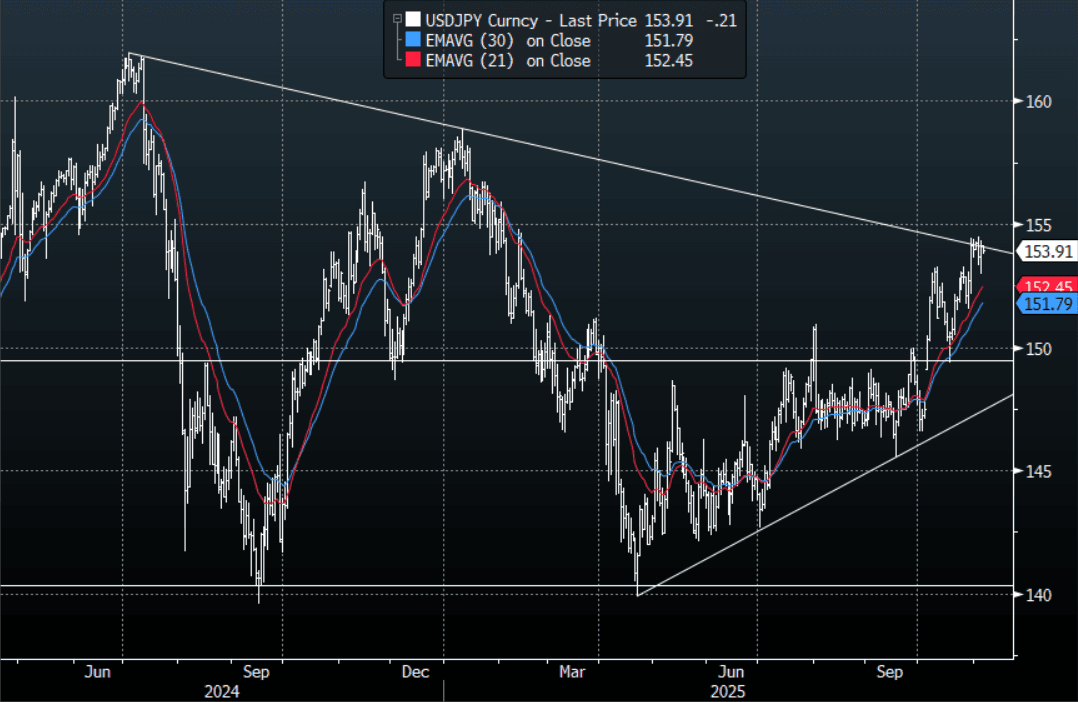

JPY: Asia-Pac: USD/JPY Struggles To Hold Above 154.00

The USD/JPY range today has been 153.80 - 154.36 in the Asia-Pac session, it is currently trading around 153.90, -0.15%. The pair bounced strongly yesterday off the 153.00 area as cross-Yen did an about face as risk recovered paring back losses overnight. A lot depends on what your view is for risk from here, should the price action of the last few days signal that we could be putting in a top and a correction of sorts plays out then I suspect the resistance around the 154/155 area should continue to offer solid resistance. If we see a similar price action to what we have all year and risk just goes straight back to make new all-time highs as we head into the year-end rally then it's highly probable this resistance gives way and we target levels closer to 160.00.

- MNI BRIEF: Japan Sept Real Wages Negative For Ninth Month. Japan’s inflation-adjusted real wages fell 1.4% y/y in September. The data highlight that nominal pay increases continue to lag inflation, leaving households squeezed by high living costs and adding pressure on the government to step up measures against rising prices.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.00($1.14b), 155.00($1.88b), 155.35($1.38b). Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

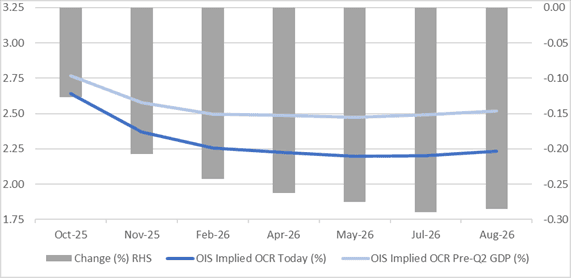

STIR: RBNZ-Dated OIS Holding Post-GDP Softening Ahead Of Tomorrow's Decision

RBNZ-dated OIS pricing closed slightly softer across meetings today, ahead of tomorrow’s RBNZ Policy Decision.

- 36bps of easing is priced for tomorrow’s meeting, with a cumulative 63bps by November 2025.

- Notably, pricing is 13-28bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

OIL: Crude Holds Onto Post-OPEC Gains, US EIA Energy Report Out Later Today

Oil prices have continued their post-OPEC relief rally during today’s APAC session following Monday’s 1.5% rise as it unwinds some of last week’s sharp sell off. The market had worried that the November increase would exceed October’s but in the end it was in line. There was also another strike on a Russian refinery, a trend that may pick up pace as Ukraine tries to impact funds for Russia’s war and it receives more US intelligence.

- WTI moved in a narrow range and is up 0.3% to $61.87/bbl slightly off the intraday high of $61.94. It had fallen to $61.65 early in the session. Brent is 0.3% higher at $65.67/bbl after reaching $65.73.

- The market has been driven by geopolitical developments, especially related to Ukraine-Russia, and excess supply worries, which have diverging effects on oil prices. Later today the EIA short-term energy outlook will be published with the IEA and OPEC’s monthly reports next week.

- The EIA has said that it is continuing its normal schedule for now despite the US shutdown, which also includes its weekly energy data. Industry-based inventories will be released on Tuesday. Stock data remain important as builds are expected as the market shifts into surplus.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

BONDS: NZGBS: Solid & Relative Performance Ahead Of Tomorrow’s RBNZ Decision

NZGBs closed just off session bests, 1-2bps richer, ahead of tomorrow’s RBNZ Policy Decision.

- On a relative basis, NZGBs' performance was even more impressive with the NZ-US and NZ-AU 10-year yields differentials finishing 4bps tighter on the day.

- Cash US tsys are flat in today's Asia-Pac session after yesterday's modest sell-off.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.