MNI EUROPEAN MARKETS ANALYSIS: USD Follows Broader Risk Trend

- Risk sentiment started the session off very poorly. Carry over negative sentiment in the equity space weighed on US futures (amid on-going AI capex concerns), while silver and bitcoin fell sharply. Sentiment improved though, albeit without an obvious catalyst. Silver is +15% above earlier lows, but still off around 12.5% for the week.

- The USD BBDXY index rose to 1197 in early dealings but sits back under 1194 now. Regional equity market sentiment is mostly under pressure, particularly in the tech space.

- With no NFP later, focus will be on Canadian employment data, as well as preliminary reads of UMich sentiment and inflation expectations.

MARKETS

US TSYS: Futures Move Suggest PF Rebalancing, Equity Vol Key to Next Move

An unsurprisingly modest day for USTs today following the dramatic moves overnight. Moves in Asia today appeared more positioning related rather than any follow on from the fall in yields. Bond markets are sensitive to data misses for now as the 'Warsh Premium' moderates for now, with non farm payrolls next in the queue on the 11th.

Bond futures are up across maturities with the 10-Yr higher by +06 at 112-09+, now by +0-15 for the week. Volumes were high today yet given the relative minor moves in price, back up the idea that most activity was attributed to rebalancing.

Cash was mostly higher in yield with yields up between +0.2bps and +1.0bps, with the front end underperforming.

- The 2-Yr is up +1.2bps at 3.467%

- The 5-Yr is up +0.7bps at 3.727%

- The 10-Yr is up +0.8bps at 4.19%

- The 30-Yr is up +0.7bps at 4.85%

University of Michigan Sentiment indexes are in focus tonight alongside US$89bn 13-week and US$77bn 26-week auction.

Vice Chair Jefferson is scheduled to participate in a discussion hosted by the Brookings Institution in Washington focusing on "Supply-Side Factors and Inflation"

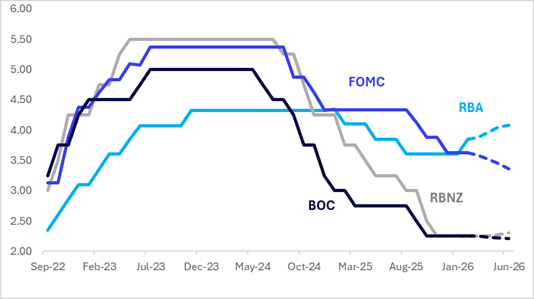

STIR: AUS Is A Hawkish Outlier In The $-Bloc

Interest-rate expectations across the $-bloc over the past three weeks, looking out to June 2026, have softened slightly, with the notable exception of Australia, where expectations firmed by 27bps. Elsewhere, US and Canada pricing moved 7bps and 3bp lower, respectively, while New Zealand nudged 2bps higher.

- The key event of the past week was the RBA’s decision to hike interest rates by 25bps to 3.85% on Tuesday.

- The RBA raised the cash rate to 3.85%, as expected by the sell-side consensus and which was largely priced by the market (around 75% priced in per OIS markets prior to the decision). The decision was unanimous by the board. The risks appear skewed towards further action to ensure that inflation moves sustainably back into the target band of 2-3%. (see MNI RBA Review here).

- RBA Governor Bullock was before the Australian Parliament this morning and stated that the RBA is watching inflation risks, particularly in terms of how much of the recent uptick is temporary versus persistent, and in turn capacity constraints, which will be the key watch points around further tightening.

- The next major regional policy event is the RBNZ meetings on 18 February. No tightening is priced for February, while December 2026 assigns 43bps.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.36%, -26bps; Canada (BOC): 2.21%,-4bp; Australia (RBA): 4.08%, +23bps; and New Zealand (RBNZ): 2.33%, +8bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JAPAN: MNI Publishes Election Preview

Access Full Report Here

Japan holds a snap general election for the lower chamber of the National Diet, the House of Representatives, on Sunday, 8 February. The contest comes as part of an effort by Prime Minister Sanae Takaichi to reinforce her position as president of the governing Liberal Democratic Party (LDP) and take advantage of strong personal approval ratings to secure a majority in the lower House. Since winning the LDP presidency and taking over from Shigeru Ishiba, becoming Japan’s first female prime minister in October 2025, Takaichi has pursued a more robust stance in regional foreign policy and advocated for a “responsible proactive fiscal policy”. Markets will be watching the election closely for signs of whether Takaichi emerges emboldened or chastened from taking such a political gamble.

In this Election Preview, we outline the electoral system for the House of Representatives and the main parties contesting the vote, put together a chartpack of relevant opinion polling and predictions market odds, provide analysis of potential post-election scenarios with assigned probabilities, an outlook for the election from a financial market and macro perspective, and a round-up of analyst views on the vote.

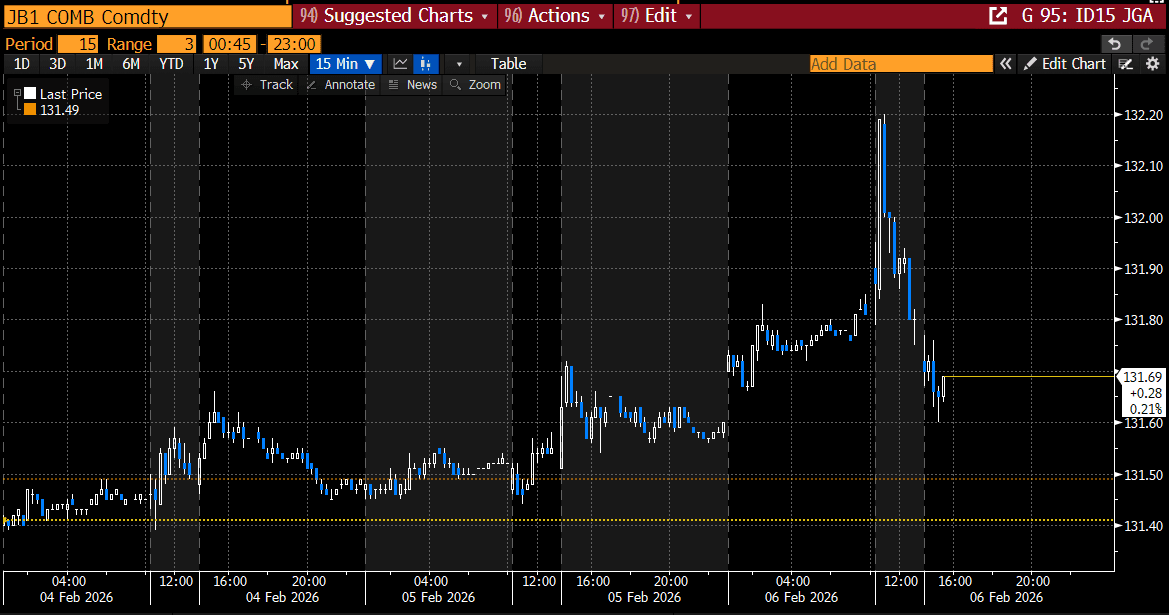

JGBS: Early Gains Pared As Risk Assets Rebound

JGB futures are little changed, -2 compared to settlement levels, after giving strong early gains as market partially unwound yesterday’s risk-off sentiment.

- MNI: Bank of Japan board member Kazuyuki Masu said on Friday that the BOJ needs to raise the policy rate in a timely manner to ensure underlying inflation remains below 2%, but he did not give a timeline. “Although the underlying inflation rate remains below 2%, it is drawing very close to the 2% target,” Masu told business leaders in Matsuyama City. He added that Japan has entered an inflationary phase as deflationary behaviour gradually unwinds.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday’s risk-off induced bull-steepener.

- Cash JGBs 1-2bps richer across benchmarks. The benchmark 30-year yield is 1.2bps lower at 3.558% after being 3.517% earlier.

- Swap rates are flat to 2bps higher, with a steeper curve.

- On Monday, the local calendar will see Cash Earnings, Current Account and Trade Balance, and Bank Lending data.

Source: Bloomberg Finance LP

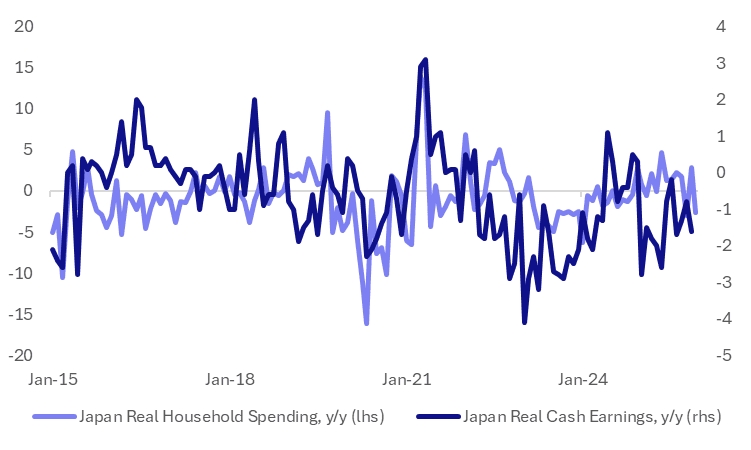

JAPAN DATA: Household Spending Slumps Back Into Negative Territory

Japan Dec real household spending was much weaker than consensus forecasts. We printed at -2.6%y/y, versus the -0.3% forecast and +2.9% prior outcome. In m/m terms, real spending fell by 2.9%. Income was flat y/y, after a -2.2% fall in Nov. The chart below plots real household spending y/y against real labour earnings (also y/y). The fall in spending moves it back more into line with real wage trends, which remain in negative territory (last print for the wages series is Nov, we get the Dec print next Monday). Sustained positive real wages gains remains a key focus point for the government and BoJ (around sustainably achieving its inflation target). Today's outcome is unlikely to add anything to near term BoJ hike expectations. It still suggests a near term wait and see approach.

Fig 1: Real Household Spending Falls, Wages Data Remains Negative

Source: Bloomberg Finance L.P./MNI

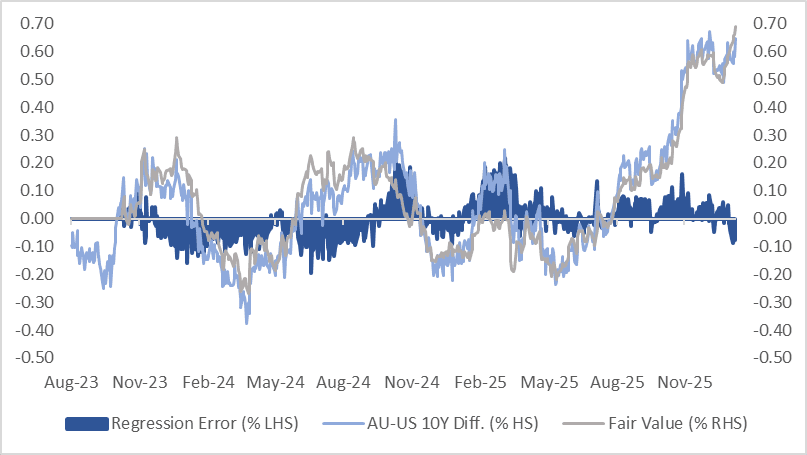

AUSSIE BONDS: Richer But AU-US 10Y Diff Back At Cycle High

ACGBs (YM +3.5 & XM +3.0) are stronger but off session bests as risk assets rebounded from yesterday’s carnage. Silver and Gold are 1% and 3% stronger, NDX and SPX futures have pared early losses while Bitcoin is up ~2%.

- In her testimony before the Australian Parliament this morning, RBA Governor Bullock stated the RBA is watching inflation risks, particularly in terms of how much of the recent uptick is temporary versus persistent, and in turn capacity constraints, which will be the key watch points around further tightening.

- While the cash ACGBs are 3bps richer today, the AU-US 10-year yield differential has returned to its cycle high of +65bps.

- Since early December, price action has effectively consolidated the differential’s 50-65bps trading range following the breakout above the ±30bps range that had prevailed since November 2022. This widening has coincided with a steady lift in market-implied expectations for the RBA cash rate.

- The bills strip has bull-flattened, with pricing +1 to +6 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 94% by June and 149% by December 2026.

- On Monday, the local calendar will see Household Spending data.

Bloomberg Finance LP

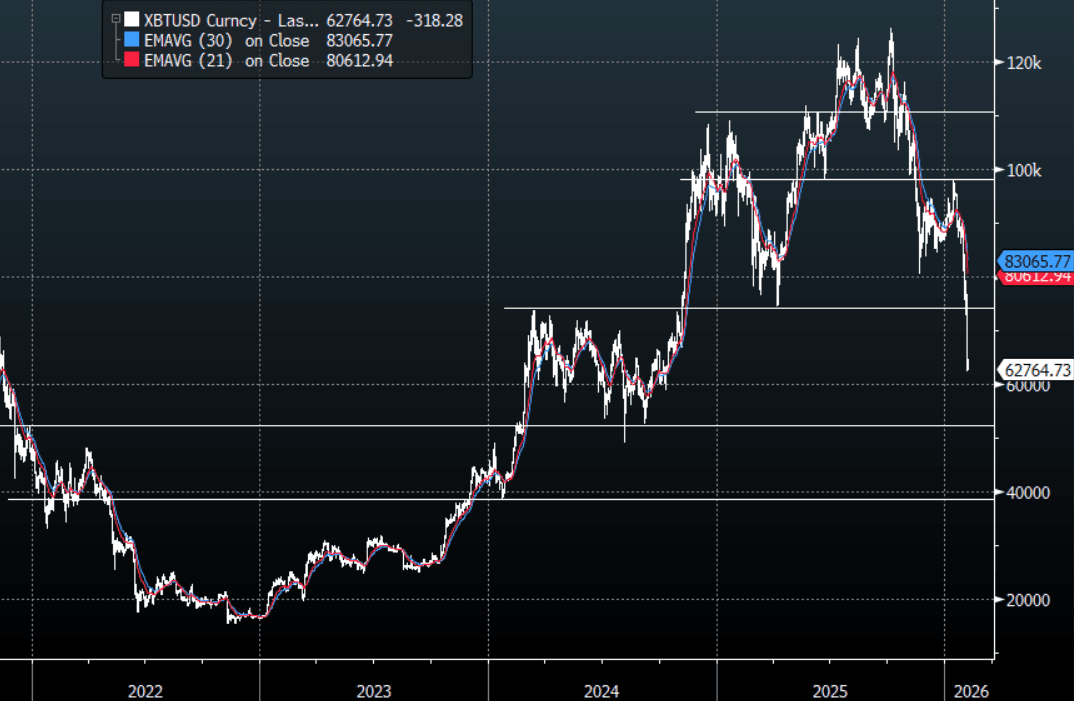

CRYPTO: Bitcoin - Collapses Through $68-$70 As De-Leveraging Intensifies

Bitcoin had a range overnight of $62,266.70 - $71,830.50, Asia is currently trading around $62700, -0.70%. Bitcoin has collapsed back through the $68k-$70k support and extended lower as de-leveraging picks up across the board, playing catch up to the moves in Metals. The price action looks appalling and reeks of people capitulating. So much for dipping your feet in the pool around $70k, this break now opens up a test of $50k-$55k next ahead of what many are calling the target for this move toward the $35k-$40k area. For now the bear trend is firmly back in place and rallies will likely be sold into, the first sell-zone is toward $70k-$74k and then the $80k-$85K area.

- Andy Constan on X on what he would be asking on MicroStrategy's earnings call: “ask them how they will pay the dividends and what yield are they willing to pay for the Strc. What happens to the company at a negative MNAV and unacceptable dividend yields required for issuance.”

- Niko Ludwig on X: “MSTR’s unrealized BTC profit of ~$33B has swung into a ~$4B loss. Per BTC pricing: October 6th: $126,210, Today: $67,251 (-47%)”

- The Market Ear on X: “This isn’t extreme yet — Bitcoin’s “normal” drawdown math still points to $38k.”

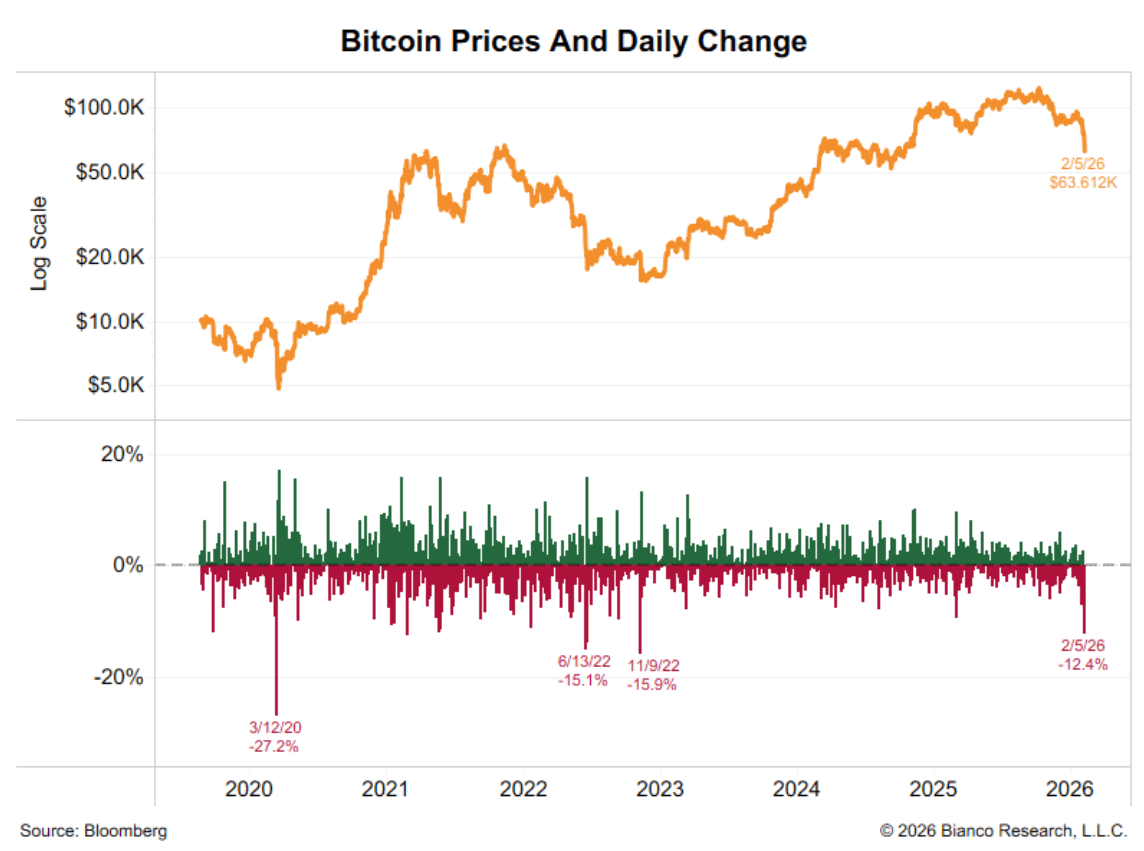

- Jim Bianco on X: “The $BTC carnage is accelerating. Now down 12+% today. Now the 4th worst day this decade. The other 3 were days around something "breaking." So, what is "breaking" now? Nov 9, 2022, FTX failure, Jun 13, 2022, Terra Luna Collapse, Mar 12, 2020, worst of COVID Shutdown.” See Fig Fig.1

- Bitcoin’s Average True Range(ATR) for the last 10 Trading days: $4,007

Fig 1: Bitcoin Daily Change

Source: MNI - Market News/Bloomberg Finance L.P/Bianco Research

Fig 1: Bitcoin spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: USD-Breaks Above 1195 In Early Trade, Can't Extend And Fills In The Gap

The BBDXY has had a range today of 1194.36 - 1197.11 in the Asia-Pac session; it is currently trading around 1194. The USD is trying to build on its recent gains, as we see mass de-leveraging of risk across the board. The USD gapped above 1195 as the rout continued in early Asian trading, it has since pared back all of those losses and filled the gap back toward 1194. I suspect that bounces will continue to find sellers in the short-term as the USD still has few friends, but the caveat being is whether we have a deeper correction in Stocks will the USD safe haven bid come back ? The market is not positioned for this. On the day, the first resistance is toward the 1198-1202 area and I suspect we could see buyers now on dips back toward the 1189-1192 area initially.

- EUR/USD - Asian range 1.1766-1.1792, Asia is currently trading 1.1790. Price action has left an ugly bearish shadow on the weekly chart, but we are approaching levels that could start to see some buyers return. On the day, the support between the 1.1760-1.1790 area continues to hold for now, a move through here could signal a deeper reversion back to the important 1.1650-1.1700 area where I suspect buyers would again be around. On the day watch for sellers back toward the 1.1810-1.1840 area as the pair looks to consolidate and the market tries to get some conviction on how it thinks the USD will trade from here.

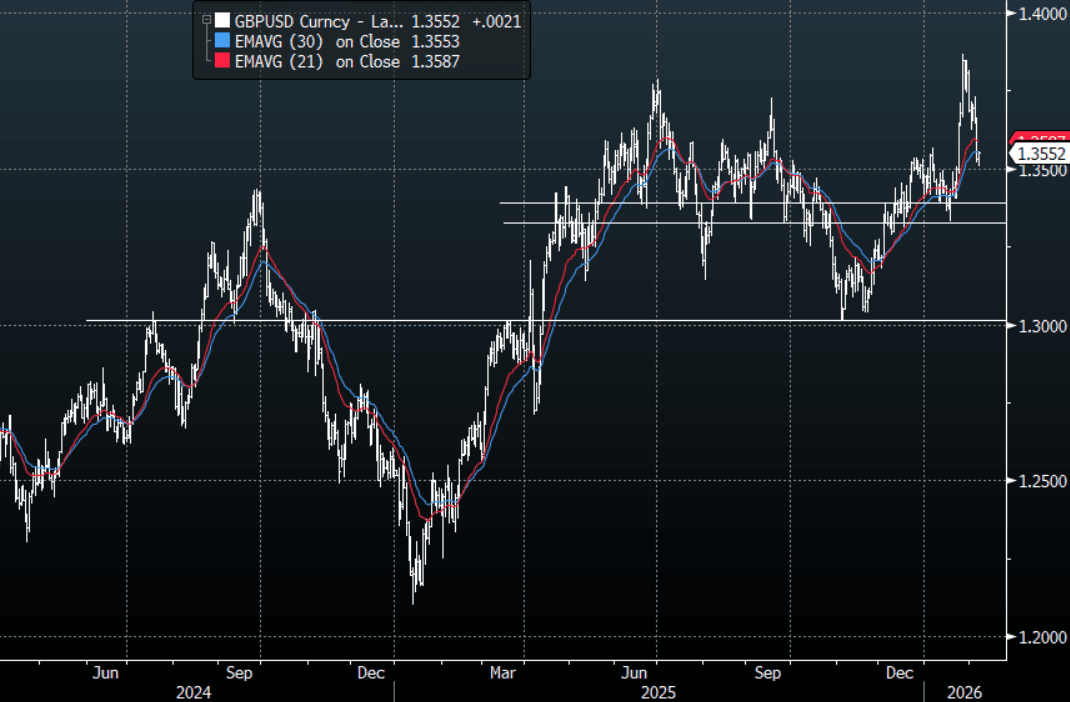

- GBP/USD - Asian range 1.3509-1.3554, Asia is currently dealing around 1.3550. The pair like everything else had an ugly weekly close leaving a clear rejection of the 1.3850 area. The pair had another leg lower as the dovish hold added to the already stiff headwinds from global risk. It is now challenging the 1.3500 area and any GBP bulls left will need this 1.3400-1.3500 area to find some demand if it is to find a base from which to move higher again.

- Cross asset : SPX -0.40%, Gold $4830, US 10-Year 4.18%, BBDXY 1194, Crude Oil $63.66

- Data/Events : France Current Account Balance, Germany Industrial Production SA/Trade Balance SA, EZ ECB Survey of Professional Forecasters, Spain Industrial Production

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

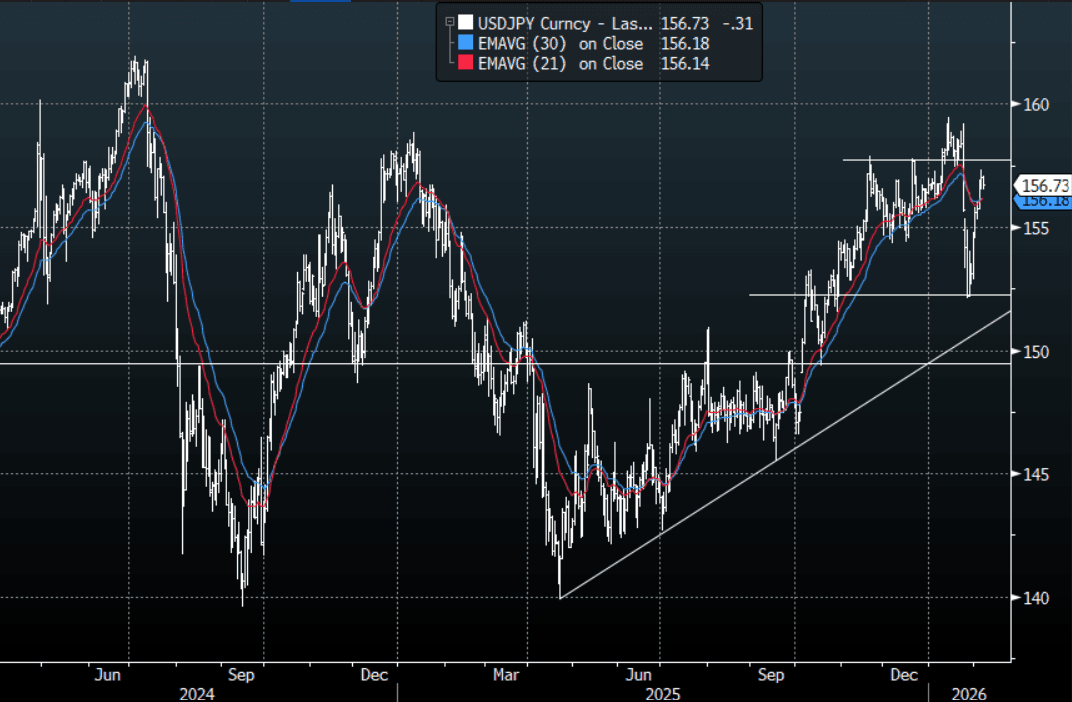

JPY: USD/JPY - Treading Water Below 157.00 Going Into The Weekend

The USD/JPY range today has been 156.52 - 157.10 in the Asia-Pac session, it is currently trading around 156.70, -0.20%. USD/JPY looks to be consolidating just below 157.00 as we head into the weekend's elections. The large move lower was more down to overextended positioning than fundamentals and as we head toward this weekend's election all the reasons for the Yen short have come back to the fore. This should keep USD/JPY well supported on dips now as the market looks toward the 160.00 area once again. It stalled above 157.00 overnight but I suspect a dip back toward the first support around 155.75-156.25 should find buyers first up.

- MNI: BOJ's Masu Sees Timely Hikes To Keep Inflation Below 2%. Bank of Japan board member Kazuyuki Masu said on Friday that the BOJ needs to raise the policy rate in a timely manner to ensure underlying inflation remains below 2%, but he did not give a timeline.

- “Donald Trump said he would meet with Sanae Takaichi at the White House on March 19. He also endorsed the PM’s coalition in Japanese elections set for Sunday.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($991m), 157.00($808m). Upcoming Close Strikes : 156.50($938m Feb 11), 157.00($754m Feb 10), 158.25($773m Feb 11) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 130 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

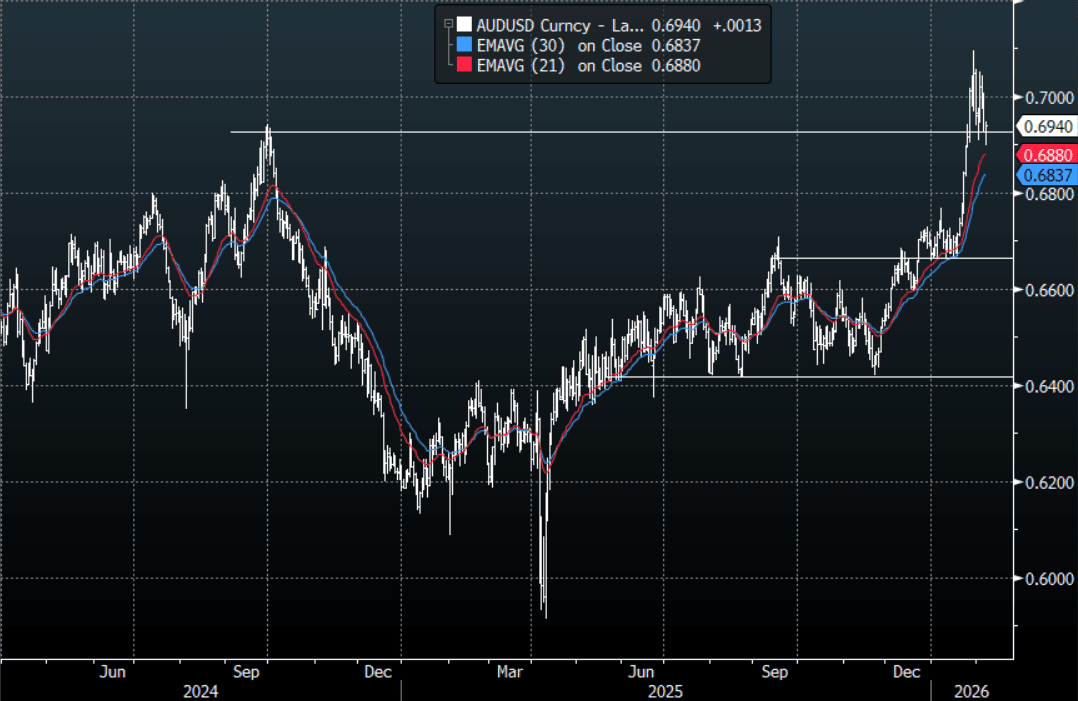

AUD/USD - Pares Back Early Losses As 0.6900 Finds Demand First Up

The AUD/USD has had a range today of 0.6897 - 6947 in the Asia- Pac session, it is currently trading around 0.6940, +0.15%. The AUD got hit hard early as the Asia open gapped lower following on from the rout overnight in risk, as the market settled and pared back some of its early losses the AUD drifted back to where it opened. The AUD has come under pressure as the risk-off back-drop has started to broaden with Crypto deciding Metals could not have all the fun and collapsed over 12%. US Stocks are again under pressure as Tech begins to falter, this time the broader market is not balancing out the move. The AUD has been outperforming across the board recently as leveraged funds add to their longs as further hikes are priced in, this move in risk could make these positions vulnerable in the short-term. On the day, the support back toward the 0.6850-0.6900 area proved to be solid at the first attempt. Should this first support give way the test of the pivotal 0.7100-0.7200 area will be delayed for now.

- Bloomberg - “Australia’s central bank chief said the interest-rate setting board is “monitoring closely” whether a recent surge in inflation is being driven by temporary or more persistent factors after it raised borrowing costs this week.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6875(AUD913m), 0.6950(AUD864m). Upcoming Close Strikes : 0.6900(AUD1.74b Feb 9), 0.6900(AUD1.22b Feb 10), 0.7100(AUD1.09b Feb 10) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 79 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

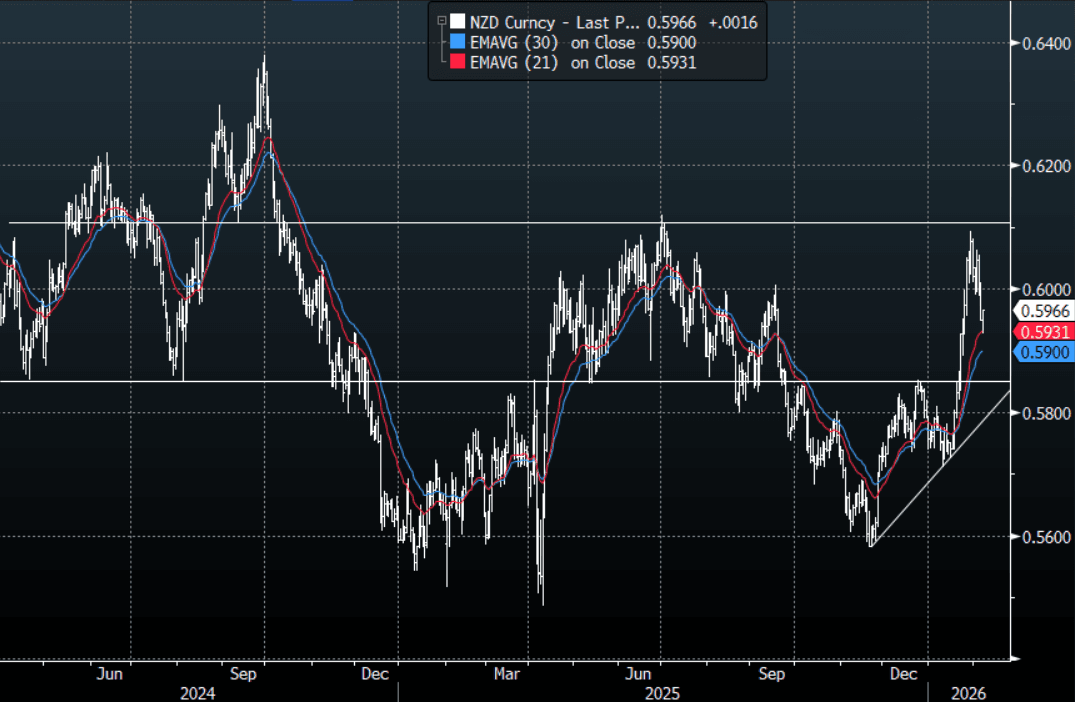

NZD/USD - Finds Buyers Toward 0.5900 As Risk Pares Back Early Losses

The NZD/USD had a range today of 0.5928-0.5967 in the Asia-Pac session, it is currently trading around 0.5966, +0.30%. The NZD got hit hard early as the Asia open gapped lower following on from the rout overnight in risk, as the market settled and pared back some of its early losses the NZD regained those losses and moved back into positive territory. The NZD has come under pressure as the risk-off back-drop has started to broaden with Crypto deciding Metals could not have all the fun and collapsed over 12%. US Stocks are again under pressure as Tech begins to falter, this time the broader market is not balancing out the move. On the day, the NZD is trading heavy back under 0.6000, and how risk trades going into the weekend will determine if we have another look toward the 0.5850-0.5900 area. This ugly rejection above 0.6000 looks to have put the test of 0.6100 on hold for now.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 60 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: AI /Tech Weighs on Kospi, JCI Struggles on Moody's Warning

- As regional bourses all suffered today, Japan held on to modest gains and is up on the week thanks to AI / tech sectors ignoring overnight leads, with Softbank up +1.75% today. The Nikkei has held onto +1.1% for the week, outperforming regional peers. China's bourses haven't faired as well with the Hang Seng down over -1% and almost -3% for the week. Metals and bitcoin deleveraging have impacted the HSI with defensive sectors in demand ahead of the upcoming lunar new year.

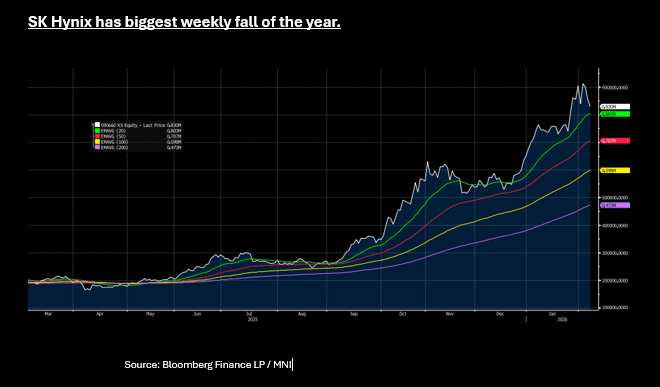

- The KOSPI traded in a range of 4,900 to 5,120 Friday but ultimately is down over -2.8% at 5,010 as the AI tech volatility continues. SK Hynix opened the day lower by almost -6% only to see dip buyers emerge. It is currently down -3.1% today and -8% for the week, it's biggest weekly fall this year.

- As the Reserve Bank of India held rates as expected, a modest upgrade to growth was not enough for the NIFTY to shake regional trends and is down -0.35% Friday. Despite that, the positive sentiment from the US tariff deal sees the index leading regional peers with gains of almost 3% for the week.

- Grey clouds still remain for the JCI with ratings agencies the latest to air their concerns. The JCI opened up strongly before giving way to the news from Moody's. It is currently down -2.8% and on track for a second week of losses, down over 5%.

ASIA STOCKS: South Korea Sees Large Outflow On Record, Further Outflows Today

Yesterday's EM Asia flow update was dominated by tech related outflows, as sentiment continues to deteriorate in this space. The $3.6bn in net outflows from South Korea looks to be a daily record per the BBG data sourced from local exchanges. It also brings the 5-day sum of net outflows to near $7bn, a very heady sum for the past 5 trading days. We have seen some dip buyers emerge for the likes of Samsung and SK Hynix so far but sentiment remains fragile. Concerns around the large AI capex cycle (how this translates into revenue etc), along with broader deleveraging, leaves tech sensitive plays in Asia still vulnerable (today, per NBUY on BBG has seen another near $1.5bn in offshore outflows from South Korea). The 12 month rolling sum of South Korea flows is negative, close to -$8bn, but the trough last year was around -$25bn. Taiwan is seeing similar risks, although hasn't seen the same degree of outflow pressures in 2026 to date.

- Elsewhere, flow trends were mixed yesterday. Indian inflow momentum remains positive, but is coming from a low base and global equity jitters may slow further inflows even after this week's earlier good trade news.

- Indonesian outflows continue, with added fresh downside today after Moody's downgraded the Indonesia credit outlook late yesterday. At this stage, the JCI is off close to 2% and the index under 8000.

- Thailand inflows remain positive, with eyes on this week's election. The SET is eyeing an upside test through 1350.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2026 To Date | |

| South Korea (USDmn) | -3612 | -6757 | -4837 |

| Taiwan (USDmn) | -2268 | -4488 | -1060 |

| India (USDmn)* | 121 | 1034 | -2426 |

| Indonesia (USDmn) | -28 | -215 | -685 |

| Thailand (USDmn) | 131 | 211 | 379 |

| Malaysia (USDmn) | -16 | -62 | 229 |

| Philippines (USDmn) | 0 | 14 | 239 |

| Total (USDmn) | -5673 | -10264 | -8160 |

| * Data Up To Feb 4 |

Source: Bloomberg Finance L.P./MNI

Oil Posting Weekly Losses as US Iran Meeting Approaches

- Despite modest gains Friday during the Asia trading day, oil is currently down over .1-5% for the week following significant falls earlier.

- WTI has traded in a US$62.31 - $63.85 range today, currently near session highs at $63.72 bbl, for gains of +0.66%. Price action however is modest as traders look ahead to Friday in the Middle East where US and Iran representatives meet.

- It is unlikely that any ground breaking 'deal' will be announced given the pushback from Iran leading in recent weeks. Trump did suggest Iran is already 'negotiating' leading to earlier declines. However news of the Saudi cut in prices for Asia buyers being less than expected, was interpreted as a positive signal for oil demand as it pushed back in afternoon trade.

- Brent is up +0.50% today but lower by almost -4% for the week. Brent opened lower in Asia reaching $66.87, rallying up to $68.12 before settling to $67.93. $68 seems a key resistance here for Brent and would likely require negative headlines from the meeting Friday to see it push beyond and hold above that level.

- Shorter term momentum indicators are trending more neutral at present, suggesting that the US Iran risks are more balanced for now, but negative headlines seem likely to provide more of an impact. The more neutral momentum indicators suggests trader's outright views remain mixed at best with likely limited expectations for any immediate break throughs.

- Shell reported a slump in fourth-quarter profits, citing weaker crude prices and poor oil trading performance, which weighed on broader energy market sentiment as it announced a pause in investment in Kazakhstan, amidst a legal dispute with the country which could cost the company billions.

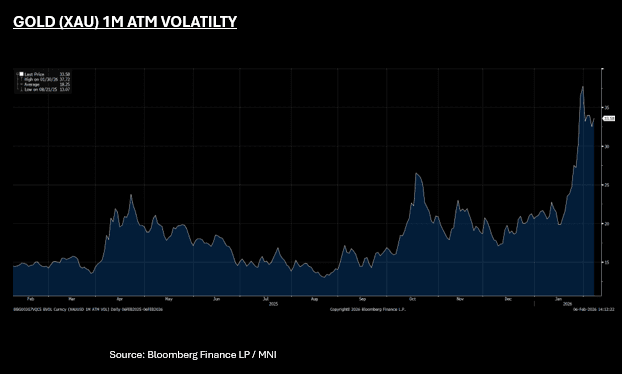

GOLD: Weakening Bias Remains, Equity Moves Giving Some Support

- Gold is up modestly Friday but remains down c.10% from an all-time high reached last week. The reversal came after gold and silver saw strong rallies in January, both reaching successive record highs. The markets were ably supported by speculator buying, geopolitical turmoil and concerns about the Federal Reserve’s independence.

- The rally came to an abrupt halt at the end of last week, with bullion plunging the most in more than a decade and silver recording its biggest daily drop on record.

- This has sent shockwaves through gold markets with platforms in China having liquidity crises and CME upping their margin requirements.

- Gold's 1 month At the Money Volatility (a commonly used volatility measure) averaged 16 for much of 2025, before jumping to a high of 37 last week.

- Gold is up Friday by 1% yet remains down by -1.5% for the week, and has traded in a US$4,655 - $4,846 range throughout the trading day. Equity weakness across the region is giving gold some support in the afternoon, but the weakening bias remains for now. Expect more volatility in the near term as markets adjust from a wild weak for precious metals.

INDIA: RBI on Hold, Governor Calls it a Wait and See Approach

- As we expected, the RBI held rates steady today at 5.25% with unanimous vote, maintaining their focus on prior policy adjustments. The MPC noted that the transmission of previous rate cuts to bank lending rates is still in progress, and further immediate easing might be premature until the full effects of the 125 bps cumulative reduction are realized.

- The RBI raised its GDP growth forecast for FY26 to 7.4% (up from 7.3%), noting that domestic momentum remains resilient and is supported by a growth-focused Union Budget and upside potential from the US trade deal

- Headline inflation remains benign (projected at 2.1% for FY26), the RBI revised its FY27 projections slightly upward to 4% for Q1 and 4.2% for Q2, necessitating a cautious stance to ensure price stability remains within the target band.

- The central bank maintained its immediate focus toward active liquidity management rather than further rate actions, aiming to address tight banking system liquidity and stabilize the yield curve

- IGB 10-Yr is up on the day, climbing +4.5bps to 6.696% whilst the NIFTY 50 is down -0.45% in early trade, following regional leads.

- We expect further focus on liquidity to translate to more injections in the coming months via OMO. Swaps have little priced in the near terms but have the potential to re-price in the coming weeks as volatility declines.

- RBI next meeting details are yet to be released.

ASIA FX: CNH Ignores Risk Gyrations, USD/KRW Fades +1470 As Risk Stabilizes

Most USD/Asia pairs are off earlier highs, as broader risk appetite has stabilized from the earlier sharp risk off moves. We started the session with weakness in Silver, gold and Bitcoin, while US equity futures were also in red. We are away from these extremes, with Bitcoin and Silver now comfortably up for the session (silver is now up 14% from earlier lows). Regional equity sentiment is still mostly softer though, particularly in tech sensitive plays like South Korea and Taiwan. Broader tech equity concerns has seen very strong outflows from South Korean equities this week.

- Spot USD/CNH holds under 6.9400 in latest dealings, very much immune to the broader risk gyrations. We are only 100pips above recent cycle lows, although broader USD index levels are off earlier Friday highs, last 1193.75 (against 1197.11 in the first part of trade).

- Spot USD/KRW found early selling interest above 1475, last near 1468.5. Given the broader risk concerns, along with sharp global led tech equity losses, we suspect dips in the pair will be supported, with 1455/56 the 20 and 50-day EMA support area. USD/TWD spot is around 31.65/70, just on recent highs. A clean break higher is likely to see the 32.00 region targeted.

ASIA FX: USD/IDR Eyes +16900, RBI On Hold, USD/PHP Breaks Lower

USD/IDR was last near 16880 just off session highs. Upside focus remains on the 16900 area. The bad news keeps coming after Moody's downgraded the ratings outlook for the country. Local equities remain under pressures, last -2.8%. BI intervention seems the main factor that can stop a sharp move through 16900.

- As expected, the RBI held rates steady. It was a somewhat hawkish hold, as the central bank nudged up its inflation forecasts, while also maintaining an optimistic growth outlook. USD/INR is down slightly, last around 90.20/25. Earlier lows this week were at 90.05. Indian bond yields are higher, as the market may have also been looking for the RBI to do more on liquidity side.

- USD/PHP has continued its recent correction lower, last 58.55/60, which is under trendline support back to May of this year and near the 100-day EMA. Lack of exposure to global risk off moves and the rise in inflation pressures (printed yesterday) is aided, as markets don't expect much more easing from BSP (although a Feb cut is still likely in our view).

- USD/THB around 31.70 currently, off earlier highs near 31.89. There looks to be some near term resistance around this level, which also coincides with the 100-day EMA resistance point. The rebound in gold has likely helped THB, while local equities have also outperformed. The weekend focus will be on the election outcome.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 06/02/2026 | 0645/0745 | ECB Cipollone on Digital Euro at Association of Cyprus Banks | ||

| 06/02/2026 | 0700/0800 | ** | Trade Balance | |

| 06/02/2026 | 0700/0800 | ** | Industrial Production | |

| 06/02/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 06/02/2026 | 0700/0800 | *** | Flash Inflation Report | |

| 06/02/2026 | 0745/0845 | * | Foreign Trade | |

| 06/02/2026 | 0800/0900 | ** | Industrial Production | |

| 06/02/2026 | 0800/0900 | ** | Unemployment | |

| 06/02/2026 | 1200/1200 | BOE Market Participants Survey | ||

| 06/02/2026 | 1215/1215 | BOE Pill at National MPC Agency Briefing | ||

| 06/02/2026 | - | BOE MPG Agenda Published | ||

| 06/02/2026 | 1330/0830 | *** | Labour Force Survey | |

| 06/02/2026 | 1330/0830 | *** | Labour Force Survey | |

| 06/02/2026 | 1500/1000 | * | Ivey PMI | |

| 06/02/2026 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 06/02/2026 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 06/02/2026 | 1700/1200 | Fed Vice Chair Philip Jefferson | ||

| 06/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/02/2026 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 06/02/2026 | 2000/1500 | * | Consumer Credit |