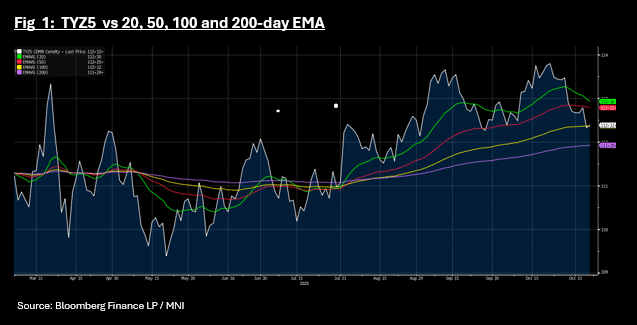

US TSYS: TYZ5 Back Above Key Tech Level

The overnight rally was sustained in Asia today with bond futures all up, albeit modestly. The 10-Yr TYZ5 is up +03 to 112-13+ in a low volume day, having trended below the 100-day EMA overnight. The rally today takes the 10-Yr back above the 100-day EMA.

Risk appetite in the Asia trading day was strong with regional bourses posting solid gains. Bonds got a bid also given the re-pricing overnight and cash down up to 1-2bps across the curve.

- The 2-Yr fell -1.2bps to 3.621%

- The 5-Yr is down -1.4bps to 3.751%

- The 10-Yr is down -1.6bps to 4.145%

- The 30-yr declined -1bps to 4.73%

The focus for issuance tonight is a US$110bn 4-week bill and a US$95bn 8-week bill auction.

Data releases are delayed tonight instead will have Fed Speakers Barr, Williams and Hammack.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Tech Related Plays Continue To Rally, Thailand Up Ahead Of BoT

Regional equity markets are still disrupted by holidays with China and South Korea remaining out, while Hong Kong markets are also out today. For those markets which are open, the tone is mostly positive, particularly tech sensitive plays. The on-going rally in US tech related indices amid AI/chip related gains is a positive for the region. The SOX rose 2.89% in Monday US trade, as AMD, the chip maker, announced a deal with OpenAI.

- Japan markets are tracking higher, with the NKY 225 up a further 0.75%, while the Topix is up 0.40%. There have been lots of headlines today, as the government looks to provide of cost of living relief but is also mindful of fiscal constraints (high debt to GDP the country faces). We also had stronger than expected household spending data, while FinMin Kato jawboned recent FX weakness. USD/JPY is little changed at this stage.

- The Topix Transport sub index is up a further 1.05%, while the banks index is down 0.49% (following yesterday's 1.89%). Incoming advisors to new PM Takaichi stated an Oct hike could be too soon for the BoJ.

- The Taiex index in Taiwan is up close to 2%, the fresh record highs. Chip bellwether TSMC continues to surge in local trade.

- In South East Asia the nest performer is Thailand up over 1.4%. This puts the index back above the 1300 level, back close to mid Sep highs. We ahve the BoT meeting tomorrow, where a rate cut is expected. Via the Bangkok Post: "The first set of measures focuses on simplifying initial public offering (IPO) rules to streamline listing procedures, reduce regulatory barriers and make the Thai market more competitive compared with regional peers." (announced by a Capital market taskforce) is also potentially helping sentiment.

- Other markets in the region are higher, although Malaysia is a laggard, down around 0.75%.

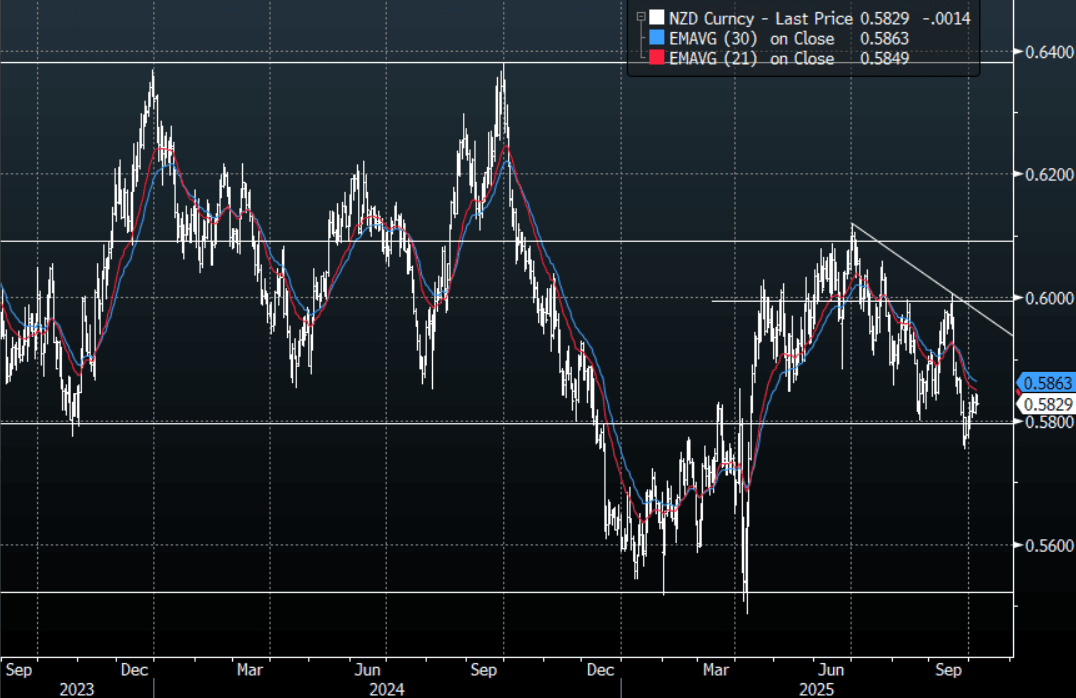

NZD: Asia Wrap - NZD/USD Trades Heavy Toward 0.5850

The NZD/USD had a range of 0.5824 - 0.5843 in the Asia-Pac session, going into the London open trading around 0.5830, -0.25%. US stocks continue to shrug off global politics and the US shutdown, the USD though got a boost from the reaction in USD/JPY. The NZD drifted higher, helped by the way risk continues to push up and probably some NZD/JPY demand as the JPY crosses turn back higher. The first sell zone should be between the 0.5850/0.5900 area for those still wanting to express a short.

- MNI - RBNZ Preview-October 2025: How Much To Ease? After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October. The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. 36bps of easing is priced for Wednesday’s meeting, with a cumulative 63bps by November 2025.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5820(NZD305m). Upcoming Close Strikes : none - BBG

- AUD/NZD range for the session has been 1.1324 - 1.1354, currently trading around 1.1350. The Cross has seen some selling to cap the move above 1.1400 for now, price action suggests we could potentially see more reversion back to the mean but expect dips back towards 1.1200 to now be supported.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Political Instability Supportive, Tuesday Sees Numerous Fed Speakers

Gold made another record high during Tuesday’s APAC trading despite little change in either the US dollar or yields. Safe-haven flows continue to push bullion towards psychological round number support at $4000 given ongoing government instability in the US, Japan and France. Gold reached $3977.44/oz earlier but then fell to $3956.02. It is currently up 0.3% to $3974.5.

- The US shutdown appears no closer to a resolution although both sides are willing to talk but the issue may be forced as 14 October approaches, when military personnel will miss their first paycheck. Polymarket has higher odds of the shutdown lasting 10-29 days rather than more than 30. The impasse is delaying key US data increasing opacity at a time of economic uncertainty and as the Fed resumes easing.

- With no political group having a majority in the French parliament and an unwillingness to cooperate, instability is likely to continue. The latest PM, Lecornu, resigned on Monday but President Macron has asked him to find a solution. The situation has unsettled markets given France’s high deficit and debt positions.

- Policy under Japan’s new PM Takaichi is also uncertain given her desire to reduce the consumption tax and previous comments against BoJ rate hikes.

- ETF inflows and central bank purchases have driven a $600 upward revision to Goldman Sachs’s end-2026 gold projection to $4900/oz, according to Bloomberg.

- Silver is little changed at $48.55 after reaching $48.653 below Monday’s high of $48.767.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.