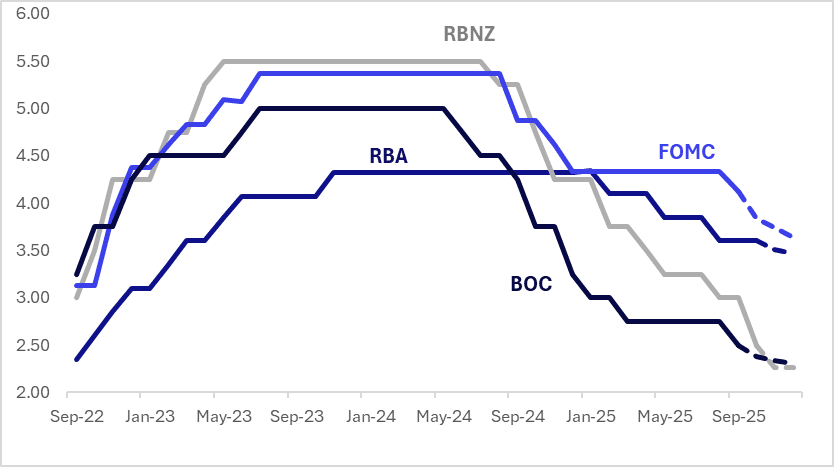

STIR: $-Bloc Pricing Little Changed Over Past Week, Except For NZ

Oct-10 01:39

Interest rate expectations across the $-bloc have shown little net change over the past week, except in NZ, which softened sharply (-12bps) following the RBNZ’s 50bp cut.

- All RBNZ board members agreed that the 50bp to 2.5% was appropriate given material spare capacity in the economy. As this negative output gap is likely to persist for some time and the economic recovery remains lacklustre, further cuts bringing policy into stimulatory territory are likely.

- The meeting record stated that the Committee remains open to further reductions in the OCR” – note the plural in “reductions”. Thus, with the recovery being lacklustre in Q3 and unlikely to surprise in Q4, another rate cut in November seems likely.

- How the economy develops before the next meeting in February will determine if more stimulus is needed. Still, it will also be the first decision with new Governor Breman at the helm.

- Looking ahead, the next key regional events are the FOMC and BOC policy decisions on October 29. Market pricing currently implies a 95% probability of a 25bps cut by the Fed and a 57% chance of easing by the BOC.

- Looking ahead to December 2025, current market-implied policy rates cumulative expected easing are as follows: US (FOMC): 3.64%, -48bps; Canada (BOC): 2.30%, -20bps; Australia (RBA): 3.47%, -13bps; and New Zealand (RBNZ): 2.26%, -24bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA AUG CPI -0.4% Y/Y VS MEDIAN -0.2%; JUL +0.0%: NBS

Sep-10 01:33

- CHINA AUG CPI -0.4% Y/Y VS MEDIAN -0.2%; JUL +0.0%: NBS

- CHINA AUG CPI +0.0% M/M VS +0.4% M/M JUL

- CHINA AUG FOOD PRICES -4.3% Y/Y VS -1.6% Y/Y JUL

- CHINA AUG NON-FOOD PRICES +0.5% Y/Y VS +0.3% Y/Y JUL

- CHINA AUG PPI -2.9% Y/Y VS MEDIAN -2.9%; JUL -3.6%: NBS

- CHINA AUG PPI +0.0% M/M VS -0.2% M/M JUL

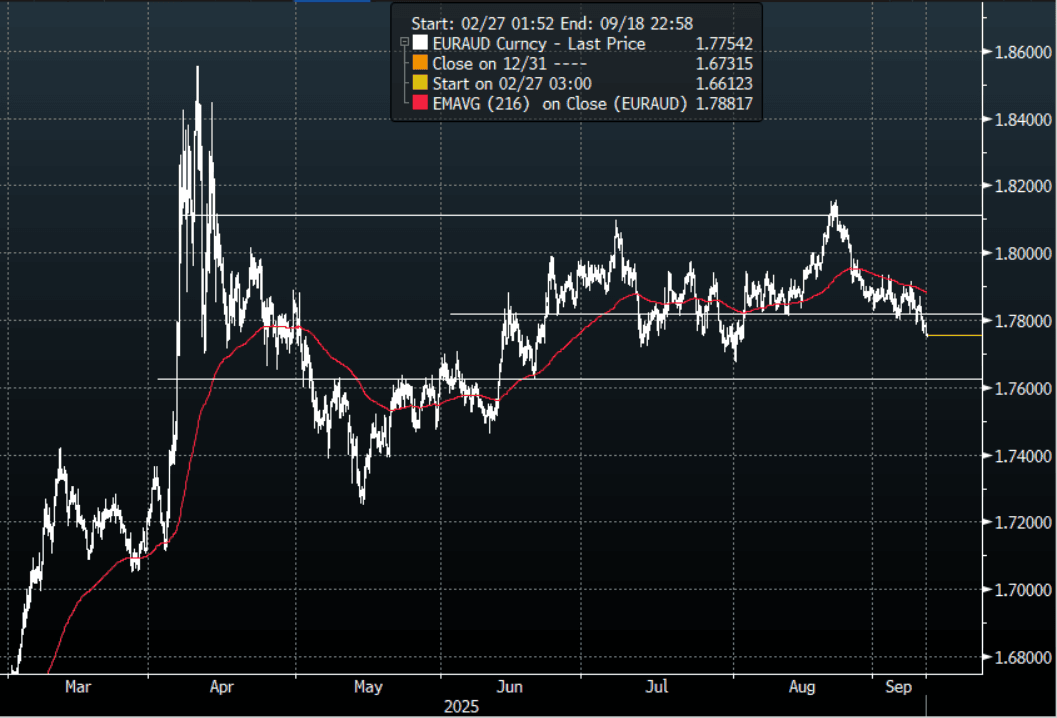

FOREX: AUD Crosses - Slightly Higher Within Ranges

Sep-10 01:28

US Equities drifted back towards all-time highs as it shrugged off another poor labour input and kept its focus on upcoming rate cuts, ignoring the concerns for growth. This morning US futures have opened slightly higher, E-minis +0.15%, NQU5 +0.05%. The AUD outperformance in the crosses quietly extends albeit within ranges.

- EUR/AUD - Overnight range 1.7761 - 1.7822, Asia is currently trading around 1.7760. The pair has broken through its first support around the 1.7800 area, below there the focus turns to the next support around 1.7600. The wider range remains 1.7600-1.8150.

- GBP/AUD - Overnight range 2.0507 - 2.0551, Asia is trading around 2.0535. The pair continues to find demand towards 2.0500, expect sellers towards 2.0700 initially. The wider range of 2.0400-2.1000 continues to contain.

- AUD/JPY - Overnight range 96.82 - 97.32, Asia is trading around 97.10. The pair topped out towards 97.50 but has consolidated its recent gains. A sustained break above 97.50/98.00 is needed to reignite the upward trend.

- AUD/NZD - Overnight range 1.1098 - 1.1116, the cross is dealing in Asia around 1.1115. The Cross is consolidating around 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: EUR/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

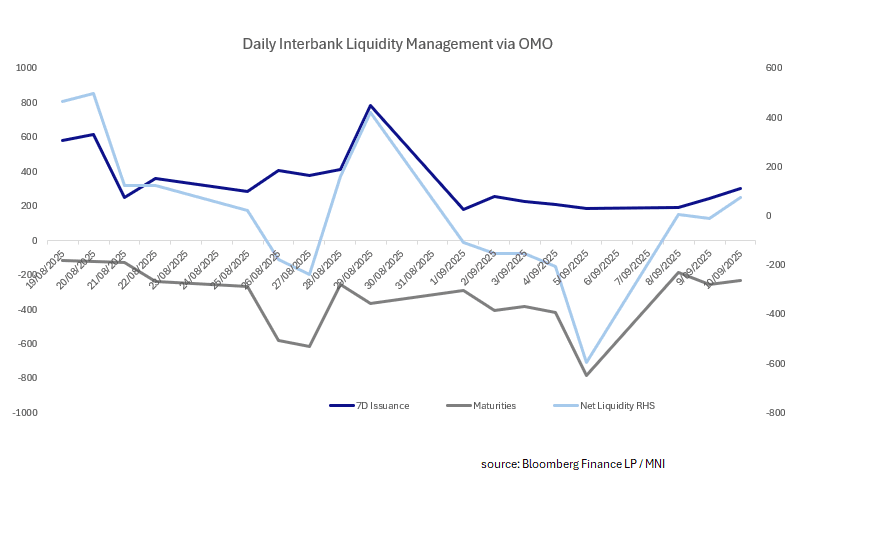

CHINA: Central Bank Injects CNY74.9bn via OMO

Sep-10 01:24

- The PBOC issued CNY304bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY229.1bn.

- Net liquidity injects CNY74.9bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.47%.

- The China overnight interbank repo rate is at 1.41%, from the prior close of 1.30%.

- The China 7-day interbank repo rate is at 1.50%, from the prior close of 1.45%.