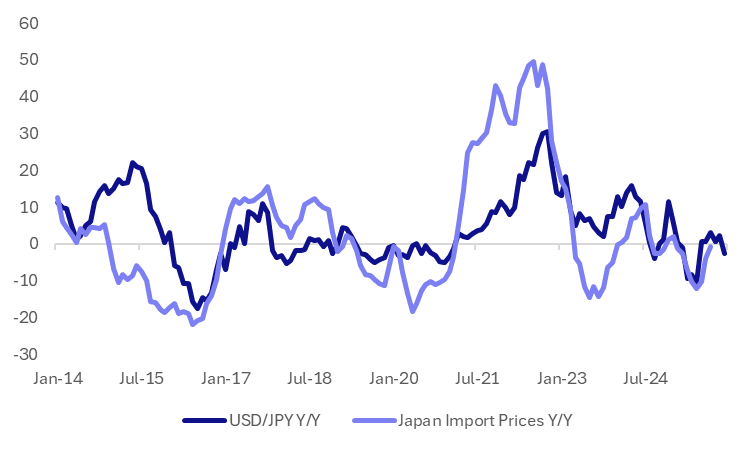

JAPAN DATA: Import Price Falls Moderating, Yen Weakness May Not Yet Be A Concern

The other part of Japan's price update this morning, was trade prices. In m/m terms, export prices rose 0.4%, matching Aug's gain. Import prices were up 0.3%m/m, the third straight monthly gain. We are off the July pace of 2.3% though. In y/y terms import prices were -0.8%y/y, against -3.9% in Aug. Disinflation from the import side continues to dissipate, which will be a BoJ watch point, particularly given renewed yen weakness. It is arguably too soon though to push the central bank to tighten rates.

- The chart below updates import prices y/y versus USD/JPY y/y changes. The USD/JPY line is extended to year end assuming current spot levels (just above 153.00 hold). Given elevated USD/JPY levels into end 2024, base effects should help keep y/y changes in the pair contained for end 2025. Higher m/m import momentum will be watched though. Sep gains were mostly evident in the commodity space, particularly metals.

- Our Japan policy team noted yesterday: The yen’s slide to an eight-month low against the dollar is unlikely to prompt a rate hike or Japanese authorities to intervene in FX markets immediately, as the weaker currency helps mitigate impacts of U.S. trade policy on exporters – a key driver of the economy, MNI understands.

- Also note, in a live TV broadcast on Thursday, Japan's new ruling party leader, Sanae Takaichi, said she has no plans to trigger an excessively weak yen and sees no immediate need to revise the 2013 BOJ accord. She noted both benefits and drawbacks of a weak yen.

Fig 1: Japan Import Prices & USD/JPY Y/Y (Assuming Current Spot Levels Prevail To Yr End)

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

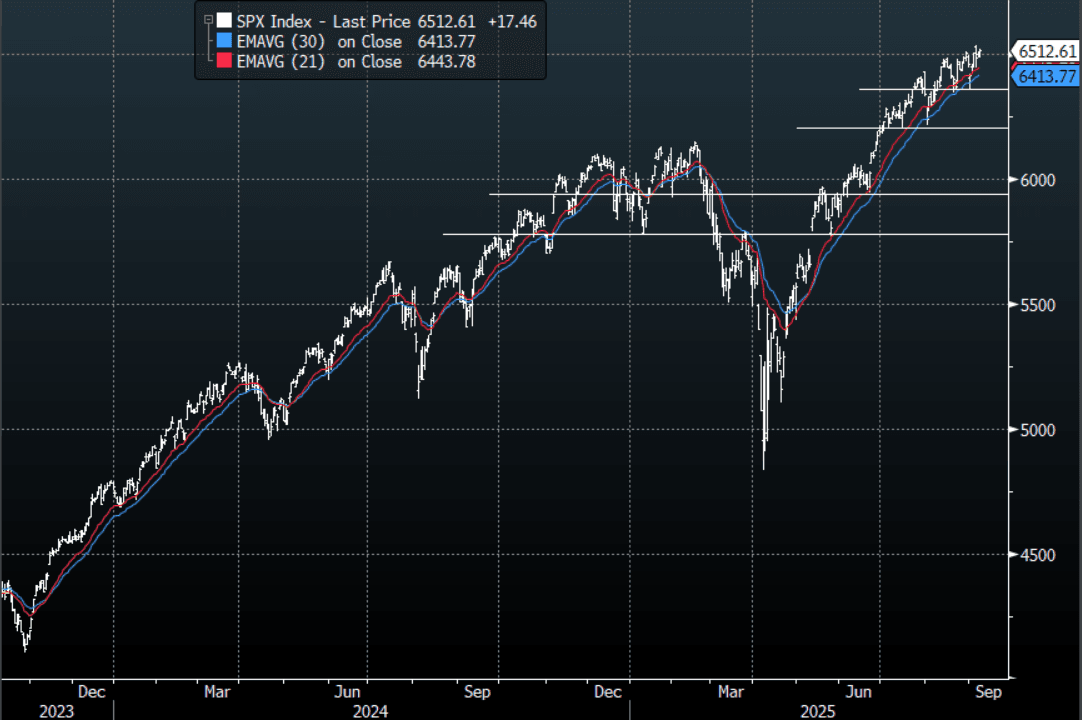

US STOCKS: S&P Back Testing All-Time Highs Even With Huge Payroll Revisions

The S&P(ESU5) overnight range was 6489.25 - 6537.25, SPX closed +0.27%, Asia is currently trading around 6533. The S&P drifted back towards its all-time highs as it shrugged off another poor labour input and kept its focus on upcoming rate cuts, ignoring the concerns for growth. This morning US futures have opened slightly higher, E-minis +0.20%, NQU5 +0.10%. The stock market looks well overdone and is in what is supposed to be a difficult seasonal period, but it remains in an uptrend and there does not look to be any imminent signs of a correction yet as it continues to grind higher.

- Jeffrey P.Snider on X: “Why the Fed will cut by fifty next week, from the Fed's own consumer survey data. It's simple math: No jobs + no tariff inflation = 50”

- Alexander Stahel on X: "Anna Wong, Economist at Bloomberg: Bottom line: The preliminary job revisions flag a strong possibility that the economy entered a recession last year, and recovered after the Fed cut rates in late-2024. Our interpretation of recent data — factoring in our estimate of future revisions — is that the labor market may have re-entered another slump in 1H25, with a low in June. We think we’re either still in recession, or in the early phase of a new business cycle.”

- Adam Taggart on X: "Hard-hitting words from Lacy Hunt: "The repeatedly and loudly proclaimed resiliency in the labor markets was wrong. Many private and public decisions were made on this extremely erroneous data. Wage and salary compensation, total personal income, private saving, GDI, national saving, industrial production, and productivity will all be revised lower since the preliminary data of all these indicators use the monthly payroll jobs which so massively over-shot actual employment growth.”

- “Today's revisions provide strong additional evidence that monetary policy is inordinately restrictive. With the labor markets as weak as now indicated, is it reasonable to question whether the corporate profits are as robust as currently believed."

Fig 1: SPX(ESU5) Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

LNG: European Gas Off Low After Israel’s Strike In Qatar

European gas prices fell 1.2% to EUR 32.68 but are up 3.3% this month. They reached a high of EUR 33.35 early in the session and then fell to EUR 32.11 but Israel’s strike on Hamas leaders in major natural gas producer Qatar drove a recovery. The US unusually reproached Israel. It seems unlikely at this stage that Qatari LNG exports will be impacted but any disruption could be a problem for Europe this close to winter. Developments will be monitored closely.

- The FT reported that President Trump told European representatives that he’s prepared to impose the same tariffs as Europe on China and India for buying Russian energy. The US will also follow the EU with any new Russian sanctions. However, Trump said he had spoken with his “good friend” Indian PM Modi.

- European LNG imports were at a 3-month high, according to Bloomberg, helping it to refill. Storage is now close to 80% full despite scheduled Norwegian maintenance.

- In terms of global supplies, there is maintenance in Australia, Africa and the Middle East but milder hurricane activity this year has meant US output has been steady. Bloomberg reports that the US Golden Pass facility should see its first LNG shipment around December.

- US gas rose 0.4% to $3.102 to be 3.5% higher in September driven by forecasts for warmer weather in mid-September which should boost cooling demand. After rising to $3.165 it fell to $3.046. Lower flows due to pipeline maintenance, which has been extended a week to 15 September, have been supportive prices.

- The EIA in its short-term energy outlook expects Henry Hub gas spot prices to rise to $3.70/MMBtu in Q4 and then average $4.30 in 2026 supported by “relatively flat” production as US LNG exports rise. US gas production in 2026 is projected to be in line with 2025.

US TSYS: Cash Open

TYZ5 is trading 113-08, down 0-03 from its close.

- The US 2-year yield opens around 3.552%, down 0.01 from its close.

- The US 10-year yield opens around 4.084%.

- MNI US DATA: For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior). Core PCE estimates are for 0.31% M/M vs 0.27% prior, with no analysts seeing core PCE printing above core CPI. That could change based on various PPI components that feed into PCE, but as it stands, the M/M core PCE estimate would be the highest since February.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

- Zerohedge on X: “If the Fed knew how bad the labor market truly was, it would have cut 25bps in March and another 25bps in June/July. There is every case to be made for a 50bps rate cut in Sept.”

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone between 4.15%-4.20%. First target the 4.00% zone then the 3.80% area.

- Data/Events: MBA Mortgage Applications, PPI, Wholesale Inventories/Sales