OIL: Saudi Cuts Prices To Asia, Fed Speakers Later On Thursday

Oil prices are moderately higher but within a narrow range during today’s APAC trading after Wednesday’s 1.5% fall and mixed EIA US inventory report that suggested robust product demand. The as expected Saudi reduction in prices across its crude grades for Asian customers helped the stabilisation, as the move could increase regional demand. A softer US dollar has been supportive (BBDXY -0.1%).

- WTI is up 0.4% to $59.80/bbl after reaching $59.86 off the intraday low of $59.55. Brent is 0.3% higher at $63.72/bbl following a high of $63.78.

- The EIA reported a US crude oil inventory build of 5.2mn barrels last week after destocking of 6.86mnm. However, gasoline stocks fell 4.7mn barrels, and distillate was down 0.6mn, the fifth consecutive weekly decline for both suggesting demand remains solid. The 0.6pp decline in refining utilisation to 86%, 4.5pp below the same time last year, helped to drive the crude stock build and product drawdown.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold.

- US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

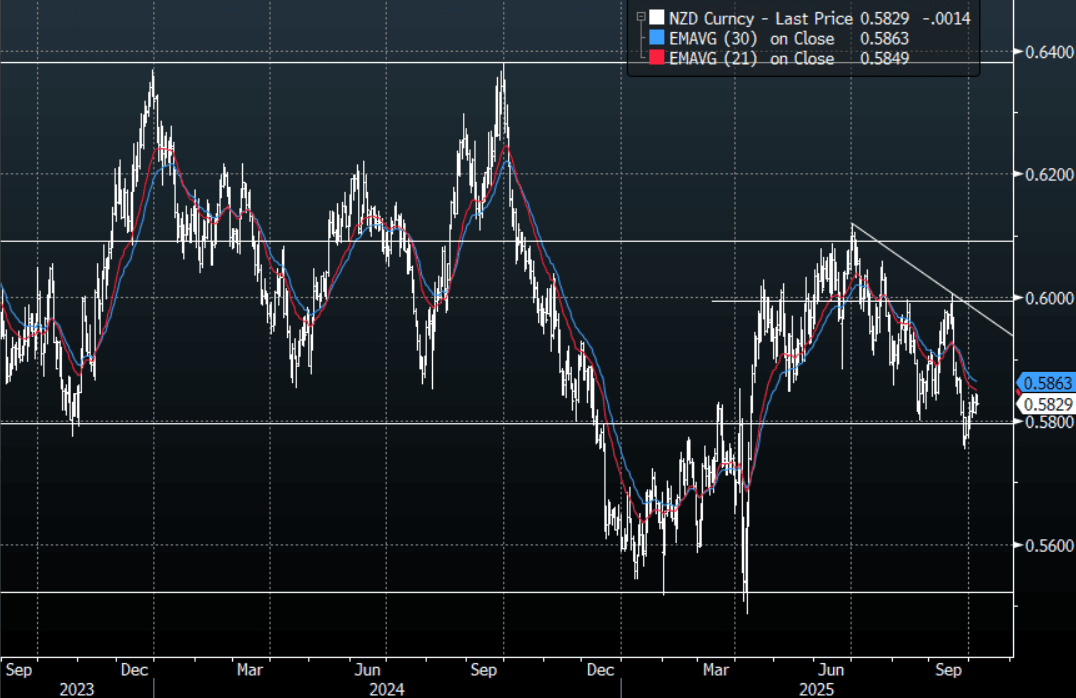

NZD: Asia Wrap - NZD/USD Trades Heavy Toward 0.5850

The NZD/USD had a range of 0.5824 - 0.5843 in the Asia-Pac session, going into the London open trading around 0.5830, -0.25%. US stocks continue to shrug off global politics and the US shutdown, the USD though got a boost from the reaction in USD/JPY. The NZD drifted higher, helped by the way risk continues to push up and probably some NZD/JPY demand as the JPY crosses turn back higher. The first sell zone should be between the 0.5850/0.5900 area for those still wanting to express a short.

- MNI - RBNZ Preview-October 2025: How Much To Ease? After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5820(NZD305m). Upcoming Close Strikes : none - BBG

- AUD/NZD range for the session has been 1.1324 - 1.1354, currently trading around 1.1350. The Cross has seen some selling to cap the move above 1.1400 for now, price action suggests we could potentially see more reversion back to the mean but expect dips back towards 1.1200 to now be supported.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Political Instability Supportive, Tuesday Sees Numerous Fed Speakers

Gold made another record high during Tuesday’s APAC trading despite little change in either the US dollar or yields. Safe-haven flows continue to push bullion towards psychological round number support at $4000 given ongoing government instability in the US, Japan and France. Gold reached $3977.44/oz earlier but then fell to $3956.02. It is currently up 0.3% to $3974.5.

- The US shutdown appears no closer to a resolution although both sides are willing to talk but the issue may be forced as 14 October approaches, when military personnel will miss their first paycheck. Polymarket has higher odds of the shutdown lasting 10-29 days rather than more than 30. The impasse is delaying key US data increasing opacity at a time of economic uncertainty and as the Fed resumes easing.

- With no political group having a majority in the French parliament and an unwillingness to cooperate, instability is likely to continue. The latest PM, Lecornu, resigned on Monday but President Macron has asked him to find a solution. The situation has unsettled markets given France’s high deficit and debt positions.

- Policy under Japan’s new PM Takaichi is also uncertain given her desire to reduce the consumption tax and previous comments against BoJ rate hikes.

- ETF inflows and central bank purchases have driven a $600 upward revision to Goldman Sachs’s end-2026 gold projection to $4900/oz, according to Bloomberg.

- Silver is little changed at $48.55 after reaching $48.653 below Monday’s high of $48.767.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

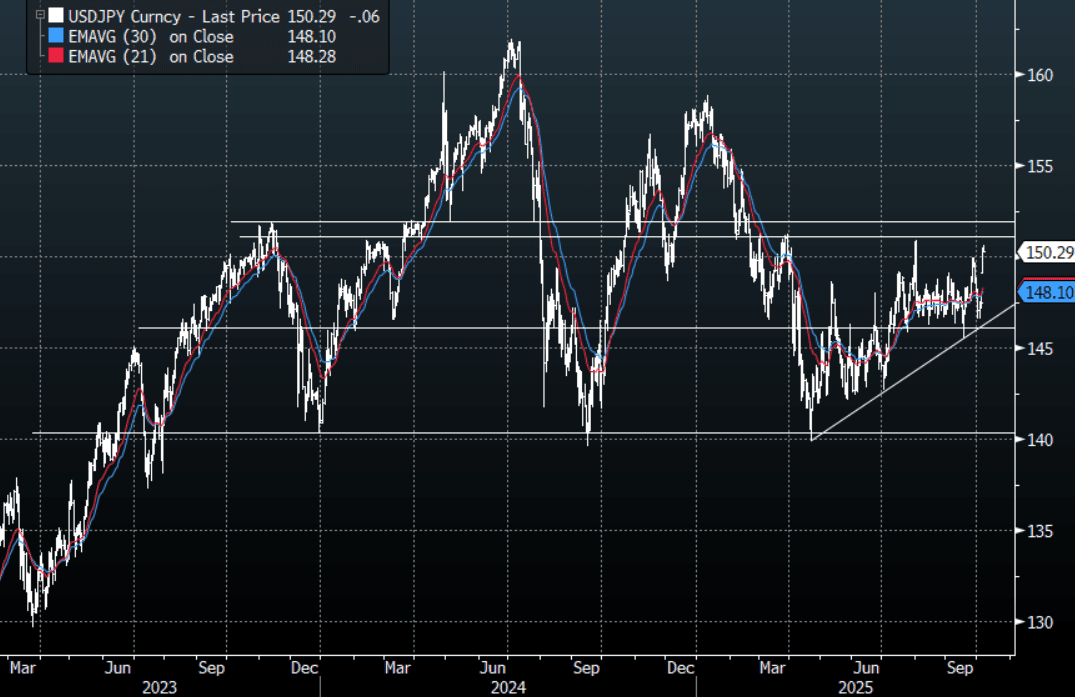

JPY: Asia Wrap - USD/JPY Consolidates Gains Above 150.00

The USD/JPY range has been 150.24 - 150.62 in the Asia-Pac session, it is currently trading around 150.30, -0.03%. The pair looks to be consolidating its gains above 150.00 after the surge higher in reaction to Sanae Takaichi’s victory. The market's attention has quickly returned to a potential looser fiscal and monetary policy on this outcome and looks to be pushing back the likelihood of an imminent rate hike. With risk roaring higher this all feeds further into the carry trade, the focus will now turn toward the pivotal 151/152 area a break of which could potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi’s policies. There was some jaw-boning today about FX moves but realistically I would not expect any action until we cross back above the 155 area.

- The last CFTC data available showed Asset Managers remained significantly long JPY, should these moves begin to gather momentum, they could be forced to first pare back their longs and then if significant levels are broken begin to rebuild JPY shorts. Many crosses are breaking through some pivotal areas(CNH/JPY Above 21.00) and unless the government says something to contradict the markets thinking these could begin to gather momentum.

- MNI - Household Spending Above Forecasts, Supports BoJ Hike Plans : Japan household spending for August was stronger than forecast (+2.3%y/y, versus 1.2% forecast, 1.4% prior). We are below earlier 2025 highs from a y/y momentum standpoint, but the trend has steadily improved from late 2024 lows. It should add, albeit at the margins, to the case for a further BoJ rate hike, although little is priced for the Oct meeting (implied rate of 0.52%, versus a current effective rate of 0.477%).

- "KATO: KEY FOR FX TO MOVE STABLY WHILE REFLECTING FUNDAMENTALS, REFRAINING FROM COMMENTING SPECIFICALLY ON MARKET MOVES" - BBG

- "SUZUKI: CAN'T IGNORE FISCAL DISCIPLINE, CAN'T ACHIEVE JAPAN GROWTH WITHOUT INVESTMENT” - BBG

Options : Close significant option expiries for NY cut, based on DTCC data: 149.75($895m), 150.00($796m), 151.00($776m). Upcoming Close Strikes : 147.00($1.47b Oct 8) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P