MNI US Macro Weekly: Hawkish December Cut Prospects Firm

Nov-28 17:20By: Chris Harrison

USFederal ReservePCEADP Report+ 1

Hidden PDF

Executive Summary

- The delayed retail sales report for September was softer than expected, with control group sales seeing their first (nominal) decline since April. We estimate a reasonably large decline in retail sale volumes in September, with weak momentum heading into Q4 after a solid Q3.

- On the flip side, core durable goods orders continued a string of solid readings in recent months with the preliminary September readings, pointing to decent momentum for production into Q4.

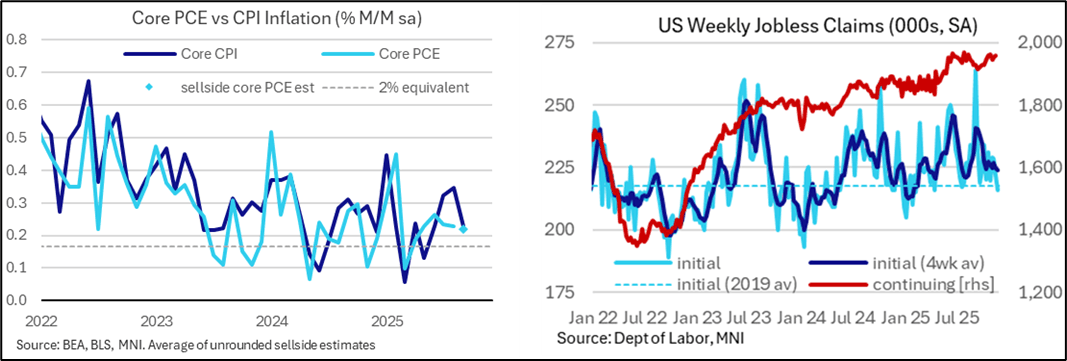

- Core PPI inflation was softer than expected back in September and broadly chimes with underlying core goods CPI inflation, with a peak for post-tariff M/M inflation pressures having come earlier in the summer (June for our median estimate on the CPI side, July for core PPI).

- Core PCE tracking has been trimmed a little further to ~0.22% M/M after 0.23% M/M in Aug and the 0.24% averaged through May-July, with scope for small upward revisions.

- Jobless claims were mixed, with particularly healthy initial claims, and on balance don’t suggest any further deterioration in the unemployment rate after September’s increase.

- The ADP update however saw a third weekly decline, pointing to a weak monthly report ahead.

- Consumer confidence saw a sharp decline in the November Conference Board survey although the labor differential at least didn’t deteriorate further.

- The 2026 fiscal year started with a larger than expected deficit in October, in what had been a wide range of expectations owing to shutdown disruption. The combination with November’s data will give a better indication of latest fiscal direction but for now the 12-month trailing deficit remains large at 5.9% GDP.

- The week’s most notable intraday shift in rates came on a Bloomberg sources piece on Hassett seen as frontrunner for Fed Chair, after Waller had earlier in the week been seen in closer contention. It prompted a sizeable rally for 2H26 contracts and onwards plus steepening in the Treasury curve.

- Fedspeak was heavily limited by the Thanksgiving holiday but saw SF Fed’s Daly support a December cut. Waller also unsurprisingly did but then warned on the January meeting being “tricky” amidst a flood of data.

- The Beige Book meanwhile reported little change in economic activity over the past six weeks whilst there were net dovish developments across employment and inflation on a breadth basis.

- Next week would ordinarily have been geared towards a NFP report on Friday but that it now set for Dec 16 as the BLS continues to work its way through the shutdown-induced data backlog. Instead, expect the myriad of labor releases starting Wednesday along with ISM surveys and monthly PCE data to help finalize market expectations ahead of the Dec 9-10 FOMC meeting, where we currently anticipate a hawkish cut.

Trending Top

Jun-26 16:22