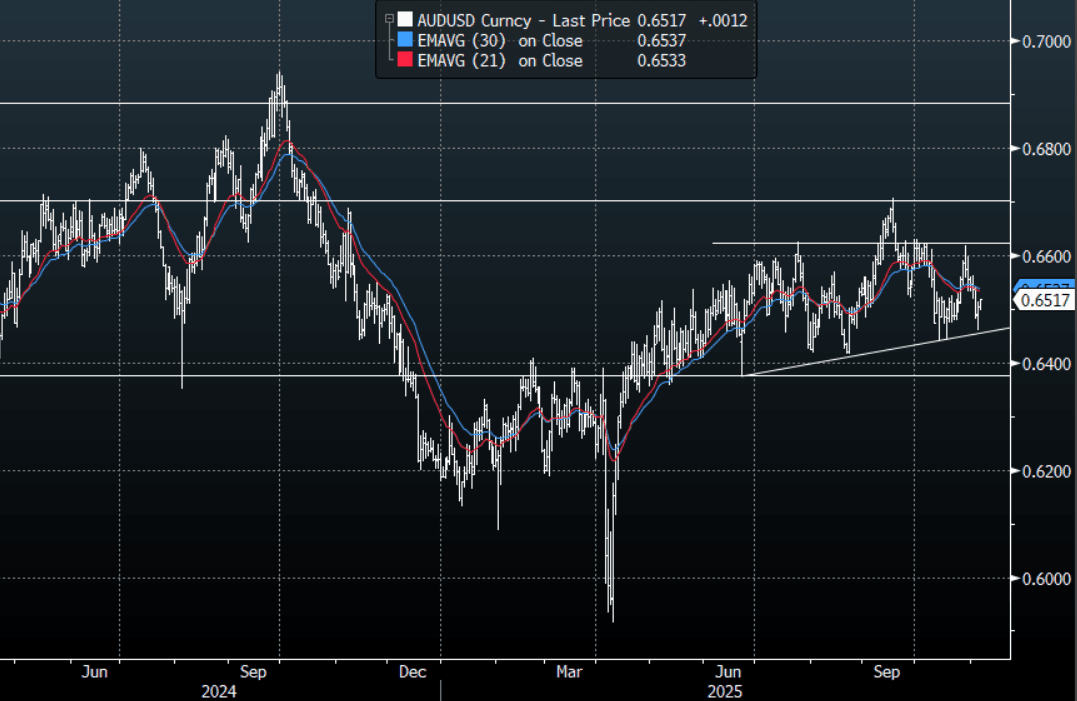

AUD: Asia-Pac: AUD/USD Recovers Back Above 0.6500

The AUD/USD has had a range today of 0.6497 - 0.6517 in the Asia- Pac session, it is currently trading around 0.6515, +0.20%. Was that it ? The dip buyers in risk look once again to be in control and what looked like the start of a correction has quickly petered out. The AUD/USD finds itself back in the middle of its now familiar range, having chopped sideways between 0.6350-0.6650 since April this year. A lot rides on how risk trades from here, should this potential correction lower play out then the USD should again come to the fore, but if that was the extent of the correction and we start building toward a year end rally for risk assets then the AUD can again start to outperform. The pivot for the AUD is around 0.6550, above there and we start to turn toward the top of the range again.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6490(AUD487m), 0.6550(AUD 479m), 0.6600(AUD567m). Upcoming Close Strikes : 0.6450(AUD544m Nov 11), 0.6500(AUD1.02b Nov 7), 0.6600(AUD682m Nov 7)- BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Solid & Relative Performance Ahead Of Tomorrow’s RBNZ Decision

NZGBs closed just off session bests, 1-2bps richer, ahead of tomorrow’s RBNZ Policy Decision.

- On a relative basis, NZGBs' performance was even more impressive with the NZ-US and NZ-AU 10-year yields differentials finishing 4bps tighter on the day.

- Cash US tsys are flat in today's Asia-Pac session after yesterday's modest sell-off.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.

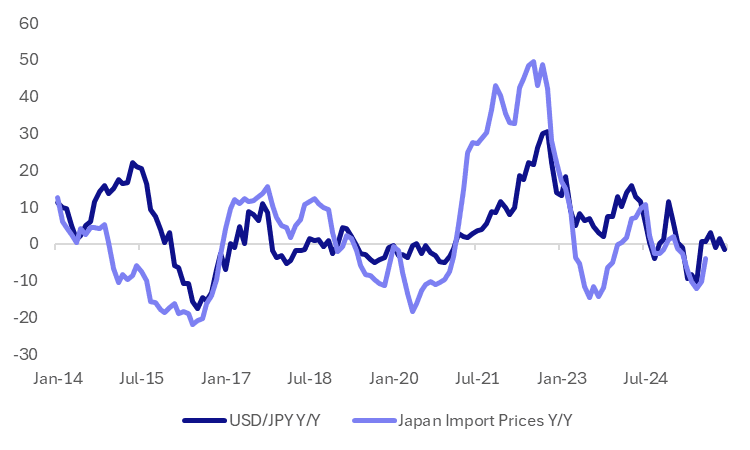

JPY: USD/JPY Levels Implying Less Import Disinflation Into year End

The other point of focus for yen weakness is what it does to the BoJ outlook, as concerns around import price pressures may rise. Given the high end point for USD/JPY at the end of last year (above 157.00), even if USD/JPY continues to rally into year end, the pass through to y/y import price momentum may not be that strong. Still, less deflation impetus from import prices would likely add to the BoJ's tightening case.

- The chart below plots USD/JPY y/y changes against import prices, also in y/y terms. The y/y rate for USD/JPY to the end of 2025 is generating assuming the pair rises 155.00 over this period.

- If these trends are maintained, it does point to the import pulse, which was -3.9%y/y (in August) shifting back closer to flat, or slightly into positive territory over this period. Even if USD/JPY stays around current levels it implies reduced import price y/y falls into year end/early Q1 next year.

- This could add to the case around BoJ tightening bias before year end/early 2026, which the new government led by Takaichi may be more comfortably with (as opposed to a Oct hike this year).

Fig 1: USD/JPY & Import Prices Y/Y (Assuming 155.00 By Year End)

Source: Bloomberg Finance L.P./MNI

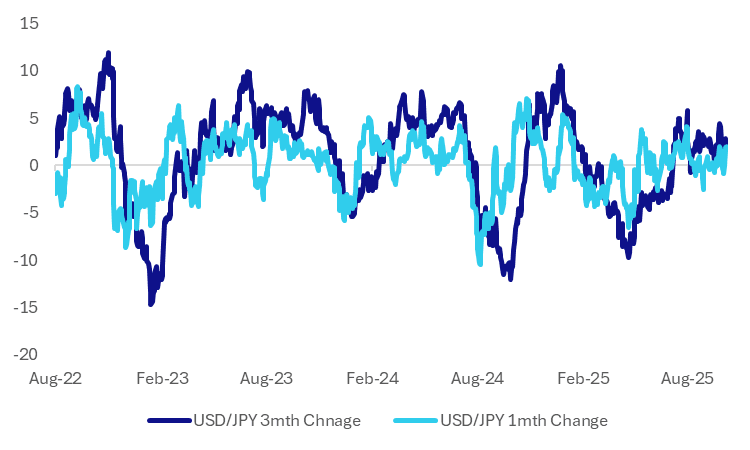

JPY: FX Jawboning Returns, But Mkt Concerns May Remain Low At This Stage

Earlier remarks from Japan FinMin Kato highlight that the recent break higher in USD/JPY hasn't gone unnoticed by the authorities. His remarks around closely watching FX moves and that markets will be monitored closely for excessive and disorderly movements. This is a reminder for markets around FX intervention risks, although as we argue in this bullet it is probably too soon for the market to be significantly concerned by such risks.

- We aren't too far away from spot levels that prevailed in the 2022 intervention episode. However, as the chart below highlights, USD/JPY's 1 month and 3 month rate of change is comfortably below levels that prevailed during this intervention episode and for those in 2024 as well. Both metrics are around +2% firmer, which is elevated but well within historical norms.

- We saw earlier that USD/JPY reacted little to the stronger household spending print. While not a tier one release, it speaks to the market comfort that a BOJ hike is likely to be off agenda in the near term.

- More broadly, with global risk appetite very well supported, this all feeds further into the carry trade.; The focus will now turn toward the pivotal 151/152 area a break of which will potentially start another leg higher. Expect dips to now find support unless there is push back on the market's views of Takaichi's policies.

- The over caveat is that USD/JPY looks too high relative to US-JP yield differentials, which may become a headwind if we test into the 151-152 area.

Fig 1: USD/JPY 1mth & 3mth Rate Of Change - Within Historical Norms

Source: Bloomberg Finance L.P./MNI