI on 29 October is likely to be important for households too. The RBA’s decision to leave rates at 3.6% and cautious tone appear to have actually reassured consumers. Sentiment was down 3.5% m/m to 92.1, the lowest in 6 months. Households remain cautious but are prepared to spend at the right price. Q3 expenditure growth improved compared to Q2 with signs of a pickup in discretionary spending.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6735(AUD350m). Upcoming Close Strikes : 0.6300(AUD899m Oct 8 )- BBG

- AUD/JPY - Asia-Pac range 99.38 - 99.68, Asia is trading around 99.50. The pair has surged higher for good reason on the election outcome. With Risk surging higher at the same time the carry trade will start to be looked at again. Dips will now be supported as the focus now turns toward 100 and then beyond.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Yields Unchanged In A Quiet Session

The TYZ5 range has been 112-12+ to 112-15 during the Asia-Pacific session. It last changed hands at 112-14, up 0-01+ from the previous close.

- The US 2-year yield is trading 3.586%.

- The US 10-year yield is trading around 4.15%.

- 10-Year yields bounced on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade the move higher.

- Bloomberg - “Global Long Bonds Can Breathe Easier After 30-Year JGB Sale. Japan’s thirty-year auction went off smoothly with a higher bid-to-cover ratio than the previous sale, which will be a relief for investors across G-10 long-term debt. Traders will also be reassured with MUFJ-MS taking up the biggest slice of the bonds, along with Japan’s other big primary dealers.”

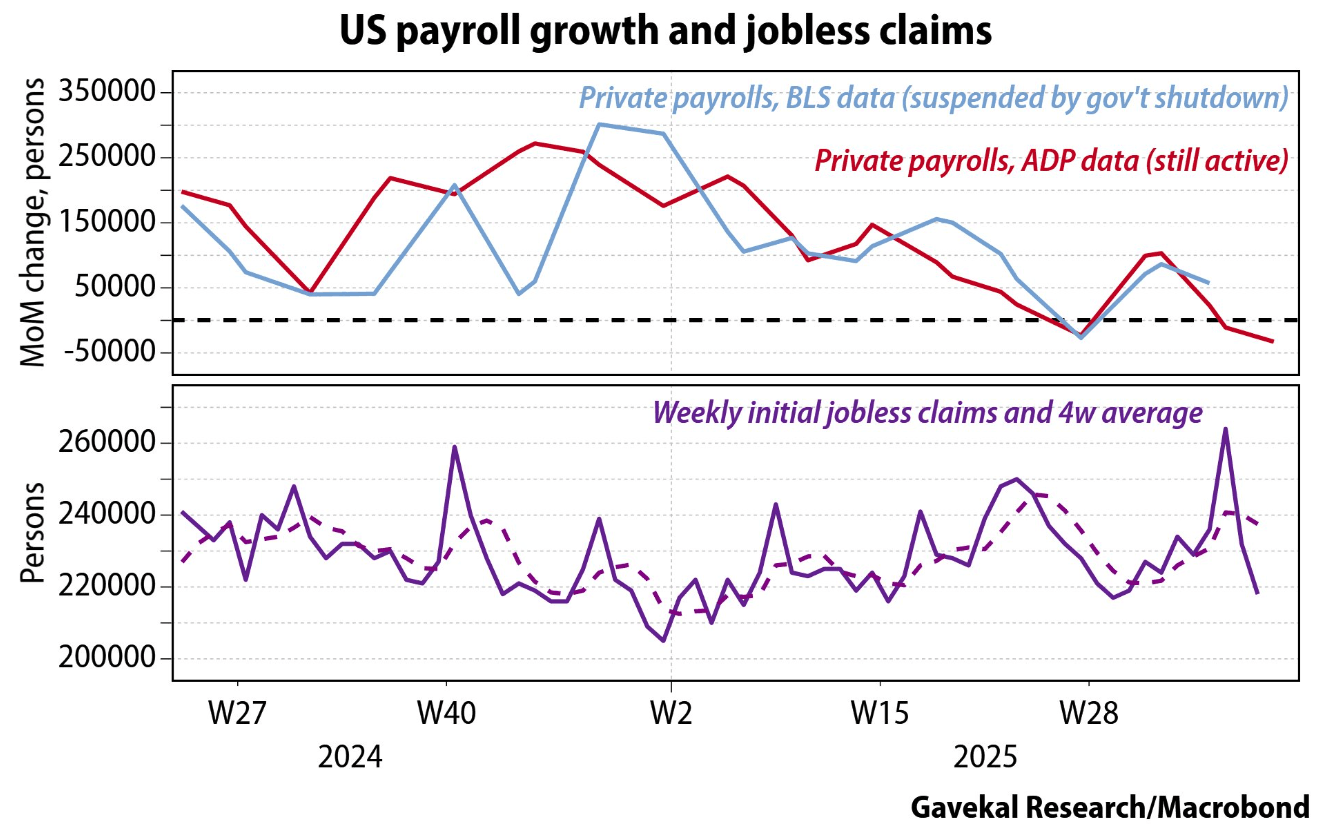

Gavekal on X: “With the Bureau of Labor Statistics temporarily dark due to the US government shutdown, investors and the Federal Reserve must rely on other employment data. Worryingly, ADP’s private payroll estimate showed its most significant contraction of this cycle. That could be the result of the immigration crackdown reducing the supply of available workers. It is also possible that slack is starting to appear in the labor market, perhaps due to the temporary fiscal contraction from tariffs or AI causing unemployment, especially among young graduates. The recent decline in jobless claims is encouraging, but it is worth noting that many young graduates do not have prior work history and thus may not be eligible to claim unemployment benefits.” See Graph Below.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

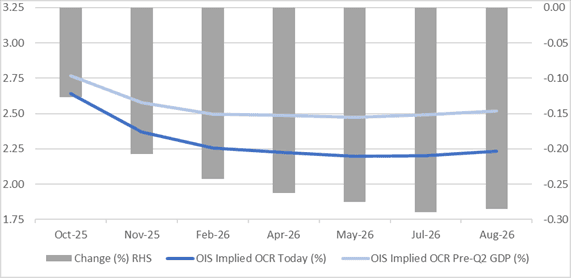

STIR: RBNZ-Dated OIS Holding Post-GDP Softening Ahead Of Tomorrow's Decision

RBNZ-dated OIS pricing closed slightly softer across meetings today, ahead of tomorrow’s RBNZ Policy Decision.

- 36bps of easing is priced for tomorrow’s meeting, with a cumulative 63bps by November 2025.

- Notably, pricing is 13-28bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI