JPY: Asia-Pac: USD/JPY Momentum Higher Stalls, FinMin Fx Jawboning Firms**

** corrected range for today

The USD/JPY range has been 152.64 - 153.27 in the Asia-Pac session, it is currently trading around 152.75, -0.20%. The pair dipped overnight on Takaichi pushing back on a weaker JPY being part of her platform; it was very short-lived though. The market is doing some work around the 153.00 area. Having come a long way very quickly we could have some pullbacks but I suspect dips will now be supported as we begin a new leg higher, with the focus ultimately back toward the 155-160 area.

- Intervention risks remain a focus. FinMin Kato stated today they were seeing one-sided, rapid moves in FX market. Such remarks weren't used on Tuesday (focus was on closely watching excessive moves, key for FX to moves with fundamentals when Kato spoke then). Still, we haven't seen remarks like deeply concerned about FX moves, or we will take appropriate action if FX moves excessively, which could signal greater interventon risks.

- MNI Policy believes the Yen Fall is Unlikely To Drive Swift Japanese Action. The yen’s slide to an eight-month low against the dollar is unlikely to prompt a rate hike or Japanese authorities to intervene in FX markets immediately, as the weaker currency helps mitigate impacts of U.S. trade policy on exporters – a key driver of the economy, MNI understands.

- MNI on Japan Data - PPI Above Forecast, But Suggests Steady CPI Trend : It rose 0.3%m/m (0.1% was expected and -0.2% was prior), while in y/y terms we rose 2.7%, (2.5% was forecast). This leaves the y/y outcome unchanged on the August outcome. At face value, it is consistent with a steady, albeit still elevated inflation backdrop.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 150.00($986m Oct 15), 151.50($905m Oct 15) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

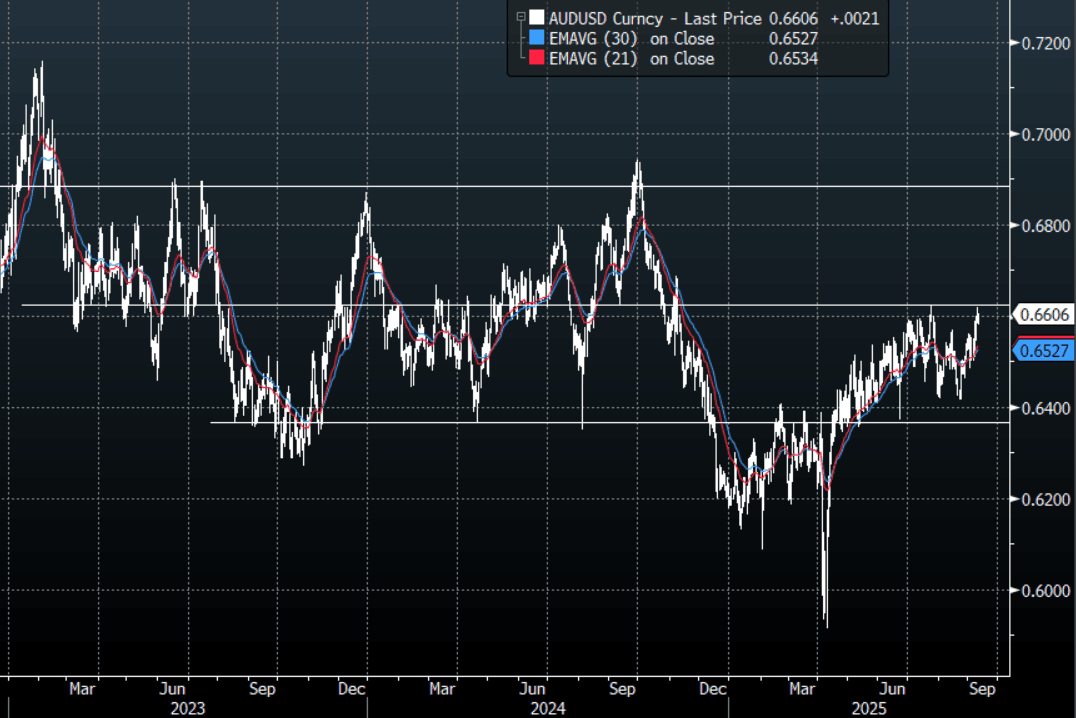

AUD: Asia Wrap - AUD Back Above 0.6600 As Risk Trades Higher Into Inflation Data

The AUD/USD has had a range of 0.6580 - 0.6606 in the Asia- Pac session, it is currently trading around 0.6605, +0.30%. US stocks are back at their highs even after record revisions to the payrolls data, nothing stops this train. The AUD is probing above 0.6600 again, having stalled overnight as the market awaits the inflation data this week. The AUD remains in its recent multi-month range of 0.6350-0.6650, should the USD break and extend lower we could potentially see the AUD break back above 0.6650. Should this occur it could provide the upward momentum to target levels back towards 0.6900/0.7000. Although still in the range the bias will be for dips back to 0.6500 to be supported for now.

- China Inflationary Pressures Fall Further: With some key onshore news suggesting that further monetary policy intervention is getting closer, today's CPI and PPI did little to dissuade that way of thinking. CPI in August declined -0.4%, ahead of estimates of -0.2% and the biggest drop since February.

- Melbourne Institute consumer inflation expectations for September are released on Thursday. It moderated substantially to 3.9% in August but the 3-month average has been around 4.5% since June.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD797m). Upcoming Close Strikes : 0.6650(AUD597m Sept 11) - BBG

- CFTC Data last week shows Asset managers reduced their shorts for the first time in a while -66025(Last -78758), the Leveraged community though look to be rebuilding their own shorts after winding them down -11860(Last -6447).

- AUD/JPY - Asia-Pac range 96.99 - 97.29, Asia is trading around 97.20. The pair topped out towards 97.50 but has consolidated its recent gains. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

OIL: Geopolitics Drives Brent Above Resistance, US Crude Stocks & PPI Later

Oil prices are higher again during today’s APAC trading after rising around 0.8% on Tuesday finding support from increased Middle East tensions following Israel’s strike on Hamas leaders in Qatar. WTI is up 0.9% to $63.22/bbl, close to the intraday high, and Brent is 0.9% higher at $67.01/bbl. The USD index is down 0.1%.

- Brent has broken above initial resistance at $69.53 opening up key resistance at $71.93. This week’s gains are still seen as corrective but a break of $71.93 may change that.

- The FT reported that President Trump told European representatives that he’s prepared to impose the same tariffs as Europe on China and India for buying Russian energy. However, Trump said he had spoken with his “good friend” Indian PM Modi and that trade negotiations were ongoing between them and that he expects “a successful conclusion for both”.

- Bloomberg reported that there was a US crude inventory build of 1.3mn barrels last week, according to those familiar with the API data. The official EIA data is out Wednesday.

- Later August US PPI data are released and will be watched closely given that a 25bp rate cut is fully priced in for September 17. CPI is out on Thursday. The ECB’s Buch speaks today.

AUSSIE BONDS: Futures Softer, But Up From Lows, Yields Tracking Recent Ranges

Aussie Bond futures are holding slightly weaker, both the 10yr (XM) and 3yr (YM) off around 2.5bps. 10yr futures were last 95.69, up from earlier lows of 95.675, while 3yr futures are at 96.535, (earlier lows were 96.525). Cash ACGB yields hold around 2bps firmer across the curve, with gains close to uniform. The 3yr yield is around 3.44%, while the 10yr is just under 4.285%.

- For the 3yr yield, downside focus is likely to rest sub 3.40%, which we haven't meaningfully breached in Sep to date, while recent highs rest around 3.55%. For the 10yr, we have spent little time sub 4.20% in recent months, while topside interest has been capped above 4.40%.

- Like NZ, news/data flow has been light in Australia today.

- Tomorrow we get Sep consumer inflation expectations.

- Earlier, via BBG: "Australia sold A$1 billion ($658.8 million) of bonds due Nov. 21, 2031 on Sept. 10."