OIL: Oil Posting Weekly Losses as US Iran Meeting Approaches

- Despite modest gains Friday during the Asia trading day, oil is currently down over .1-5% for the week following significant falls earlier.

- WTI has traded in a US$62.31 - $63.85 range today, currently near session highs at $63.72 bbl, for gains of +0.66%. Price action however is modest as traders look ahead to Friday in the Middle East where US and Iran representatives meet.

- It is unlikely that any ground breaking 'deal' will be announced given the pushback from Iran leading in recent weeks. Trump did suggest Iran is already 'negotiating' leading to earlier declines. However news of the Saudi cut in prices for Asia buyers being less than expected, was interpreted as a positive signal for oil demand as it pushed back in afternoon trade.

- Brent is up +0.50% today but lower by almost -4% for the week. Brent opened lower in Asia reaching $66.87, rallying up to $68.12 before settling to $67.93. $68 seems a key resistance here for Brent and would likely require negative headlines from the meeting Friday to see it push beyond and hold above that level.

- Shorter term momentum indicators are trending more neutral at present, suggesting that the US Iran risks are more balanced for now, but negative headlines seem likely to provide more of an impact. The more neutral momentum indicators suggests trader's outright views remain mixed at best with likely limited expectations for any immediate break throughs.

- Shell reported a slump in fourth-quarter profits, citing weaker crude prices and poor oil trading performance, which weighed on broader energy market sentiment as it announced a pause in investment in Kazakhstan, amidst a legal dispute with the country which could cost the company billions.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Twist-Steepener Ahead Of Tomorrow's 30Y Supply

JGB futures are stronger, +16 compared to settlement levels, but off session bests.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- (Bloomberg) “JGB traders continue to be aggressive sellers of bonds in the mid-section of the curve when the BOJ comes calling at Rinban operations. The selling ratio rose today to 3.11 in the three-to-five year sector, up from 2.37 at the previous round.”

- Nevertheless, the cash JGB curve has twist-steepened across benchmarks, with yields 1.3–1.7bps lower in the 3–5-year sector and around 2.5bps higher at the 40-year point, ahead of tomorrow’s long-end supply.

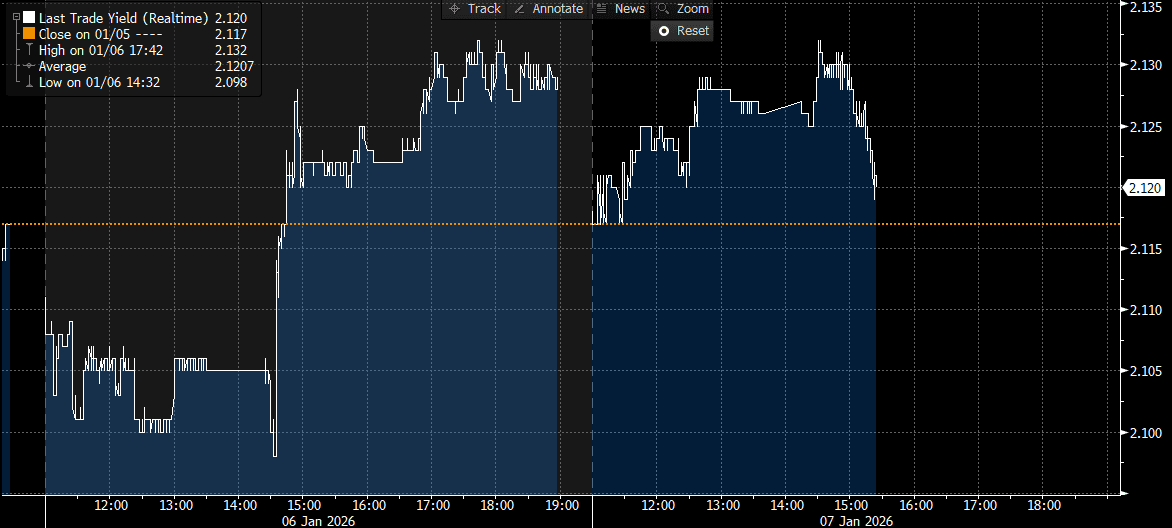

- The benchmark 10-year yield is 0.9bp lower at 2.120% versus the cycle high of 2.134% (see chart).

- The 10-year JGB auction yesterday delivered weakish results, with the low price failing to meet expectations at 100.00, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3037x from 3.5913x.

- Swap rates are 1bp lower to 1bp higher, with a steeper curve.

- Tomorrow, the local calendar will see Cash Earnings, Tokyo Avg Office Vacancies, Consumer Confidence and Weekly International Investment Flows alongside 30-year supply.

Source: Bloomberg Finance LP

AUDNZD: Fresh Highs, Eyeing 1.18-1.20, RBA Expectations/Higher Commodities Help

The earlier A$ pullback was very modest and well supported. It came after the slight downside surprise in headline CPI for Nov. AU rates markets were softer in yield terms initially, but supported on dips, particularly the front end. Indeed, RBA-dated OIS is slightly firmer versus pre-CPI levels. The pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 41% for February to 121% by June and 189% by December 2026. Outside of yield support, another source of A$ gains is rising commodity prices.

- The AUD/NZD cross has reached fresh cycle highs, last tracking near 1.1690, which is fresh highs back to 2013. We are in overbought territory per RSI (14), but dips remain supported. Upside focus is likely to rest for a move into the 1.18-1.20 region.

- It might take a move back under 1.1480/85, which marks the 50-day EMA support support, which held in Q4 last year, to shift bullish sentiment.

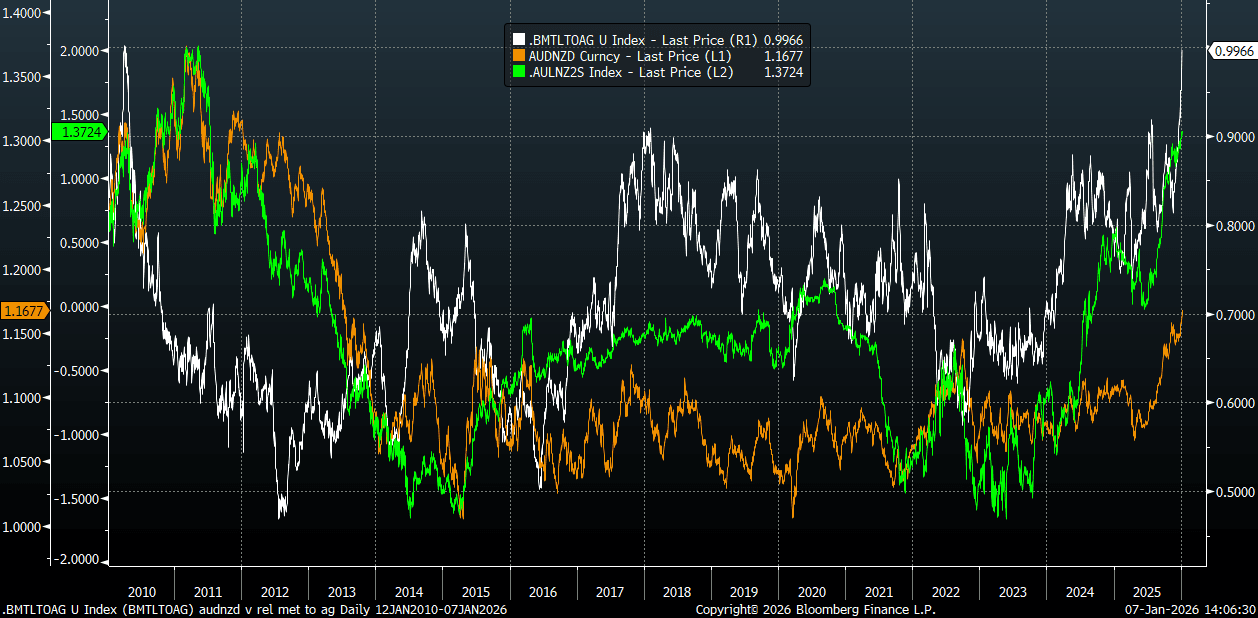

- The chart below plots the AUD/NZD spot cross versus the AU-NZ 2yr swap spread (the green line0 last around +137bps and fresh multi year highs. The other line is a metals to agricultural price index ratio (a rough proxy for relative terms of trade between the two economies). Even with the overnight rise in whole milk prices, metals gains continue to outpace from a trend standpoint.

Fig 1: AUD/NZD Versus Metal To Agricultural Commodity Prices & AU-NZ 2yr Swap Spread

Source: Bloomberg Finance L.P./MNI

CHINA: Bond Futures Trade Sideways in Wednesday Price Action

- China's bond futures are doing very little today as the daily OMO withdrew liquidity again, taking the YTD total near CNY1.7tn.

- The 10-Yr is unchanged at 107.7, below all major moving averages. The topside resistance is at the 20-day EMA of 107.95.

- The 2-Yr is at 102.366, unchanged for the day and remains below all major moving averages. Topside resistance is at the 50-day EMA of 102.42

- The 2-YR CGB is at 1.39% today and the 10-Yr at 1.88%.

- There is some significant issuance to note Wednesday with a CNY175bn 2027 bond auction.