MNI US Macro Weekly: Navigating Murky Waters

Oct-10 2025 20:30By: Tim Cooper and 1 more...

USEmploymentMinutesChina+ 5

Hidden PDF

- The federal government shutdown that began October 1 is all but certain to extend through the middle of the month, with prediction markets eyeing just a one-in-three chance it’ll be concluded by Oct 22.

- The actual economic fallout is not expected to be extensive (yet), but it’s left the data schedule somewhat lacking. What readings we have received don’t really change the underlying narrative.

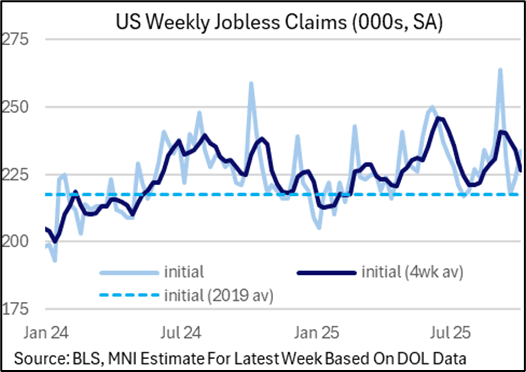

- We will have to wait indefinitely to get the September Employment report but jobless claims (cobbled together from state-level readings) continue to portray a low-hiring, low-firing labor market, and various higher-frequency measures of economic activity suggest that growth maintained an above-potential pace at least through early October even as consumer confidence remains limp.

- We, as well as the Fed and market participants, are increasingly eyeing "Alternative" data sources that are mainly private-sector indicators that offer insight into trends in key areas of the economy, including the Labor Market, Retail Sales/Consumer, Inflation, Housing, and Economic Activity. Our calendar - linked to below - includes some of these indicators and the document includes expected release dates and links.

- With data proving limited in its market-moving ability, the standout move in the week was a strong rally in US rates Friday on President Trump threatening more extensive tariffs on China. A 25bp Fed rate cut at the end of the month remained assured, particularly with only limited data to dissuade.

- The biggest headline out of the September FOMC minutes release is that "most" participants "judged that it likely would be appropriate to ease policy further over the remainder of this year". But that’s not a surprise given the Dot Plot, and the minutes also arguably had a bit of a cautious tone, as it portrayed a Committee that is wary but not overly concerned about the state of the labor market.

- The list of potential Fed chairs was whittled down to 5 per reports, with NEC director Hassett considered a narrow favorite over Blackrock Fixed Income CIO Rick Rieder and ex-Fed Gov Warsh, with current Fed Board members Waller and Bowman slightly behind per prediction markets.

- As we went to press, the Fed announced that next week's Industrial Production data will be postponed (was due to be published next Friday Oct 17) as the data “incorporate a range of data from other government agencies, the publication of which has been delayed as a result of the federal government shutdown.” We won’t be getting September CPI as scheduled on Oct 15, but at least the BLS announced it will publish the data on Oct 24.

- As such next week we’ll be looking at some under-covered data points, including the Redbook weekly and Chicago Fed’s CARTS retail sales data (in lieu of the Census Bureau retail sales report), with a little more focus than usual on regional Fed manufacturing indices (NY, Philadelphia).

- Once again, the dearth of tier-one data leaves Fed commentary in focus ahead of the pre-FOMC blackout period: highlights for us are Philadelphia Fed President Paulson making her first comments on monetary policy on Monday since being appointed in the summer, while as always Chair Powell bears watching on Tuesday (we also hear from Bowman, Waller, Collins, Miran, Schmid, and Musalem).

- Additionally we get the latest Beige Book which was already key given the FOMC was already increasingly focused on anecdotal information as it attempts to navigate murky economic waters.

Related stories

Related by topic

US

Employment

Minutes

China

Tariffs

Kevin Hassett

Jerome Powell

Donald Trump

CPI