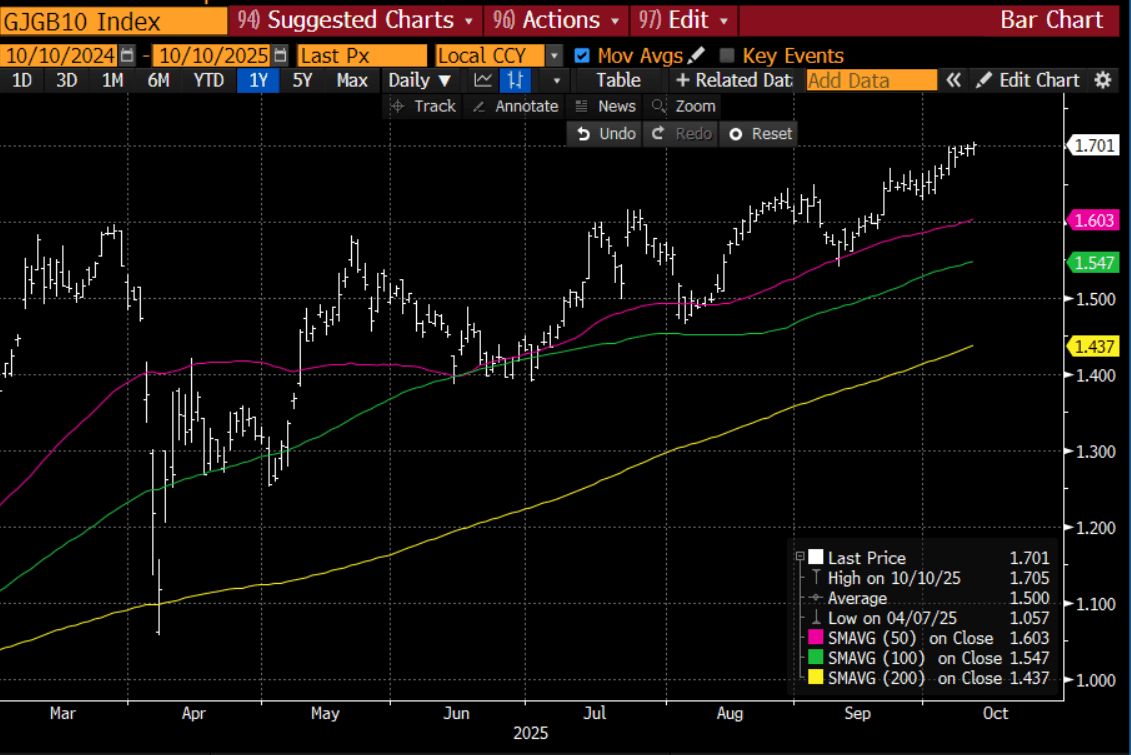

JGBS: Slightly Mixed But 10YY At Highest Since 2008

Oct-10 04:24

JGB futures are little changed, +1 compared to the settlement levels.

- Cash JGBs have continued to largely look past today's price data, with yields 0.5bp higher to 1.5bp richer across benchmarks.

- Nevertheless, the 10-year has pushed to a fresh cycle high of 1.705%, its highest yield since 2008. (See chart)

- Earlier Japan PPI data was a touch above forecasts. Moreover, disinflation from the import side continues to dissipate, which will be a BoJ watch point, particularly given renewed yen weakness. It is arguably too soon, though, to push the central bank to tighten rates.

- The benchmark 30-year yield is down 0.8bps at 3.178%, after trading in a 3.15-3.35% range this week. Even if the BOJ refrains from further rate hikes this year - with only a small chance currently priced in - we doubt long-dated JGBs would rally meaningfully, as such a move would likely be seen as a delay in tightening rather than its abandonment.

- Swap rates are, however, 1-3bps richer, with tighter swap spreads.

- On Monday, the local market will be closed.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Futures Softer, But Up From Lows, Yields Tracking Recent Ranges

Sep-10 04:22

Aussie Bond futures are holding slightly weaker, both the 10yr (XM) and 3yr (YM) off around 2.5bps. 10yr futures were last 95.69, up from earlier lows of 95.675, while 3yr futures are at 96.535, (earlier lows were 96.525). Cash ACGB yields hold around 2bps firmer across the curve, with gains close to uniform. The 3yr yield is around 3.44%, while the 10yr is just under 4.285%.

- For the 3yr yield, downside focus is likely to rest sub 3.40%, which we haven't meaningfully breached in Sep to date, while recent highs rest around 3.55%. For the 10yr, we have spent little time sub 4.20% in recent months, while topside interest has been capped above 4.40%.

- Like NZ, news/data flow has been light in Australia today.

- Tomorrow we get Sep consumer inflation expectations.

- Earlier, via BBG: "Australia sold A$1 billion ($658.8 million) of bonds due Nov. 21, 2031 on Sept. 10."

US TSYS: Asia Wrap - Yields Have Little Reaction To Cook News For Now

Sep-10 04:18

The TYZ5 range has been 113-06 to 113-09+ during the Asia-Pacific session. It last changed hands at 113-08+, down 0-02 from the previous close.

- The US 2-year yield has edged higher trading around 3.493%, up 0.01 from its close.

- The US 10-year yield has edged lower trading around 4.045%, up 0.01 from its close.

- 10-Year Yields have broken through its support as the market reacts to a labour market that is rapidly cooling. This move should now see buyers return on bounces with the first buy-zone back towards 4.20%. First target the 4.00% zone then the 3.80% area.

- MNI Policy: A federal judge Tuesday night granted a preliminary injunction blocking President Donald Trump from firing Federal Reserve Governor Lisa Cook while her lawsuit challenging her termination is resolved. The FOMC is set to meet again September 16-17.

- MNI US DATA: For PPI, current Bloomberg consensus is for a cooling after July’s hot print, with M/M final demand PPI at 0.3% (0.9% prior) and “core” (ex-food/energy/trade) also at 0.3% (0.6% prior). Core PCE estimates are for 0.31% M/M vs 0.27% prior, with no analysts seeing core PCE printing above core CPI. That could change based on various PPI components that feed into PCE, but as it stands, the M/M core PCE estimate would be the highest since February.

- Given increasing focus on labor risks it’s hard to imagine a set of inflation readings that stops the Fed from cutting 25bp as expected, but it could help shape the updated rate and economic projections to be released at the meeting (including the 2025 “dot” median), as well as Chair Powell’s tone.

- Data/Events: MBA Mortgage Applications, PPI, Wholesale Inventories/Sales

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

CHINA: Bond Futures Lower in Morning Trade

Sep-10 04:15

- China's bond futures are down this morning with the 10-Yr leading.

- The 10-Yr is down -0.16 at 107.62 to move further below all major moving averages.

- The 2-Yr is down -0.04 at 102.35 to also move further below all major moving averages.

- The 10-Yr CGB is at 1.79% after last night's close of 1.81%