GOLD: Gold Slightly Higher But Still In Range, Will Watch Upcoming Fed Speakers

Gold prices are moderately higher in Thursday’s APAC session supported by a softer US dollar (BBDXY -0.1%) and slightly lower yields. The chance of a December Fed rate cut has also risen also boosting non-interest bearing bullion. The market has been range trading this week driven by uncertainty over the outlook for the next Fed decision. Gold is up 0.2% to $3987.0 today off the high of $3990.43.

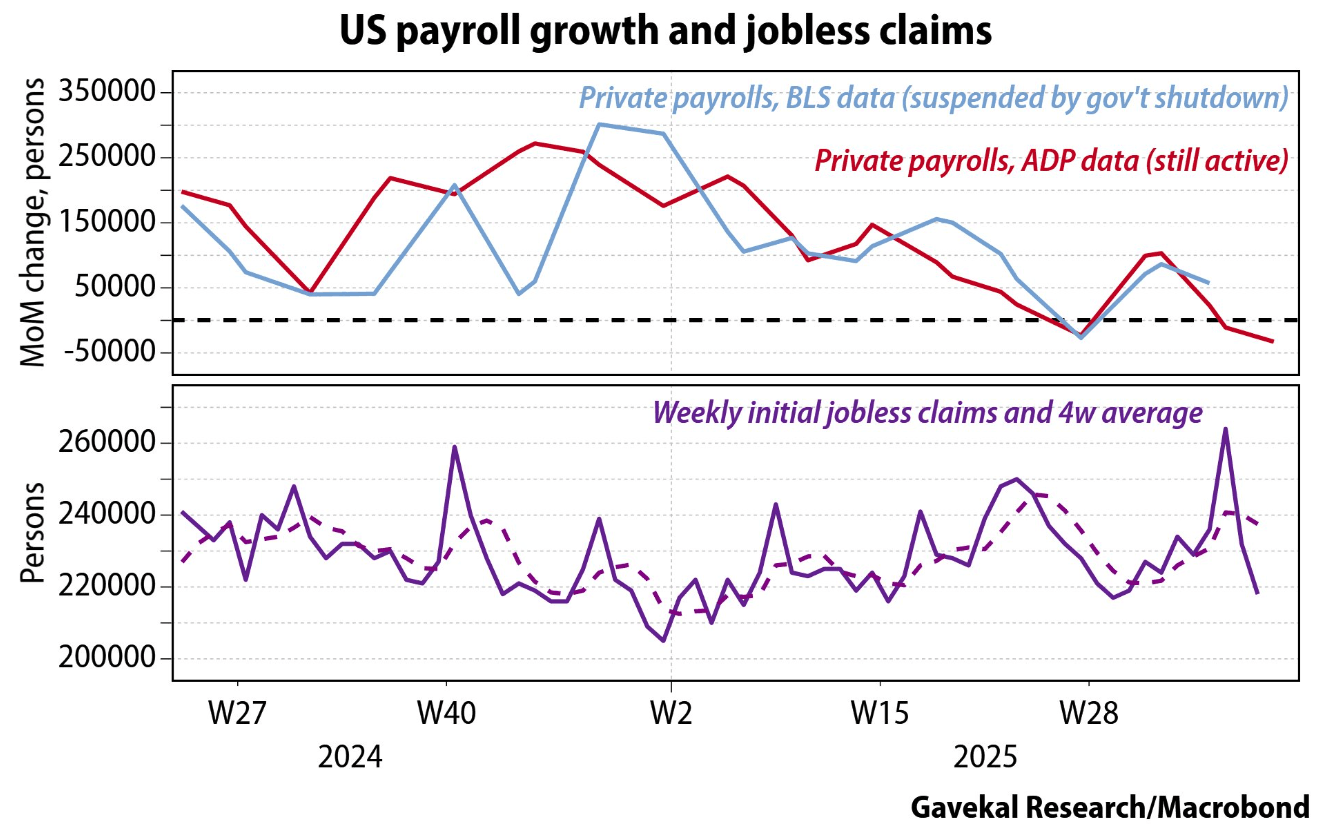

- With US data scarce due to the government shutdown, ADP October employment was watched closely. With a 42k rise after two consecutive falls, it signalled that the labour market remains soft but may have stabilised. Looking forward, the swathe of Fed speakers on Thursday will be monitored for thinking regarding upcoming decisions.

- Silver is 0.5% higher at $48.24 after reaching $48.263 following a low of $47.738. Like gold it has traded between resistance at $49.456, 23 October high, and support at $46.089, 50-day EMA. The trend in the metal remains bullish and any declines are considered corrective.

- Equities are generally stronger with the Nikkei up 1.4% and CSI 300 +1.3% but S&P e-mini flat. Oil prices are higher with WTI +0.4% to $59.86/bbl. Copper is up 0.6%.

- Later there are numerous Fed speakers including Williams, Barr, Hammack, Waller, Paulson and Musalem. The ECB’s Schnabel, de Guindos, Buch and Lane also speak. The BoE is expected to be on hold. US October Challenger job cuts are likely to be monitored closely given October payrolls will be delayed due to the government shutdown. Also German September IP, euro area September retail sales, Q3 French payrolls and October UK construction PMI print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Yields Unchanged In A Quiet Session

The TYZ5 range has been 112-12+ to 112-15 during the Asia-Pacific session. It last changed hands at 112-14, up 0-01+ from the previous close.

- The US 2-year yield is trading 3.586%.

- The US 10-year yield is trading around 4.15%.

- 10-Year yields bounced on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade the move higher.

- Bloomberg - “Global Long Bonds Can Breathe Easier After 30-Year JGB Sale. Japan’s thirty-year auction went off smoothly with a higher bid-to-cover ratio than the previous sale, which will be a relief for investors across G-10 long-term debt. Traders will also be reassured with MUFJ-MS taking up the biggest slice of the bonds, along with Japan’s other big primary dealers.”

Gavekal on X: “With the Bureau of Labor Statistics temporarily dark due to the US government shutdown, investors and the Federal Reserve must rely on other employment data. Worryingly, ADP’s private payroll estimate showed its most significant contraction of this cycle. That could be the result of the immigration crackdown reducing the supply of available workers. It is also possible that slack is starting to appear in the labor market, perhaps due to the temporary fiscal contraction from tariffs or AI causing unemployment, especially among young graduates. The recent decline in jobless claims is encouraging, but it is worth noting that many young graduates do not have prior work history and thus may not be eligible to claim unemployment benefits.” See Graph Below.

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

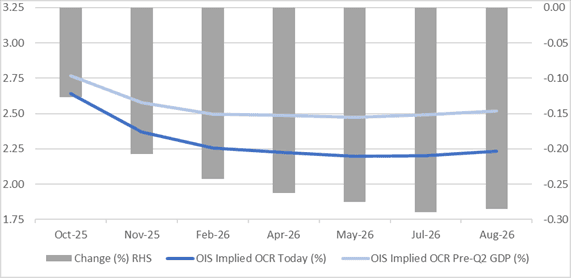

STIR: RBNZ-Dated OIS Holding Post-GDP Softening Ahead Of Tomorrow's Decision

RBNZ-dated OIS pricing closed slightly softer across meetings today, ahead of tomorrow’s RBNZ Policy Decision.

- 36bps of easing is priced for tomorrow’s meeting, with a cumulative 63bps by November 2025.

- Notably, pricing is 13-28bps softer across meetings versus 18 September’s pre-Q2 GDP levels.

- Both the production and expenditure-based GDP measures fell 0.9% q/q in Q2, the weakest since the pandemic. The RBNZ had expected a 0.3% q/q decline.

Figure 1: RBNZ Dated OIS Current vs. Pre-Q2 GDP (%)

Source: Bloomberg Finance LP / MNI

OIL: Crude Holds Onto Post-OPEC Gains, US EIA Energy Report Out Later Today

Oil prices have continued their post-OPEC relief rally during today’s APAC session following Monday’s 1.5% rise as it unwinds some of last week’s sharp sell off. The market had worried that the November increase would exceed October’s but in the end it was in line. There was also another strike on a Russian refinery, a trend that may pick up pace as Ukraine tries to impact funds for Russia’s war and it receives more US intelligence.

- WTI moved in a narrow range and is up 0.3% to $61.87/bbl slightly off the intraday high of $61.94. It had fallen to $61.65 early in the session. Brent is 0.3% higher at $65.67/bbl after reaching $65.73.

- The market has been driven by geopolitical developments, especially related to Ukraine-Russia, and excess supply worries, which have diverging effects on oil prices. Later today the EIA short-term energy outlook will be published with the IEA and OPEC’s monthly reports next week.

- The EIA has said that it is continuing its normal schedule for now despite the US shutdown, which also includes its weekly energy data. Industry-based inventories will be released on Tuesday. Stock data remain important as builds are expected as the market shifts into surplus.

- Later the Fed’s Bostic, Bowman, Miran and Kashkari as well as the ECB’s Lagarde and Machado speak. September NY Fed 1-year inflation expectations and August Germany factory orders are released.