NZD: Asia-Pac: NZD/USD Drifts Higher Helped By Strong CNY Fix

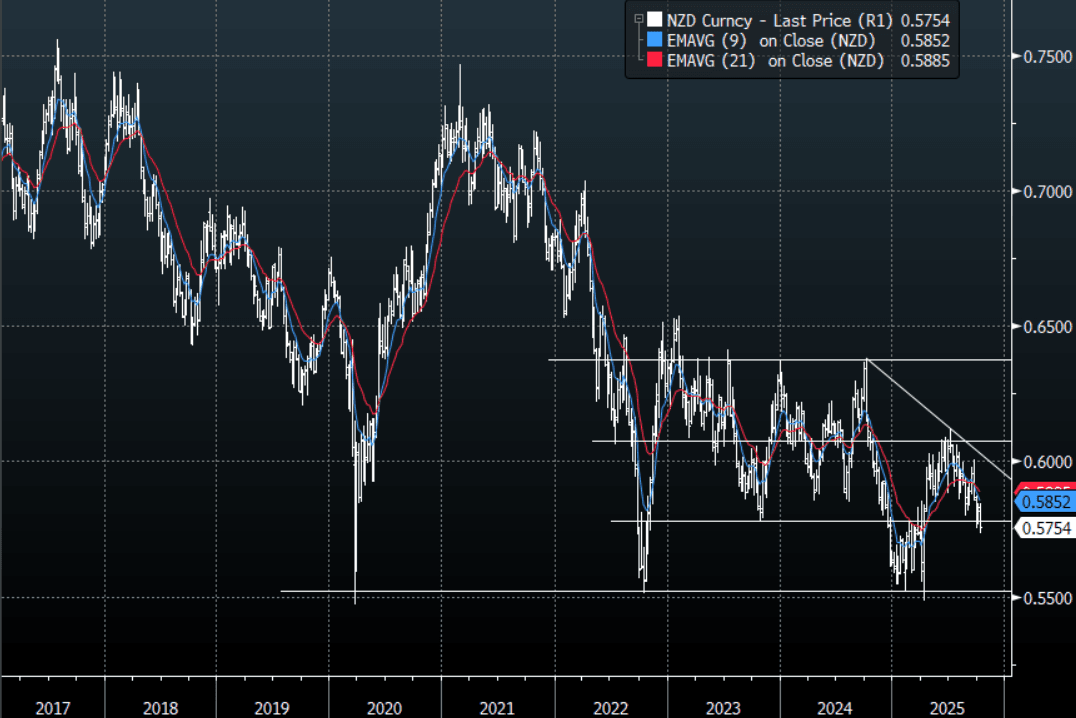

The NZD/USD had a range of 0.5742 - 0.5757 in the Asia-Pac session, going into the London open trading around 0.5755, +0.15%. of 0.6552 - 0.6570 in the Asia- Pac session, it is currently trading around 0.6565, +0.20%. The USD has drifted lower in our session after the PBOC delivered a much stronger fix at 7.1048. The NZD ran into solid supply back toward 0.5800 overnight and when the USD began to build on its gains the NZD fell away very quickly challenging the RBNZ lows. The NZD remains one of the stand out vehicles to express a short, you just have to decide what against. Rallies should now be faded while below 0.5800/0.5850, the market will be looking for a potential move back towards the 0.5500/0.5600 area.

- "NZ'S WILLIS: FORECASTS REMAIN THAT ECONOMY WILL RECOVER IN 3Q, BUDGET SURPLUS IN 2028 REMAINS A ‘FISCAL GOAL’, CONFIDENT NZ’S ECONOMIC GROWTH WILL ACCELERATE IN Q4" - BBG

- "NZ'S WILLIS: NOT PLANNING ANY MAJOR ASSET SALES, WILL LOOK TO USE BALANCE SHEET TO FUND PROJECTS" - BBG

- "NZ'S WILLIS: ECONOMY DOESN'T NEED A FISCAL STIMULUS, ECONOMIC STIMULUS IS COMING FROM MONETARY POLICY" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14) - BBG

- AUD/NZD range for the session has been 1.1401 - 1.1417, currently trading around 1.1415. The Cross surged back above 1.1400 on the surprise 50bps cut. I continue to feel the cross should do some work in the 1.1400/1.1500 area. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Holding 2-4Bps Firmer, RBNZ To Consult On OMOs

Benchmark NZGB yields how around 2-4bps higher for Wednesday trade. Outside of early yield moves, which followed US gains from Tuesday trade, we have seen quite steady trends through the rest of trade today. The 2yr yield rests at 2.96%, while the 10yr is just above 4.33%, up around 4bps. The 2/10s curve is a touch steeper at +137bps. The 2yr swap rate is down a touch to 2.745%.

- US Tsy futures are a touch weaker so far today, while cash yields are little changed ahead of key inflation data (both this evening and on Thursday).

- The data calendar just had net migration figures for July, not a market mover. We were up +2k and showing some signs of stabilization, with annual migration up to +13k. Still, we are coming from a low base, so further recover is likely needed for this to benefit the economy more broadly.

- The RBNZ announced: "We are consulting on how we conduct Open Market Operations and are seeking input on design considerations for a Committed Liquidity Facility. This consultation builds upon previous work, including speeches and Bulletins given as part of the Liquidity Management Review. Respondents to the consultation may choose to comment on one or both parts of the consultation and whichever questions are relevant to them. This consultation is open until 31 October."

- The data calendar is empty tomorrow, with Friday delivering the Aug PMI, along with card spending figures.

GOLD: Gold Higher Ahead Of US PPI Data

Gold prices are off their intraday low of $3620.47/oz despite the ruling that temporarily blocks President Trump removing Fed Governor Cook. The judge said that possible mortgage fraud was unlikely to be “cause” for dismissal and that the way she was dismissed was against the constitution. With threats to Fed independence recently driving bullion higher, it has not responded to the news. Gold is currently up 0.4% to $3639.0 supported by increased Middle East tensions as well as a lower US dollar (BBDXY -0.1%). US yields are steady.

- Bullion reached a high of $3640.91 early in today’s APAC trading holding below yesterday’s record of $3674.27.

- The FT reported that President Trump told European representatives that he’s prepared to impose the same tariffs as Europe on China and India for buying Russian energy. However, Trump said he had spoken with his “good friend” Indian PM Modi.

- Gold has found support from increased central bank buying with the PBoC purchasing over successive months but Bloomberg reported that RBI is also accumulating and that Czech holdings are at record.

- After falling 1.2% on Tuesday, silver is 0.4% higher today at $41.03. It fell to $40.721 and then recovered to a high of $41.045.

- Equities are rallying with the S&P e-mini up 0.2%, Hang Seng +1.2% and KOSPI +1.5%. Oil prices are higher again with WTI +0.9% to $63.20/bbl. Copper is up 0.4%.

- Later August US PPI data are released and will be watched closely given that a 25bp rate cut is fully priced in for September 17. CPI is out on Thursday. The ECB’s Buch speaks today.

MNI EXCLUSIVE: MNI Discusses China's Bid To Boost Consumption