BONDS: NZGBS: Bear-Steepener Pushes Curve Towards 2021 Highs

NZGBs closed showing a bear-steepener, with benchmark yields 1-5bps higher.

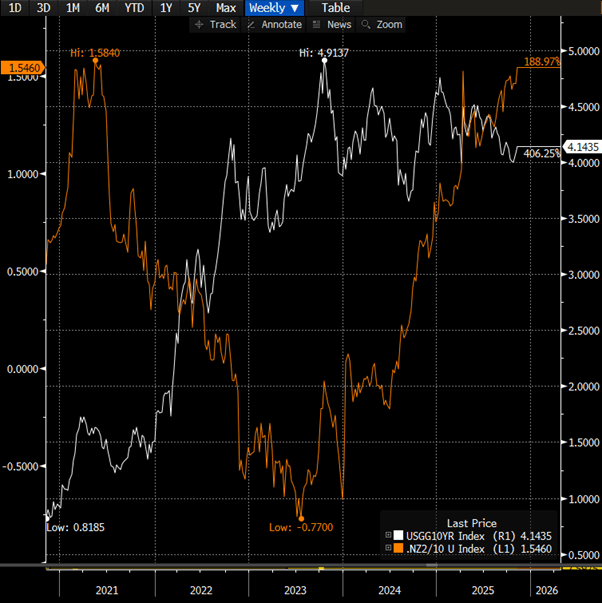

- Today’s move leaves the NZGB 2/10 yield curve at 155bps and near its steepest level since 2021. When the curve was last this steep, the OCR stood at 0.25%, compared with 2.5% today. Although the NZ–US 10-year yield differential is near its 2021 level, the US 10-year yield is now 4.16%, up from 1.65% at that time. (see chart)

- The NZGB 10-year outperformed its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 3bps and 1bps narrower on the day.

- Today’s weekly supply was received with solid demand. Cover ratios ranged from 3.24x (May-54) to 3.97x (Apr-29).

- Swap rates closed 1-4bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed slightly softer across meetings. 28bps of easing is priced for November, with a cumulative 36bps by February 2026.

- Tomorrow, the local calendar will be empty. The next release of note will be the RBNZ's Inflation Expectations data on Tuesday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JPY: USD/JPY Levels Implying Less Import Disinflation Into year End

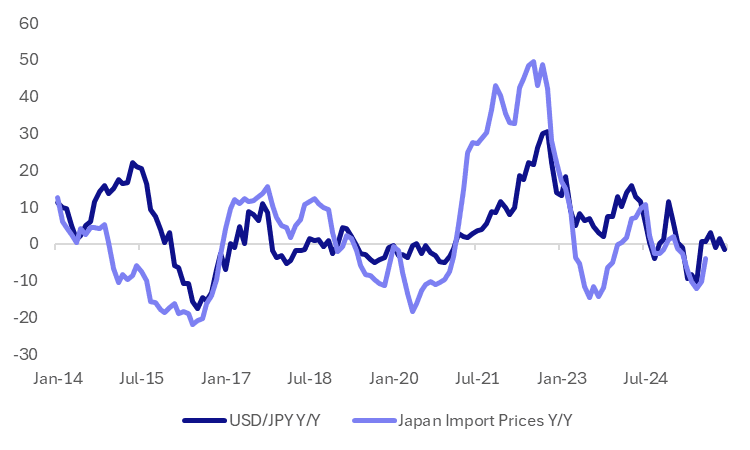

The other point of focus for yen weakness is what it does to the BoJ outlook, as concerns around import price pressures may rise. Given the high end point for USD/JPY at the end of last year (above 157.00), even if USD/JPY continues to rally into year end, the pass through to y/y import price momentum may not be that strong. Still, less deflation impetus from import prices would likely add to the BoJ's tightening case.

- The chart below plots USD/JPY y/y changes against import prices, also in y/y terms. The y/y rate for USD/JPY to the end of 2025 is generating assuming the pair rises 155.00 over this period.

- If these trends are maintained, it does point to the import pulse, which was -3.9%y/y (in August) shifting back closer to flat, or slightly into positive territory over this period. Even if USD/JPY stays around current levels it implies reduced import price y/y falls into year end/early Q1 next year.

- This could add to the case around BoJ tightening bias before year end/early 2026, which the new government led by Takaichi may be more comfortably with (as opposed to a Oct hike this year).

Fig 1: USD/JPY & Import Prices Y/Y (Assuming 155.00 By Year End)

Source: Bloomberg Finance L.P./MNI

JPY: FX Jawboning Returns, But Mkt Concerns May Remain Low At This Stage

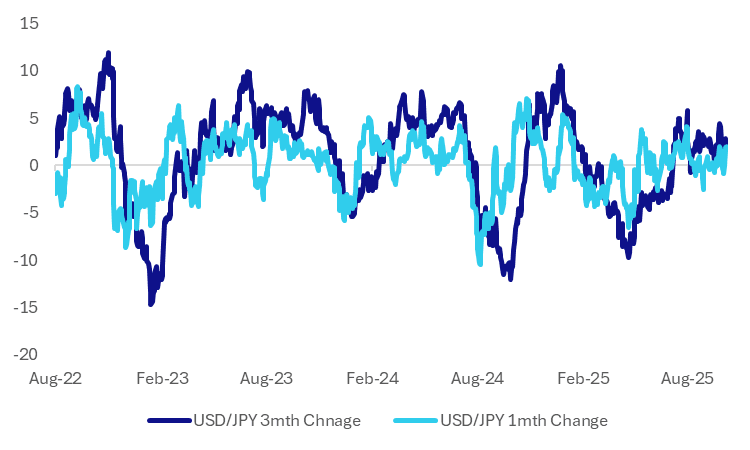

Earlier remarks from Japan FinMin Kato highlight that the recent break higher in USD/JPY hasn't gone unnoticed by the authorities. His remarks around closely watching FX moves and that markets will be monitored closely for excessive and disorderly movements. This is a reminder for markets around FX intervention risks, although as we argue in this bullet it is probably too soon for the market to be significantly concerned by such risks.

- We aren't too far away from spot levels that prevailed in the 2022 intervention episode. However, as the chart below highlights, USD/JPY's 1 month and 3 month rate of change is comfortably below levels that prevailed during this intervention episode and for those in 2024 as well. Both metrics are around +2% firmer, which is elevated but well within historical norms.

- We saw earlier that USD/JPY reacted little to the stronger household spending print. While not a tier one release, it speaks to the market comfort that a BOJ hike is likely to be off agenda in the near term.

- More broadly, with global risk appetite very well supported, this all feeds further into the carry trade.; The focus will now turn toward the pivotal 151/152 area a break of which will potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi's policies.

- The over caveat is that USD/JPY looks too high relative to US-JP yield differentials, which may become a headwind if we test into the 151-152 area.

Fig 1: USD/JPY 1mth & 3mth Rate Of Change - Within Historical Norms

Source: Bloomberg Finance L.P./MNI

JGBS AUCTION: Relief Rally Post-30Y Auction

The 30-year JGB auction delivered mixed results. The low price fell short of dealer expectations of 99.15, per the Bloomberg survey. However, the cover ratio increased to 3.4110x from 3.30806x. On the other hand, the auction tail shortened to 0.17 from 0.18, indicating an improvement in bidding strength.

- Today’s result is an improvement versus the 10-year auction earlier this month, which demonstrated weak demand metrics.

- As highlighted in our preview, today's issuance arrived with an outright yield at a new cycle high of 3.351%, approximately 10bps higher than last month’s issuance.

- The 30-year yield has rallied strongly following the result, suggesting that the recent bear-steepening was overdone. Although newly elected Liberal Democratic Party leader Sanae Takaichi is perceived to have an expansionary fiscal and monetary policy stance, a lot of these expectations appear to have already been priced into the market.