AUSSIE BONDS: Heavy Session As Market Digests A Cautious RBA

ACGBs (YM -4.5 & XM -6.0) are weaker and at or near session cheaps.

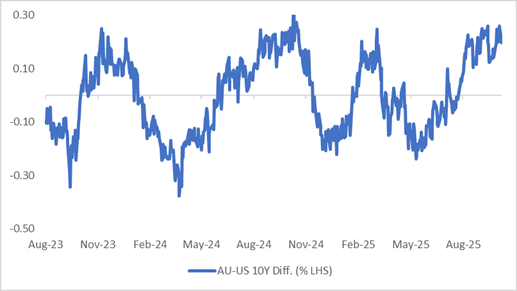

- Cash ACGBs are 4-5bps cheaper with the AU-US 10-year yield differential at +22bps. At this level, the spread has recoiled from the upper end of the 30bps range that has persisted since November 2022. (see chart)

- MNI RBA Review: The RBA Monetary Policy Board unanimously left rates at 3.6%, as was widely expected, and sounded generally cautious. Staff trimmed mean projections were revised higher over the rest of 2025 and 2026, with the important 2q/2q annualised rate returning to 3% in Q1 and 2.6% in Q4, which may allow a rate cut from May if this eventuates. Decisions remain highly data-dependent. (see link)

- The bills strip is weaker, with pricing -2 to -4 across contracts.

- RBA-dated OIS pricing is little changed following this week’s RBA Policy Decision. RBA-dated OIS pricing is showing a 25bp rate cut in December at a 10% probability, with a cumulative 18bps of easing priced by mid-2026. Notably, current pricing leaves levels some 22-26bps firmer than pre-Q3 CPI levels in late October.

- Tomorrow, the local calendar will see Foreign Reserves.

- The AOFM plans to sell A$800mn of the 3.00% 21 November 2033 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

STIR: RBNZ-Dated OIS Holding Post-GDP Softening Ahead Of Tomorrow's Decision

RBNZ-dated OIS pricing closed slightly softer across meetings today, ahead of tomorrow’s RBNZ Policy Decision.

- 36bps of easing is priced for tomorrow’s meeting, with a cumulative 63bps by November 2025.

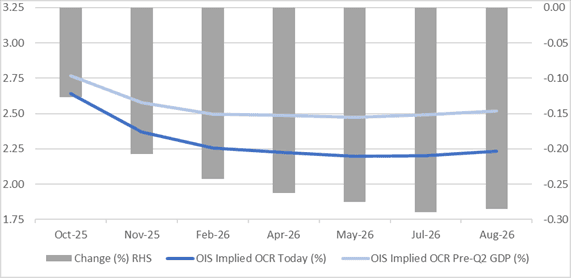

- Notably, pricing is 13-28bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

OIL: Crude Holds Onto Post-OPEC Gains, US EIA Energy Report Out Later Today

Oil prices have continued their post-OPEC relief rally during today’s APAC session following Monday’s 1.5% rise as it unwinds some of last week’s sharp sell off. The market had worried that the November increase would exceed October’s but in the end it was in line. There was also another strike on a Russian refinery, a trend that may pick up pace as Ukraine tries to impact funds for Russia’s war and it receives more US intelligence.

- WTI moved in a narrow range and is up 0.3% to $61.87/bbl slightly off the intraday high of $61.94. It had fallen to $61.65 early in the session. Brent is 0.3% higher at $65.67/bbl after reaching $65.73.

- The market has been driven by geopolitical developments, especially related to Ukraine-Russia, and excess supply worries, which have diverging effects on oil prices. Later today the EIA short-term energy outlook will be published with the IEA and OPEC’s monthly reports next week.

- The EIA has said that it is continuing its normal schedule for now despite the US shutdown, which also includes its weekly energy data. Industry-based inventories will be released on Tuesday. Stock data remain important as builds are expected as the market shifts into surplus.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.

BONDS: NZGBS: Solid & Relative Performance Ahead Of Tomorrow’s RBNZ Decision

NZGBs closed just off session bests, 1-2bps richer, ahead of tomorrow’s RBNZ Policy Decision.

- On a relative basis, NZGBs' performance was even more impressive with the NZ-US and NZ-AU 10-year yields differentials finishing 4bps tighter on the day.

- Cash US tsys are flat in today's Asia-Pac session after yesterday's modest sell-off.

- After Q2 GDP fell 0.9% q/q, more than the RBNZ’s -0.3% projected in August, expectations of a 50bp rate cut increased. Now 10 out of 25 analysts surveyed by Bloomberg are forecasting 50bp of easing on 8 October.

- The weaker GDP print means that there was more excess capacity in the economy than the RBNZ assumed in August, but the data are prone to large revisions and so it may want to stick to the 25bp rate cuts for October and November signalled in August.

- Two MPC members voted for a 50bp rate cut at the last meeting, but recent and upcoming personnel changes on the committee add to the uncertainty around the October decision. (See MNI RBNZ Preview here)

- RBNZ dated OIS pricing closed slightly softer across meetings. 36bps of easing is priced for tomorrow, with a cumulative 63bps by November 2025.