US TSYS: Rate Up With US$ Recovery on Fed Chair Nomination: Kevin Warsh

Jan-30 20:28

- Treasuries look to finish mixed, curves twisting steeper with 2s-5s outperforming weaker 10s-30s by the bell. Rather decent volumes (TYH6 over 2.1M) as markets price in Pres Trumps nomination for Fed Chairman: Kevin Warsh, with multiple Fed speakers fresh out of Blackout voicing their opinion on policy.

- TYH6 is currently -1 at 111-26.5 (111-17.5 low / 111-28 high), Initial firm resistance to watch is at the 20-day EMA, currently at 111-31+. The 50-day EMA is at 112-09. The area between the 20- and 50-day averages represents a key resistance zone.

- Fed Gov Miran initmated a lot of Warsh's views "are really right". Miran had dissented against this week's rate hold in favor of a 25bp cut (smaller than the 50bp he called for at the prior 3 meetings) - continued to argue for easier policy in a CNBC appearance Friday.

- St Louis Fed's Musalem (not a 2026 FOMC voter but a hawkish-leaning member) on Friday echoed comments he made prior to the December meeting in suggesting that it would be "unadvisable" to cut rates at this time. That said, if the data were to align, then he is open to the possibility of cuts in future.

- Warsh's nominated, not confirmed: Republican Senator Tillis - said he'd block any Trump Fed nominees until the Powell/Fed DOJ investigation is resolved - reiterated that position in a post on X.com: "Kevin Warsh is a qualified nominee with a deep understanding of monetary policy. However, I will oppose the confirmation of any Federal Reserve nominee, including for the position of Chairman, until the DOJ’s inquiry into Chairman Powell is fully and transparently resolved."

- PPI details offered a slightly stronger readthrough to core PCE inflation for December than was the case in November. Our best guess is that analysts will continue to expect core PCE inflation around 0.4% M/M in Dec after the 0.16% M/M in Nov (potentially revised up marginally).

- Cross-Asset update: Friday's broad rally in the US dollar (BBDXY +9.55 at 1187.45) prompted as extreme sell-off in metals prices, particularly precious metals which have plunged sharply: Spot gold fell to a low of $4,690/oz in recent trade, down more than $700 on the day, before bouncing slightly.

- Look ahead: US ISM Manufacturing PMI data will take focus on Monday, while markets will be attentive to developments over the US government shutdown and any potential comments from both Fed’s Powell and Warsh ahead. The employment report for January next Friday.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

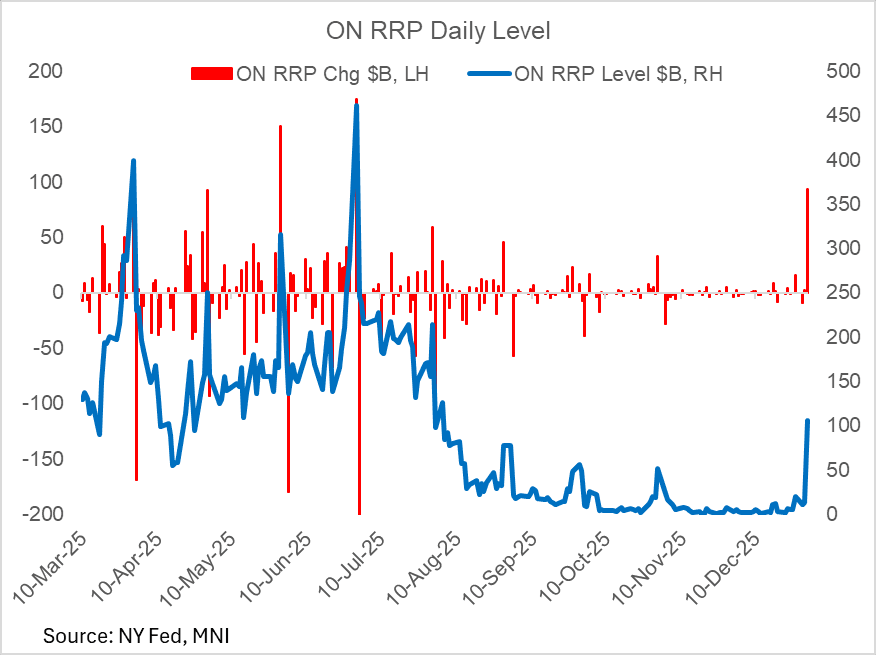

US TSYS/OVERNIGHT REPO: ON RRP Soars At Year-End, Well Below Prior Year's Level

Dec-31 18:22

Month-/quarter-/year-end brings a jump in Fed reverse repo takeup, to $106.0B. The $93B jump from the prior session is the biggest since May's $150B; the level is the highest since August.

- Of course, this is due to reverse sharply in coming sessions, and the takeup level is far below the $473B seen at year-end 2024.

US TSYS: Volume Jumps Into Year End

Dec-31 18:14

A 6+ tick dip in TYH6 accompanies the CME floor close for the New Year's holiday, to a session-low 112-10+ (a level last seen on Dec 24).

- After light volumes throughout the morning, a burst of around 400k contracts trade into the month end to a daily volume of 1.13M.

- Prices are stabilizing (last 112-12+), though as we noted earlier, from a technical perspective 111-29 would confirm a resumption of the bear cycle.

- SIFMA recommends a cash close at 2pm ET; Globex is open until 4pm ET.

US TSYS: Wrapping Up 2025

Dec-31 17:48

- Treasuries reversed early support after the final weekly claims data for 2025 came out lower than expected Wednesday, rather a decent range on moderate volumes ahead of the early close for the New Year's Eve holiday (1300ET; 1600ET Globex), re-open/electronic trade Thursday evening for Friday's order of business.

- TYH6 currently trades 112-17 (-3.5) vs. 112-14 low, curves mixed: 2s10s +.738 at 67.887, 5s30s -.890 at 111.961.

- The technical trend theme remains bearish and a break of 111-29 would confirm a resumption of the bear cycle. This would open 111-19, a Fibonacci projection. Key short-term resistance has been defined at 112-31, the Dec 18 high, where a break would undermine a bear theme and signal scope for a stronger recovery instead.

- Treasury yields slipped overnight in reaction to additional tariffs on beef by China: the US will have to pay 55% additional tariffs on beef exports to China, above its specified quota (164k tons a year in 2026). 10Y yield tapped a low of 4.1024% before climbing to 4.1513% high following the jobless claims data.

- Initial jobless claims for the Dec 27 week were much lower than expected at 199k, vs the 218k consensus (215k prior rev from 214k). This marked the lowest level of seasonally-adjusted initial claims since the Nov 29 week, though it is for that reason that we suggest caution: both are holiday weeks (the other is Thanksgiving) which typically translates into volatility in claims.

- Meanwhile continuing claims for the Dec 20 week came in at 1,866k (1,902k consensus, 1,913k prior rev from 1,923k), marking a 3-week low but still in the recent ranges. NSA claims dropped 103k to 1,881k, and like initial, we would expect a large pickup the following week.

Trending Top

Apr-03 08:04

Apr-02 19:04