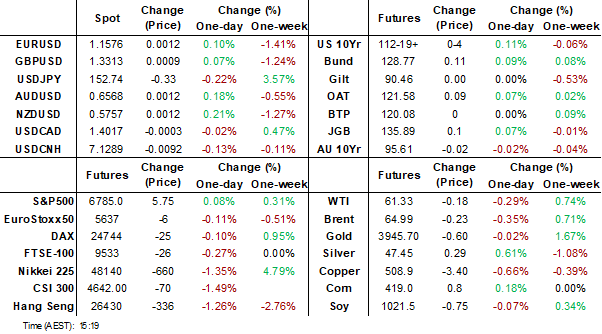

MNI EUROPEAN MARKETS ANALYSIS: USD Trims Thursday Gains

- Japan's FinMin ramped up FX rhetoric but the comments didn't suggest FX intervention was imminent. USD/JPY sits back under 153.00. The USD is a touch softer elsewhere, while US yields are little changed. Earlier Japan PPI data was a touch above forecasts.

- Commodities are mostly weaker, with gold holding under $4000. Regional equities are being led lower by the tech side. Some markets are correcting from overbought levels.

- Looking ahead, we have Norway CPI, Canadian jobs data and in the US the U. of Mich consumer sentiment print.

MARKETS

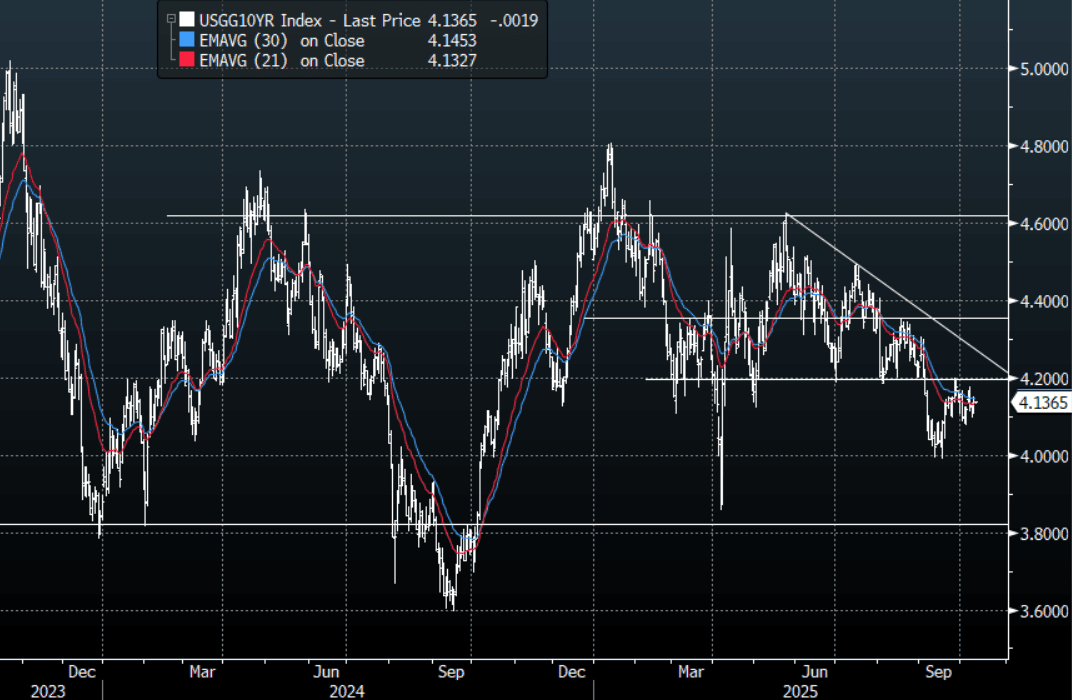

US TSYS: Asia-Pac: Front-End Yields Drift Slightly Lower

The TYZ5 range has been 112-16+ to 112-18+ during the Asia-Pacific session. It last changed hands at 112-18, up 0-02+ from the previous close.

- 10-Year yields continue to consolidate just above 4.10% but remain subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around the 4.20% area initially and look to fade any move higher for now.

- The US 10-year yield is trading around 4.137%.

- The US 2-year yield has edged lower trading 3.588%, down 0.01 from its close.

- “LABOR DEPT'S BLS AIMING TO RELEASE SEPT CPI DATA BY MONTH'S END” - BBG

With Labour data at a premium after NFP was delayed, “Neil Dutta, Head of Economics at @RenMacLLC, told the Schwab Network that there could be fewer construction workers employed, as homebuilders are "a little bit bloated in terms of their labor relative to what they're doing." He said the job losses can be substantial, adding that the slight drop in mortgage rates "hasn't really stoked" homebuyer activity.” - Schwab Network on X.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

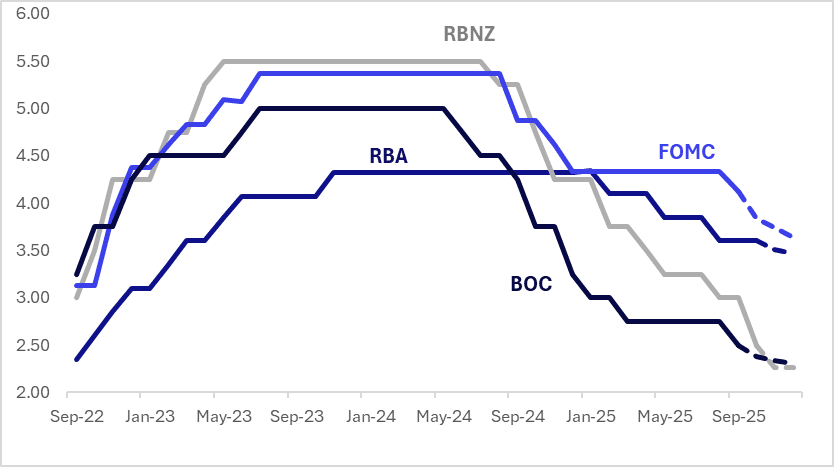

STIR: $-Bloc Pricing Little Changed Over Past Week, Except For NZ

Interest rate expectations across the $-bloc have shown little net change over the past week, except in NZ, which softened sharply (-12bps) following the RBNZ’s 50bp cut.

- All RBNZ board members agreed that the 50bp to 2.5% was appropriate given material spare capacity in the economy. As this negative output gap is likely to persist for some time and the economic recovery remains lacklustre, further cuts bringing policy into stimulatory territory are likely.

- The meeting record stated that the Committee remains open to further reductions in the OCR” – note the plural in “reductions”. Thus, with the recovery being lacklustre in Q3 and unlikely to surprise in Q4, another rate cut in November seems likely.

- How the economy develops before the next meeting in February will determine if more stimulus is needed. Still, it will also be the first decision with new Governor Breman at the helm.

- Looking ahead, the next key regional events are the FOMC and BOC policy decisions on October 29. Market pricing currently implies a 95% probability of a 25bps cut by the Fed and a 57% chance of easing by the BOC.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing are as follows: US (FOMC): 3.64%, -48bps; Canada (BOC): 2.30%, -20bps; Australia (RBA): 3.47%, -13bps; and New Zealand (RBNZ): 2.26%, -24bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JPY: Kato Nudges Up FX Jawboning, USD/JPY Little Changed

Headlines have crossed from Japan FinMin Kato, nudging up the FX rhetoric. Still, USD/JPY hasn't reacted much. Via BBG:

"*KATO: REFRAIN FROM COMMENTING ON FX TRENDS,

*KATO: SEEING ONE-SIDED, RAPID MOVES IN FX MARKET" - BBG,

"*KATO: IMPORTANT THAT FX MOVES STABLY, REFLECTING FUNDAMENTALS,

*KATO: GOVT WILL CAREFULLY EXAMINE EXCESSIVE FX MOVES" - BBG

These remarks from Kato appear to be a bit of step up in rhetoric compared to what was said earlier in the week. Today's remarks on seeing one-sided, rapid moves in FX market wasn't mentioned on Tuesday. From Tuesday Kato stated:

"*KATO: REFRAINING FROM COMMENTING SPECIFICALLY ON MARKET MOVES

*KATO: KEY FOR FX TO MOVE STABLY WHILE REFLECTING FUNDAMENTALS

*KATO: WILL CLOSELY WATCH ANY EXCESSIVE MOVES IN FX MARKET"

Still, we haven't seen remarks like deeply concerned about FX moves, or we will take appropriate action if FX moves excessively). USD/JPY sits down a touch for the session, last near 152.90, but hasn't reacted much to Kato's comments.

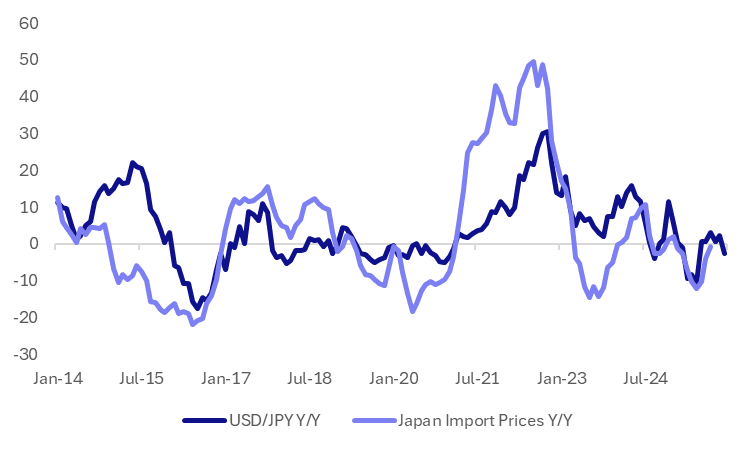

JAPAN DATA: Import Price Falls Moderating, Yen Weakness May Not Yet Be A Concern

The other part of Japan's price update this morning, was trade prices. In m/m terms, export prices rose 0.4%, matching Aug's gain. Import prices were up 0.3%m/m, the third straight monthly gain. We are off the July pace of 2.3% though. In y/y terms import prices were -0.8%y/y, against -3.9% in Aug. Disinflation from the import side continues to dissipate, which will be a BoJ watch point, particularly given renewed yen weakness. It is arguably too soon though to push the central bank to tighten rates.

- The chart below updates import prices y/y versus USD/JPY y/y changes. The USD/JPY line is extended to year end assuming current spot levels (just above 153.00 hold). Given elevated USD/JPY levels into end 2024, base effects should help keep y/y changes in the pair contained for end 2025. Higher m/m import momentum will be watched though. Sep gains were mostly evident in the commodity space, particularly metals.

- Our Japan policy team noted yesterday: The yen’s slide to an eight-month low against the dollar is unlikely to prompt a rate hike or Japanese authorities to intervene in FX markets immediately, as the weaker currency helps mitigate impacts of U.S. trade policy on exporters – a key driver of the economy, MNI understands.

- Also note, in a live TV broadcast on Thursday, Japan's new ruling party leader, Sanae Takaichi, said she has no plans to trigger an excessively weak yen and sees no immediate need to revise the 2013 BOJ accord. She noted both benefits and drawbacks of a weak yen.

Fig 1: Japan Import Prices & USD/JPY Y/Y (Assuming Current Spot Levels Prevail To Yr End)

Source: Bloomberg Finance L.P./MNI

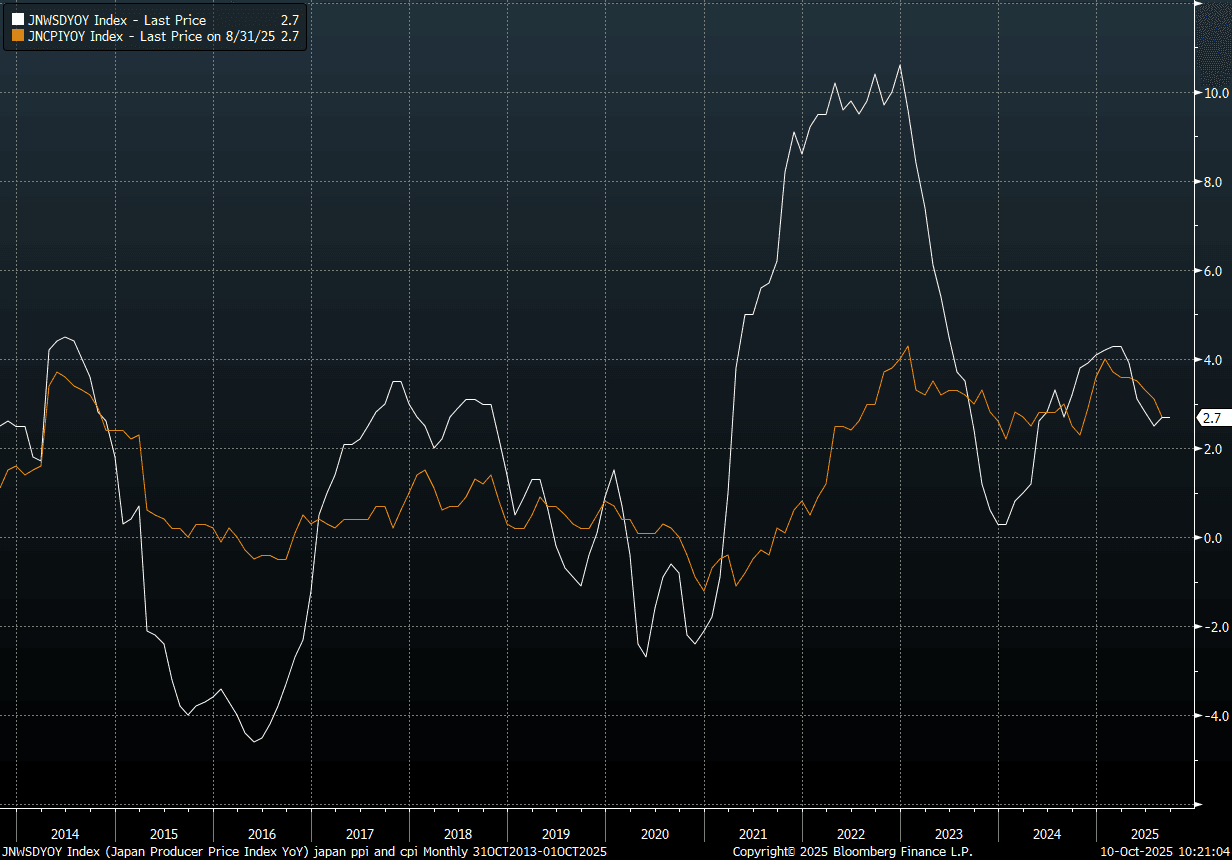

JAPAN DATA: PPI Above Forecast, But Suggests Steady CPI Trend

Earlier Japan PPI data was a touch above forecasts. It rose 0.3%m/m (0.1% was expected and -0.2% was prior), while in y/y terms we rose 2.7%, (2.5% was forecast). This leaves the y/y outcome unchanged on the August outcome. The chart below plots this y/y metric against headline CPI for Japan. At face value, it is consistent with a steady, albeit still elevated inflation backdrop.

- Via our Japan policy team: The index was supported by higher prices for nonferrous metals (+9.6% vs. +6.2% in August) but was weighed down by a smaller increase in agriculture, forestry and fishery products (+30.5% vs. +41.0%). Export prices for automobiles to the U.S. fell 16.3% on a yen basis and 18.8% on a contract currency basis, compared with August’s declines of 19.9% and 20.5%, respectively, suggesting that Japanese carmakers continue to lower export prices, squeezing profits.

Fig 1: Japan PPI & CPI Y/Y

Source: Bloomberg Finance L.P./MNI

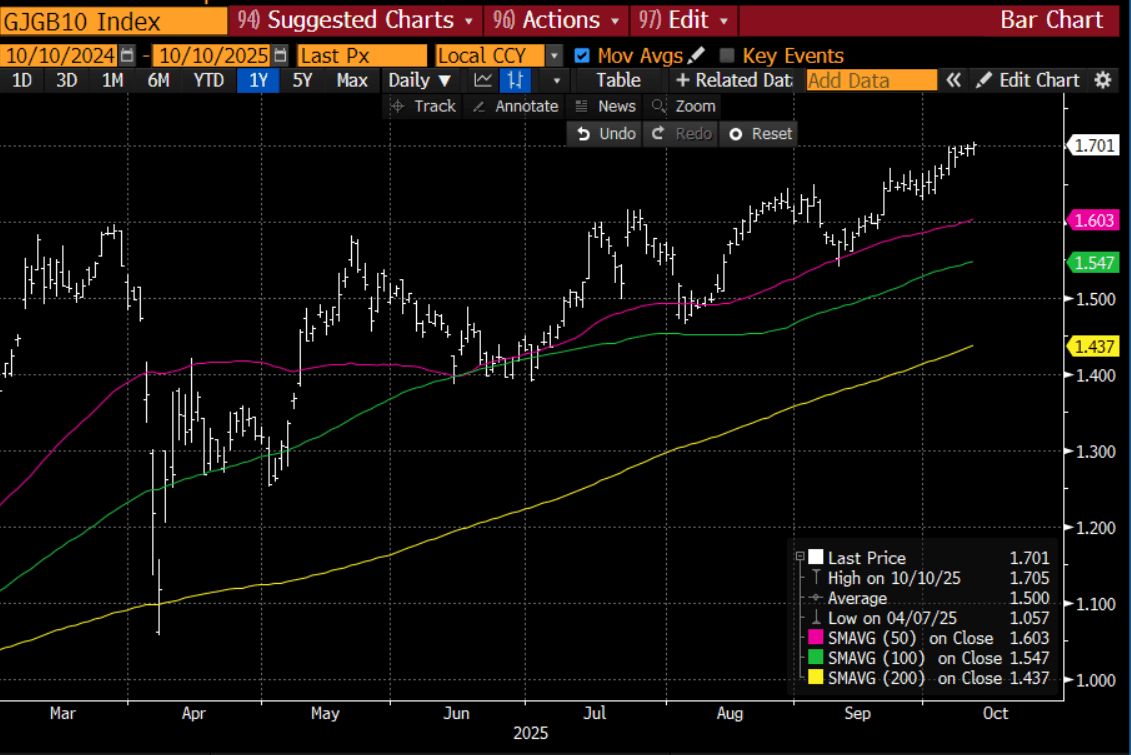

JGBS: Slightly Mixed But 10YY At Highest Since 2008

JGB futures are little changed, +1 compared to the settlement levels.

- Cash JGBs have continued to largely look past today's price data, with yields 0.5bp higher to 1.5bp richer across benchmarks.

- Nevertheless, the 10-year has pushed to a fresh cycle high of 1.705%, its highest yield since 2008. (See chart)

- Earlier Japan PPI data was a touch above forecasts. Moreover, disinflation from the import side continues to dissipate, which will be a BoJ watch point, particularly given renewed yen weakness. It is arguably too soon, though, to push the central bank to tighten rates.

- The benchmark 30-year yield is down 0.8bps at 3.178%, after trading in a 3.15-3.35% range this week. Even if the BOJ refrains from further rate hikes this year - with only a small chance currently priced in - we doubt long-dated JGBs would rally meaningfully, as such a move would likely be seen as a delay in tightening rather than its abandonment.

- Swap rates are, however, 1-3bps richer, with tighter swap spreads.

- On Monday, the local market will be closed.

Bloomberg Finance LP

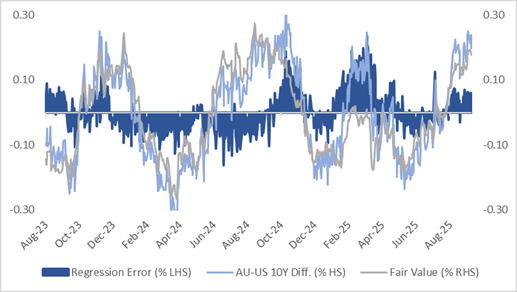

AUSSIE BONDS: Cheaper, AU-US 10Y Diff Back Near Wides, Issuance Light Next Week

ACGBs (YM -3.5 & XM -2.5) are weaker after trading in narrow ranges in today’s session.

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at +24bps. At +24bps, the differential is near the top of the ±30bps range that has prevailed since November 2022.

- Going forward, a move toward the top of the range would likely prompt international investors and traders to initiate differential-narrowing trades. Such flows would tend to be self-reinforcing so long as it aligned with the direction of the AU–US 1Y3M spread.

- The bills strip is -3 to -4 across contacts.

- RBA-dated OIS pricing shows a 25bp rate cut in November as a 36% probability, with a cumulative 13bps of easing priced by year-end.

- Next week, the AOFM plans to sell A$400mn of the 3.25% 21 June 2039 bond on Tuesday, A$800mn of the 4.25% 21 December 2035 bond on Wednesday and A$800mn of the 1.00% 21 December 2030 bond on Friday.

- Issuance is below the typical size in fiscal 2026 of about A$2.2bn for a second straight week. This is consistent with the recently reported budget deficit for fiscal 2025 of A$10bn, less than its forecast of A$27.9bn earlier this year.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

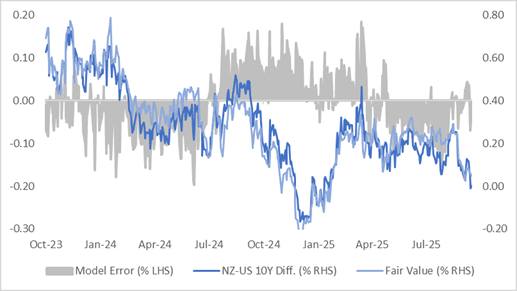

BONDS: Post-RBNZ Rally Stalls Ahead Of W/E

NZGBs closed 2-3bps cheaper, with the NZ-US 10-year differential 1bp wider at flat.

- At this level, the differential sits in the lower half of the -20bps to +40bps range observed year to date. For context, it was around +30bps in mid-September, prior to the release of much weaker-than-expected Q2 NZ GDP data.

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is about 6bps below its estimated fair value of +8bps. (See chart)

- Swap rates closed 2-3bps higher. As noted previously, the 30bp decline in the 2-year rate since the release of Q2 GDP in late September appeared increasingly over-extended, with the rate approaching channel resistance. A period of consolidation, therefore, looks more likely unless another negative economic shock emerges.

- “NZ Finance Minister Nicola Willis expressed optimism about the country’s economy, saying she was confident it had returned to growth last quarter as interest-rate cuts help boost sentiment.”- BBG

- RBNZ dated OIS pricing is little changed across meetings. 23bps of easing is priced for November, with a cumulative 33bps by February 2026.

- On Monday, the local calendar will see Performance Services Index and Net Migration data.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

FOREX: Asia FX Wrap - USD: Can The Bounce Extend?

The BBDXY has had a range of 1214.52 - 1216.07 in the Asia-Pac session; it is currently trading around 1215, -0.10%. The USD has given back a little of its overnight gains in our session after the PBOC delivered a much stronger fix at 7.1048. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD. Longer term accounts could potentially look to fade this squeeze as they increase hedging ratios.

- EUR/USD - Asian range 1.1556 - 1.1571, Asia is currently trading 1.1570. The pair extended its retracement after breaking below 1.1600 overnight. Price is probing its first support around the 1.1550 area; a break through here is needed to signal a deeper correction towards the more important 1.1200-1.1300 support.

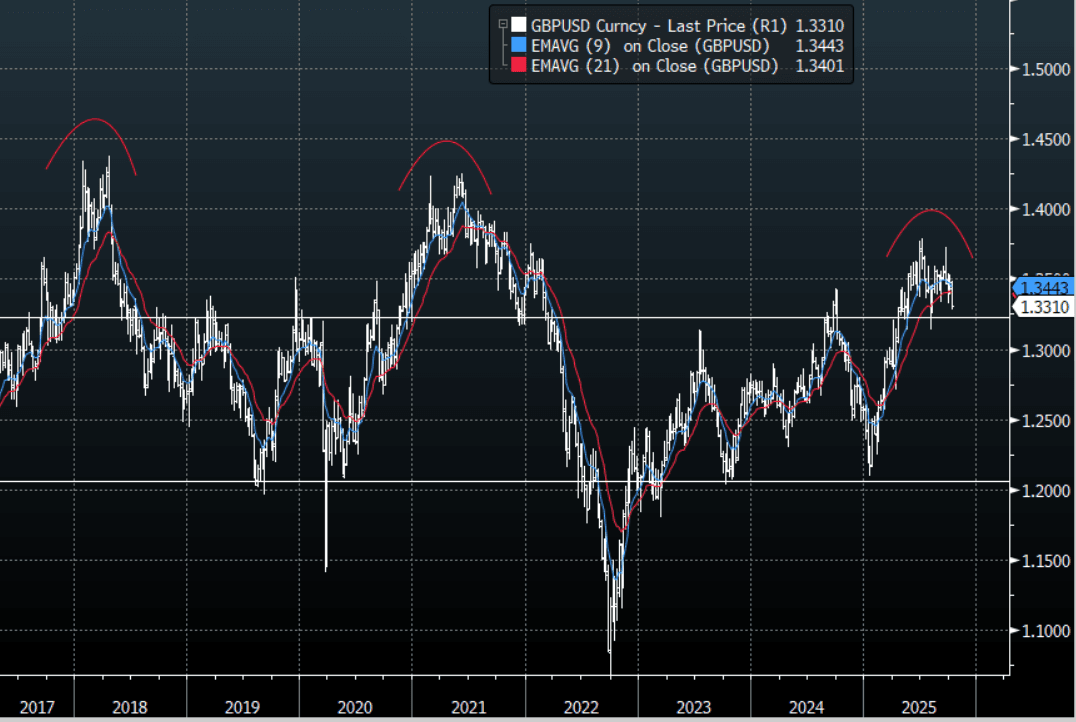

- GBP/USD - Asian range 1.3293 - 1.3309, Asia is currently dealing around 1.3300. The pair continues to be capped on any move back towards the 1.3500 area. Cable looks to be breaking its recent support this could potentially signal a deeper move lower. Should this support give way the next support is around 1.3150, below this support and it could signal a potential interim top in the pair. See Graph Below.

- USD/CNH - Asian range 7.1288 - 7.1392, the USD/CNY fix printed lower at 7.1055, Asia is currently dealing around 7.1310. The area around 7.1500/1600 has proved to be solid resistance and with the PBOC managing the fix lower, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX +0.15%, Gold $3985, US 10-Year 4.137%, BBDXY 1215, Crude Oil $61.59

- Data/Events : Italy Industrial Production. Asia FX Wrap - USD Can The Bounce Extend

Fig 1: GBP/USD Spot Weekly Chart

Source: Bloomberg Finance L.P./MNI

JPY: Asia-Pac: USD/JPY Momentum Higher Stalls, FinMin Fx Jawboning Firms

The USD/JPY range has been 152.64 - 153.27 in the Asia-Pac session, it is currently trading around 152.75, -0.20%. The pair dipped overnight on Takaichi pushing back on a weaker JPY being part of her platform; it was very short-lived though. The market is doing some work around the 153.00 area. Having come a long way very quickly we could have some pullbacks but I suspect dips will now be supported as we begin a new leg higher, with the focus ultimately back toward the 155-160 area.

- Intervention risks remain a focus. FinMin Kato stated today they were seeing one-sided, rapid moves in FX market. Such remarks weren't used on Tuesday (focus was on closely watching excessive moves, key for FX to moves with fundamentals when Kato spoke then). Still, we haven't seen remarks like deeply concerned about FX moves, or we will take appropriate action if FX moves excessively, which could signal greater interventon risks.

- MNI Policy believes the Yen Fall is Unlikely To Drive Swift Japanese Action. The yen’s slide to an eight-month low against the dollar is unlikely to prompt a rate hike or Japanese authorities to intervene in FX markets immediately, as the weaker currency helps mitigate impacts of U.S. trade policy on exporters – a key driver of the economy, MNI understands.

- MNI on Japan Data - PPI Above Forecast, But Suggests Steady CPI Trend : It rose 0.3%m/m (0.1% was expected and -0.2% was prior), while in y/y terms we rose 2.7%, (2.5% was forecast). This leaves the y/y outcome unchanged on the August outcome. At face value, it is consistent with a steady, albeit still elevated inflation backdrop.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 150.00($986m Oct 15), 151.50($905m Oct 15) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: Bloomberg Finance L.P./MNI

AUD: Asia-Pac - AUD Drifts Higher, 0.6625 Resistance Holding

The AUD/USD has had a range of 0.6552 - 0.6570 in the Asia- Pac session, it is currently trading around 0.6565, +0.20%. The USD has drifted lower in our session after the PBOC delivered a much stronger fix at 7.1048. The AUD could not break above the 0.6625 resistance overnight and fell away pretty easily from there as the USD built on its recent gains. While AUD/USD remains below 0.6625/50 I suspect the risk remains skewed to the down side and sellers will fade bounces initially. First support is back toward 0.6500 but a break below here would signal a deeper correction lower and could see the move accelerate.

- The USD move is beginning to challenge a market that is short but we are approaching some pivotal levels and suspect longer-term investors might see this bounce as an opportunity to fade as weaker hands are forced out.

- Bloomberg reported that Governor Michele Bullock said “Australia’s economy is in a “pretty good spot” with inflation inside the central bank’s 2%-3% target band and the labor market still tight.” speaking in Canberra today.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6545(AUD657m). Upcoming Close Strikes : 0.6500(AUD1.01b Oct 14), 0.6600(AUD943m Oct 14), 0.6650(AUD880m Oct 14) - BBG

- AUD/JPY - Asia-Pac range 100.23 - 100.50, Asia is trading around 100.45. The pair has surged higher for good reason on the election outcome. It has extended its move higher and is looking to build on its break above 100. Dips should now be supported as the focus now turns toward 102.50 and then the 105.00 area.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

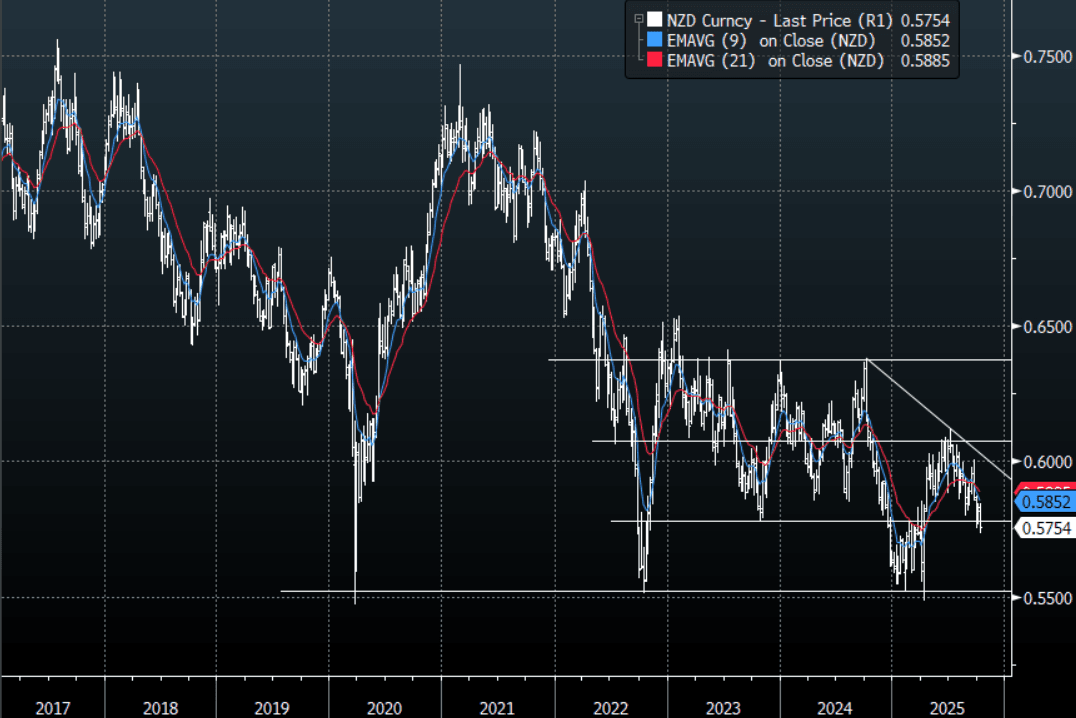

NZD: Asia-Pac: NZD/USD Drifts Higher Helped By Strong CNY Fix

The NZD/USD had a range of 0.5742 - 0.5757 in the Asia-Pac session, going into the London open trading around 0.5755, +0.15%. of 0.6552 - 0.6570 in the Asia- Pac session, it is currently trading around 0.6565, +0.20%. The USD has drifted lower in our session after the PBOC delivered a much stronger fix at 7.1048. The NZD ran into solid supply back toward 0.5800 overnight and when the USD began to build on its gains the NZD fell away very quickly challenging the RBNZ lows. The NZD remains one of the stand out vehicles to express a short, you just have to decide what against. Rallies should now be faded while below 0.5800/0.5850, the market will be looking for a potential move back towards the 0.5500/0.5600 area.

- "NZ'S WILLIS: FORECASTS REMAIN THAT ECONOMY WILL RECOVER IN 3Q, BUDGET SURPLUS IN 2028 REMAINS A ‘FISCAL GOAL’, CONFIDENT NZ’S ECONOMIC GROWTH WILL ACCELERATE IN Q4" - BBG

- "NZ'S WILLIS: NOT PLANNING ANY MAJOR ASSET SALES, WILL LOOK TO USE BALANCE SHEET TO FUND PROJECTS" - BBG

- "NZ'S WILLIS: ECONOMY DOESN'T NEED A FISCAL STIMULUS, ECONOMIC STIMULUS IS COMING FROM MONETARY POLICY" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14) - BBG

- AUD/NZD range for the session has been 1.1401 - 1.1417, currently trading around 1.1415. The Cross surged back above 1.1400 on the surprise 50bps cut. I continue to feel the cross should do some work in the 1.1400/1.1500 area. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Weighed By China Curbs, HSTECH Back Close To 20-day EMA

Most Asia Pac markets are lower, with tech headwinds weighing. This reflects broader global moves (with major indices down in cash trade on Thursday) but also concerns around China export controls in the tech space. Given how bullish sentiment has been recently, markets may be needing fresh catalysts to continue the recent rally at its heady pace. US futures sit touch higher, with Eminis last around 6789, just off record highs above 6812.

- The CSI 300 index is off around 1.1% as we approach the lunchtime break. Recent cycle highs have been above 4726, while we last tracked near 4659. The 20-day EMA support point is back around 4547, with dips to this zone supported since early July.

- BBG notes: "Batteries and some materials-related stocks lead declines after China said it would impose export controls on some lithium batteries, critical materials, and related technology and equipment" These announcements followed yesterday's earlier rare earth export controls. Valuation concerns also linger.

- The HSI is off around 1% as well, while the HSTECH is down over 2.3%, tracking lower for the fifth straight session. We are no back close to the 20-day EMA (6294 versus 6311 current levels). The RSI (14) has corrected from overbought conditions, back to 54.

- Japan markets are weaker. The Topix down 1.7%, the MKY 225 off 1%. The uptrend in USD/JPY has stalled somewhat (back under 153.00), verbal rhetoric from the FinMin picked up a touch. Again, these markets are correcting from overbought levels from a technical standpoint.

- South Korea is bucking these trends, up 1.25% for the Kospi, as onshore markets return after the recent break. Chip/AI related firms like Samsung surged at the open.

- In South East Asia, most markets are down but only modestly. The exception is Thailand, which is off 1.9% and putting the SET back under 1300. BBG notes: "Delta Electronics shares slide after the stock exchange imposes market surveillance measures following their record-breaking rally.".

US: Bessent - India To Start Buying More US Oil, Argentine Peso Undervalued

US Treasury Secretary Bessent was on FoxNews earlier. It was noteworthy that he stated that India will soon be buying less oil from Russia and that it will be rebalancing more towards US oil (via Rtrs). This comes as the US government looks to build pressure on Russia to end the Ukraine conflict, with reduced oil revenue seen as one avenue. Whether this is part of a broader US-India deal/trade package, which helps to lower Indian tariffs, remains to be seen.

- Other snippets from the Bessent interview included this: "U.S. TREASURY SECRETARY: I BELIEVE CHINESE WILL HAVE COME BACK AT THE END OF THE SEASON AND BUY SOY BEANS - [RTRS]". Bessent added that farmers would have been given assistance if it wasn't for the government shutdown. This remains a focus point for the US ahead of China talks.

- Bessent also noted the US assistance being provided to Argentina is not a bailout, while also stating the Argentine Peso is undervalued (via RTRS). From Thursday we saw, via BBG: "Washington has finalized a $20 billion currency swap framework with Argentina’s central bank, Treasury Secretary Scott Bessent said in a social media post."

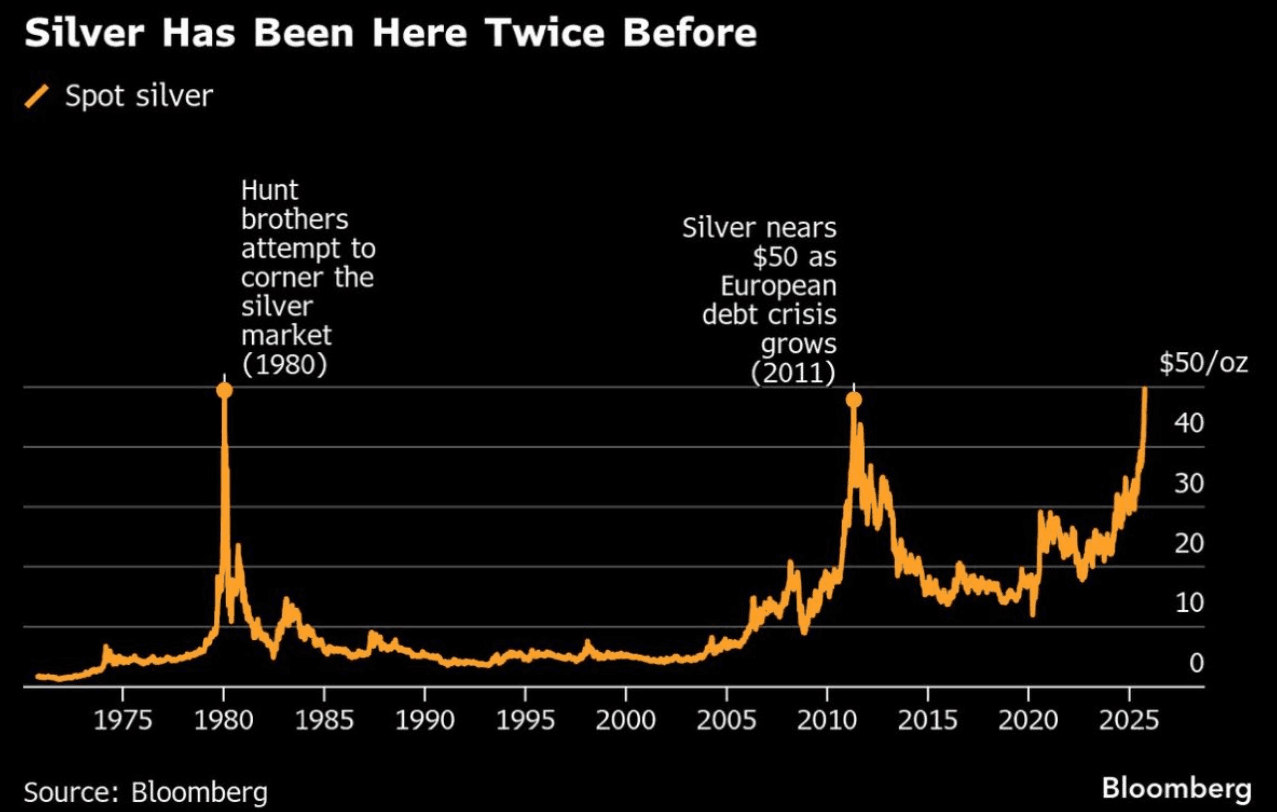

PRECIOUS METALS: Silver - Makes New All-Time Highs Above $50

The range overnight for XAG was $48.474 - $51.235, Asia is currently trading around $49.15, -0.25%%. Silver continued its parabolic move higher making new all-time highs above $50.00. The last two times the metal has reached these lofty heights it has very quickly retreated so some caution is warranted. With all the talk regarding fiat currency debasement growing louder this feels like it still has some legs to go further. Short-term you can’t rule out some pullbacks but I suspect these will be supported as the market tries to extend and build a move above and beyond $50.

- Samantha LaDuc expands on the bullish structure of the move on X: “You know what is kinda scary? This gold/silver squeeze is not your AI-mania kinda squeeze, but a structurally important layer in a central bank reserve asset that has implications on global settlement of trade & risk partity in purchasing power - not just a hedge on inflation & fiscal profligacy.”

Fig 1 : Silver Chart

Source: MNI - Market News/Bloomberg Finance L.P/@BurggrabenH

COMMODITIES: Gold Softer But Bull Cycle Intact, Oil Range Bound

Gold is softer, but above Thursday lows at this stage, as sentiment turns a little more cautious post the recent surge through $4000. We are still up +2% for the week, tracking higher for the 10th straight week (spot bullion was last near $3964). Oil benchmarks are little changed, last at $65/bbl for Brent and $61.40/bbl for WTI. We are tracking close to 1% firmer for the week, but this followed last week's near 8% fall. Some support for oil has been evident following a more cautious OPEC November output increase and US product drawdowns.

- For gold, the recent correction from highs of $4059.3, looks to be profit taking/technical correction. Such flows may have been encouraged by the recent Israel/Hama ceasefire as well (lowering geopolitical tensions).

- Via DJ, the debasement theme remains key one though: "The gold rally this year signals increasing distrust in the existing fiscal and monetary order, says Ajay Rajadhyaksha, Barclays global chairman of research, in a note. "

- Even with a softer USD backdrop so far today, gold is still tracking lower, which also points to positioning/momentum driving price shifts in the near term.

- Gold is still well above its 20-day EMA (last around $3831), while a fresh test above $4000 may see sights set on $4074.54, a Fibonacci projection.

BSP: Growth Risks To Determine Further BSP Easings, JPM Sees 3 More Cuts

Yesterday's surprise BSP rate cut, 25bps to 4.75%, took rates to lowest levels since 2022. Comments by BSP Governor Remolona this morning reiterated that the central bank's main driver for going yesterday was growth concerns stemming from the corruption scandal. Remolona noted confidence had been dented, while signs of investment slowing were already clear. He did state growth should improve in 2027 (per CNBC/BBG).

- This suggests that further easings will likely to be dependent on the growth backdrop. The data calendar is pretty quiet until the end of this month when trade and bank lending figures are due. The bank lending data will be watched given this can often lead investment.

- In early Nov we get CPI for Oct, then on Nov 7 Q3 GDP. This could be too soon to gauge the impact of the corruption scandal on growth, but if there is already evidence of weaker momentum it likely pave the way for a further cut in Dec.

- Both J.P. Morgan and Goldman Sachs expect 25bps cuts at the Dec meeting. Indeed J.P. Morgan notes: "With both domestic and external growth pressures rising and policy settings still in restrictive territory, we think that the central bank will likely attempt to continue policy normalization, and we now pencil in three more consecutive 25bp rate cuts, taking the policy rate to 4.0% by next April."

- Goldman Sachs states: "Given the Governor’s dovish guidance today, we see risk of further easing in 2026, if activity data (e.g. business sentiment index) points towards further growth softness."

PHP: USD/PHP Upside Capped At 58.30/40, But Downside May Remain Limtied

USD/PHP sits back at 58.25/30 in latest dealings, once again finding good selling interest in the 58.30/40 region (earlier highs were at 58.405). Fallout from yesterday's surprise 25bps easing has been limited so far, although official intervention may be continuing to cap gains in the pair. Earlier data this week showed a healthy headline FX reserve position (+$108.8bn as at end Sep). The authorities may be aiming to curb FX weakness until a better seasonal backdrop unfolds in Nov/Dec of this year (remittance inflows typically aid PHP over this period).

- In the cross asset space, local equities haven't shown much upside following yesterday's hike. PCOMP remains near 6050, so still close to recent lows.

- BSP Governor Remolona stated earlier that the corruption scandal was a key focus point for the rate cut decision, with signs of reduced investment and lower sentiment (per CNBC/BBG). He stated growth should recover in 2027.

- Such a backdrop may not aid a turn lower in USD/PHP in the near term. The 20-day EMA is around 57.84, where we bounced off yesterday.

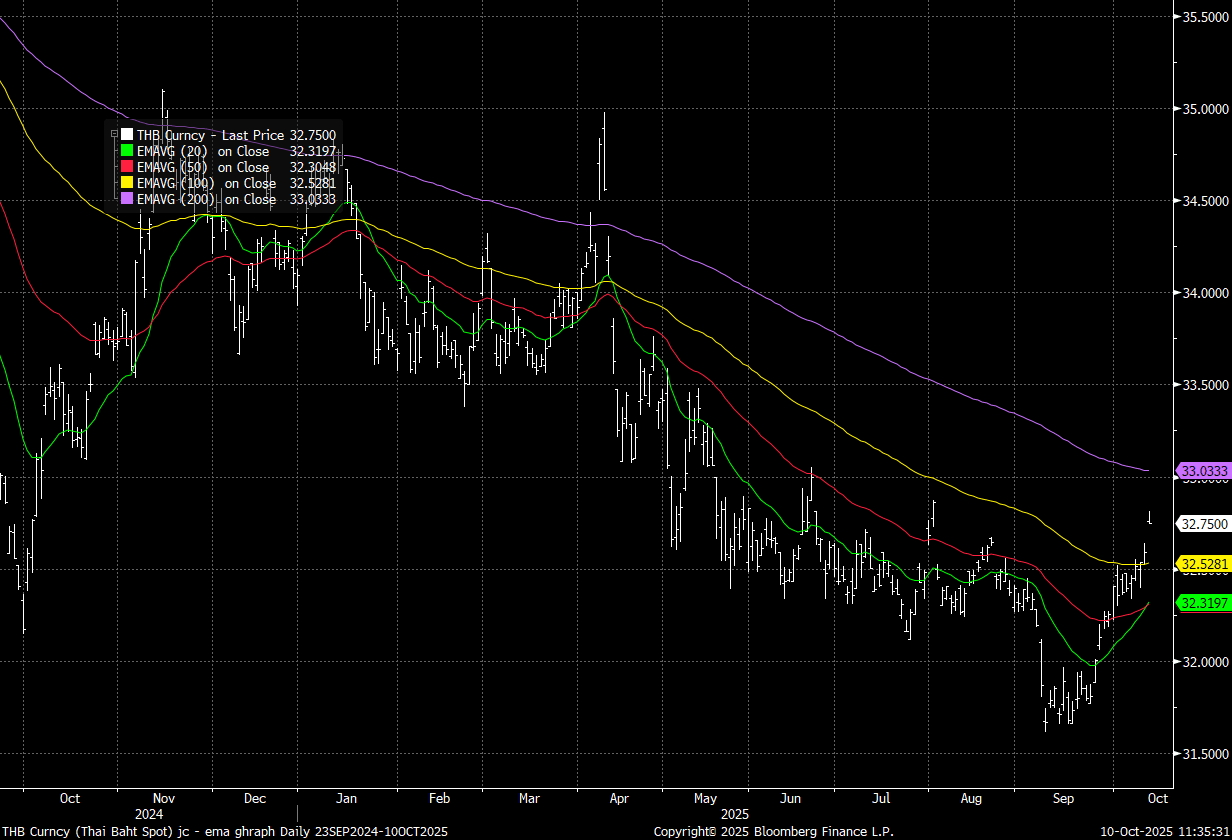

THB: USD/THB Eyeing 33.00 Upside Test, New BoT Governor Speaks Today

USD/THB tested above 32.80 in the first part of Friday trade, fresh highs since early Aug (per BBG). We are above all key EMAs except for the 200-day (at 33.03). The 100-day is back around 32.53 (which may now act as a support point) (see the chart below). Broader USD gains, coupled with gold prices back under $4000, are THB headwinds. The pair remains in an uptrend since late Sep, with likely upside focus around the 33.00 level.

- Focus today will be on new BoT Governor Vitai, who holds his first meet the press event at 1pm local time (per BBG). The Shippers council will also hold a briefing at 11am local time to discuss the export backdrop (with baht gains/strength this year having been a focus point).

- The Commerce Ministry noted late yesterday: "The Thai baht is expected to strengthen further following expectations the Federal Reserve’s additional rate cut, which will likely attract capital inflows, Commerce Minister Suphajee Suthumpun says." (via BBG).

- Whilst this recent run higher will be welcomed by the authorities it is not being supported by US-TH yield differentials, which have tracked down a touch since this week's surprise BoT hold (1y1y differential at +202bps).

- USD/THB also looks too higher relative to gold price trends (even with the recent gold correction), but the focus of the authorities is to reduce the strength is this relationship.

Fig 1: USD/THB Versus Key EMAs

Source: Bloomberg Finance L.P./MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/10/2025 | 0600/0800 | *** | CPI Norway | |

| 10/10/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/10/2025 | 0900/1100 | * | Industrial Production | |

| 10/10/2025 | - | ECB de Guindos at ECOFIN Meeting | ||

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1230/0830 | *** | Labour Force Survey | |

| 10/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 10/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 10/10/2025 | 1700/1300 | St Louis Fed's Alberto Musalem | ||

| 10/10/2025 | 1800/1400 | ** | Treasury Budget |