US: Bessent - India To Start Buying More US Oil, Argentine Peso Undervalued

US Treasury Secretary Bessent was on FoxNews earlier. It was noteworthy that he stated that India will soon be buying less oil from Russia and that it will be rebalancing more towards US oil (via Rtrs). This comes as the US government looks to build pressure on Russia to end the Ukraine conflict, with reduced oil revenue seen as one avenue. Whether this is part of a broader US-India deal/trade package, which helps to lower Indian tariffs, remains to be seen.

- Other snippets from the Bessent interview included this: "U.S. TREASURY SECRETARY: I BELIEVE CHINESE WILL HAVE COME BACK AT THE END OF THE SEASON AND BUY SOY BEANS - [RTRS]". Bessent added that farmers would have been given assistance if it wasn't for the government shutdown. This remains a focus point for the US ahead of China talks.

- Bessent also noted the US assistance being provided to Argentina is not a bailout, while also stating the Argentine Peso is undervalued (via RTRS). From Thursday we saw, via BBG: "Washington has finalized a $20 billion currency swap framework with Argentina’s central bank, Treasury Secretary Scott Bessent said in a social media post."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Cash Open

TYZ5 is trading 113-08, down 0-03 from its close.

- The US 2-year yield opens around 3.552%, down 0.01 from its close.

- The US 10-year yield opens around 4.084%.

- MNI US DATA: For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior). Core PCE estimates are for 0.31% M/M vs 0.27% prior, with no analysts seeing core PCE printing above core CPI. That could change based on various PPI components that feed into PCE, but as it stands, the M/M core PCE estimate would be the highest since February.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

- Zerohedge on X: “If the Fed knew how bad the labor market truly was, it would have cut 25bps in March and another 25bps in June/July. There is every case to be made for a 50bps rate cut in Sept.”

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone between 4.15%-4.20%. First target the 4.00% zone then the 3.80% area.

- Data/Events: MBA Mortgage Applications, PPI, Wholesale Inventories/Sales

JAPAN DATA: Rtrs Monthly Tankan At Multi Yr Highs, Official Q3 Print Due Oct 1

Headlines crossed earlier from Reuters from its monthly survey tracking the BoJ's quarterly Tankan survey - "Manufacturers' sentiment index +13 in September vs +9 in August" (Rtrs). It added, "...showed the manufacturers' mood index improved to 13 in September from 9 in August, marking a third month of increases and the highest reading since August 2022."

- "Multiple managers in the transport machinery sector said they were receiving solid orders, while some referred to stagnant domestic production in recent months given a shrinkage in exports" (via Rtrs). However, the report also noted more caution around the outlook, reflecting concerns on the domestic economic backdrop.

- The official Q3 Tankan report will be out on Oct 1 and will be a key watch point for the BoJ, as it looks to gauge fallout from the US-Japan trade deal.

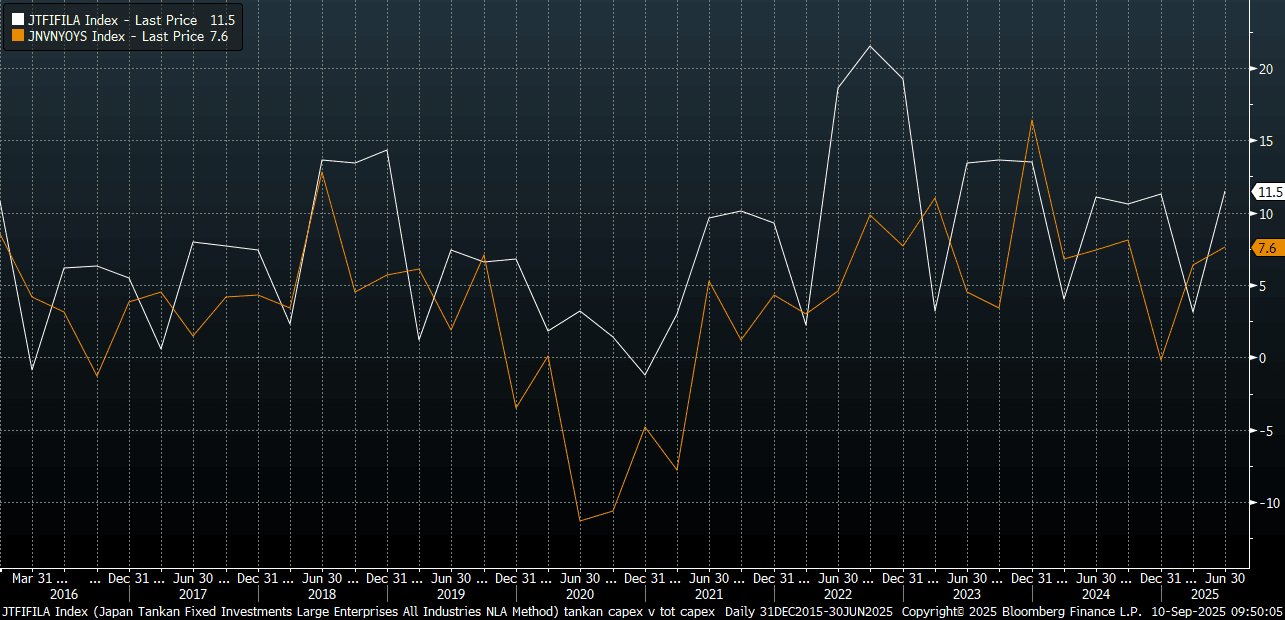

- The last Tankan survey for Q2 painted a resilient backdrop for large manufacturers, while the all industry capex estimate was also nudged higher. The chart below plots this capex estimate against total capex investment y/y.

- A resilient Q3 outcome could give the BoJ renewed confidence in the economic outlook and ring rate hikes back onto the agenda. We saw late yesterday some hawkish headlines via BBG, indicating there is a "chance of" a hike this year despite the political turmoil following PM Ishiba's resignation Sunday, which also weighed on USD/JPY (but follow through to the downside was limited). "Some officials are even of the view that a hike might be appropriate as early as October", the Bloomberg article added.

- Market pricing for a hike in Oct remains fairly modest at this stage though.

Fig 1: Tankan Capex Estimate & Capital Investment Y/Y

Source: Bloomberg Finance L.P/MNI

JGBS: Futures Back Under 138.00, 5yr Supply On Tap Today

JGB futures finished the post Tokyo close on Tuesday at 137.76, -.24 versus settlement levels. Some negative lead likely came from core markets elsewhere, with US Tsy futures weakening ahead of key inflation data (out later today and tomorrow).

- Also note some likely weight from news wires headlines. A set of hawkish comments from the BOJ, indicating there is a "chance of" a hike this year despite the political turmoil following PM Ishiba's resignation Sunday, which also weighed on USD/JPY (but follow through to the downside was limited). "Some officials are even of the view that a hike might be appropriate as early as October", the Bloomberg article added.

- Market pricing for a hike in Oct remains fairly modest at this stage (implied rate of around 0.57%, versus a current effective policy rate of 0.48%).

- For JGB futures, recent lows for futures rest close to 137.20, while recent highs were at 138.37. The general technical bias remains for a bearish threat for futures.

- In the cash JGB space, the 10yr yield finished up just above 1.57%, while the 30yr was near 3.27%. The 2/30s curve finished up around +243bps.

- The data calendar is empty today. Rtrs noted earlier: "Japanese manufacturers' sentiment was its best in more than three years in September, the Reuters Tankan poll showed, with trade uncertainties easing after Japan reached a tariff deal with the U.S. in July." The actual Q3 Tankan survey is released on Oct 1.

- We do have 5yr debt supply on tap today. The last 5yr debt auction had a bid to cover ratio sub 3.00.