JGBS: Firmer As Komeito Withdraws Support For LDP

JGB futures initially add ~15 ticks after headlines suggest the Komeito Party is set to withdraw from the ruling coalition with the LDP.

- Contract then fades from session highs as the market begins to assess the potential for fresh elections in Japan.

- A reminder that the “Takaichi trade” was initially JGB-negative owing to assumptions surrounding the new LDP Party leader’s expansionary fiscal preferences.

- Initial resistance in the JGB futures lies at 136.08, high of 136.02 seen so far.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: DXY Ticks Lower, Antipodeans Outperform

The broader USD trades on the backfoot early on Wednesday, with headlines noting that President Trump cannot fire Fed Governor Cook for cause at this stage doing little to support the USD (potential for ongoing Trump-related headline risk on that front may be lifting uncertainty and adding weight to the greenback).

- Upticks in global equity markets will also be weighing on the USD, while also helping explain the outperformance for the AUD & NZD amongst G10 FX.

- Zooming out, JPY, EUR & GBP are little changed vs. the USD on the day after recovering from Asia lows.

- EUR/USD based at 1.1690 before a recovery to 1.1710. Initial support at the 20-day EMA (1.1674) went untouched, leaving the bullish technical theme in the pair intact.

- USD/CNH threatened to test yesterday’s lows in recent trade, before a recovery to 7.1180. China’s Finance Minister stressed China’s commitment to using all its proactive fiscal policy space, along with vowing to stabilise international trade and domestic employment conditions. There wasn’t much new in the headlines given by Xinhua.

- Contained reaction in Scandi FX following this morning’s Norwegian CPI & Swedish consumption & production data (see recent bullets for more details).

- U.S. PPI data headlines today’s macro calendar, ahead of CPI data due Thursday.

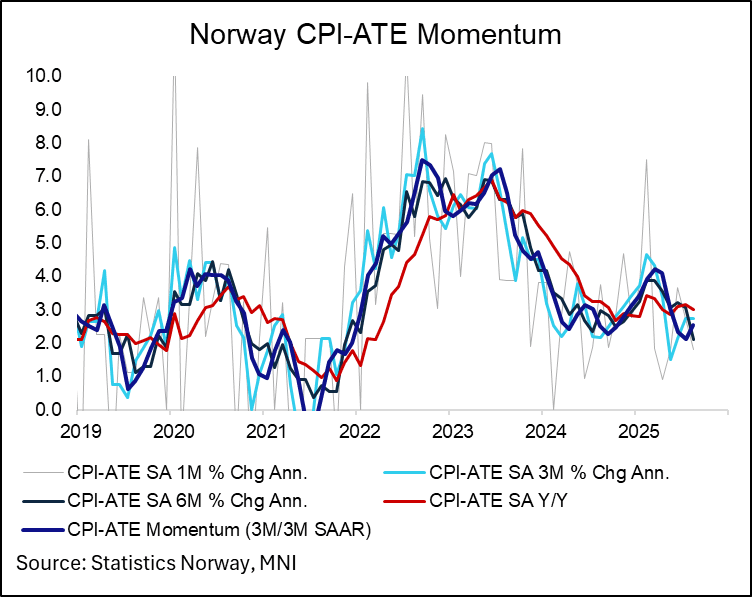

NORWAY: SA CPI-ATE Inflation Consistent With 2% Annualised In August

On a seasonally adjusted basis using Statistics Norway data, CPI-ATE inflation rose 0.15% M/M, after 0.22% in July and 0.30% in June. When annualised, this is a rate slightly below 2%. As such, we think it is consistent with the view that while August inflation was stronger-than-expected, it isn’t enough to stand in the way of a September rate cut in isolation. Tomorrow’s Regional Network Survey remains very import.

- 3m/3m annualised inflation momentum rose to 2.52% in August (vs 2.12% prior) because the March – May period was characterised by soft M/M SA inflation rates averaging 0.13%.

- These rates remain below the 3-4% range seen at the start of this year (which caused Norges Bank to delay its plans for a March rate cut).

EQUITY TECHS: E-MINI S&P: (U5) Northbound

- RES 4: 6617.73 2.0% 10-dma envelope

- RES 3: 6600.00 Round number resistance

- RES 2: 6543.75 2.00 proj of the Apr 7 - 10 - 21 price swing

- RES 1: 6541.75 High Sep 5

- PRICE: 6538.75 @ 07:23 BST Sep 10

- SUP 1: 6462.58/6371.75 20-day EMA / Low Sep 2

- SUP 2: 6365.35 50-day EMA

- SUP 3: 6313.25 Low Aug 6

- SUP 4: 6239.50 Low Aug 1 and a key support

A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirmed a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6456.35, the 20-day EMA.