ASIA FX: USD/IDR Eyes +16900, RBI On Hold, USD/PHP Breaks Lower

USD/IDR was last near 16880 just off session highs. Upside focus remains on the 16900 area. The bad news keeps coming after Moody's downgraded the ratings outlook for the country. Local equities remain under pressures, last -2.8%. BI intervention seems the main factor that can stop a sharp move through 16900.

- As expected, the RBI held rates steady. It was a somewhat hawkish hold, as the central bank nudged up its inflation forecasts, while also maintaining an optimistic growth outlook. USD/INR is down slightly, last around 90.20/25. Earlier lows this week were at 90.05. Indian bond yields are higher, as the market may have also been looking for the RBI to do more on liquidity side.

- USD/PHP has continued its recent correction lower, last 58.55/60, which is under trendline support back to May of this year and near the 100-day EMA. Lack of exposure to global risk off moves and the rise in inflation pressures (printed yesterday) is aided, as markets don't expect much more easing from BSP (although a Feb cut is still likely in our view).

- USD/THB around 31.70 currently, off earlier highs near 31.89. There looks to be some near term resistance around this level, which also coincides with the 100-day EMA resistance point. The rebound in gold has likely helped THB, while local equities have also outperformed. The weekend focus will be on the election outcome.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

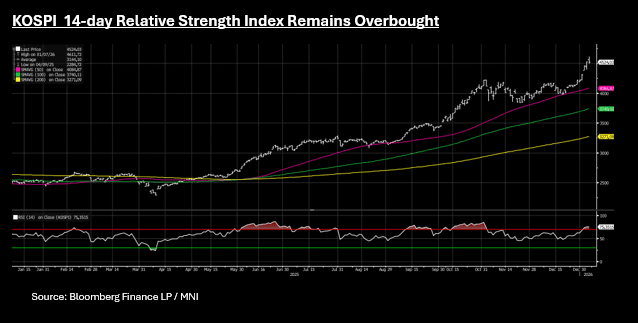

ASIA STOCKS: Mixed Day for Stocks, KOSPI Remains Overbought on RSI

A mixed day across Asia with profit taking driving key markets as they back away from near term highs. A mixed day for key AI / Tech stocks with Taiwan's TSMC - 1.7%, Korea's AI /Tech names have had a strong rally with Samsung Electronics +1.6%, +3.3%, Whilst Japan's Softbank fell -1.5%. The weakness in oil has had a limited impacted with some energy linked companies like Petronas in Malaysia up 1% today. There is growing recognition from markets of the stretched valuations for the tech sector, a risk that will continue in the background for now whilst the euphoria continues.

- The NIKKEI has had its first fall of the year, down -1.2% today whilst remaining up over 3% in the first three trading days, reaching a new high of 52,518 yesterday.

- The KOSPI is flat today despite the bounce back from the AI Tech names despite growing concerns over their valuations. The KOSPI maintains its position of overbought on the 14-day relative strength index, likely feeding into the the lacklustre performance today.

- China's bourses are mixed today with the Hang Seng following the lead from Japan and Korea with falls of -1.2%, dragging the CSI 300 down -0.22% with it. Onshore bourses have fared better with Shanghai up +0.15% and Shenzhen +0.21%

- SE Asia's major bourses were stable with SE Thai and FTSE Malay flat and the JCI in Indonesia up by a modest +0.14%

- India's NIFTY 50 continues to moderate down -.20% at early Wednesday for its third day of falls. Having reached new highs Friday of 26,328 it has fallen -0.60% in subsequent trading days.

OIL: Crude Continues Selling Off As Venezuelan Oil To Flow To US

Oil has faced further downward pressure today after US data showed large product inventory builds and President Trump announced Venezuela will ship “between 30 and 50 MILLION barrels of High Quality Sanctioned Oil” to the US. Both events added to ongoing concerns over a global supply glut pushing prices down further after Tuesday’s 2% decline. In addition, the discussion of security guarantees Tuesday may have brought a Ukraine deal closer.

- WTI is down 1.6% today to $56.24 after falling to $55.76 following Trump’s Truth Social post but holding above initial support at $54.89. Brent is 1.1% lower at $60.02 with the break below $60 short-lived. While technicals signal a dominant downtrend, it is holding above support at $58.53.

- Chevron & Quantum are set to bid for Lukoil’s assets after US imposed sanctions on Russia’s oil majors, according to the FT.

- Without a timeframe it is difficult to understand how Venezuela will be able to send 30-50mn barrels of oil to the US. The IEA reported that it produced only 860 kbd in November 2025 down from around 1mbd earlier.

- It is reported that Chevron, who still has operations in Venezuela, has sent 11 tankers to begin transporting oil to the US. Gulf refineries are geared to refine heavy, sour crude of the type that Venezuela produces.

- Bloomberg reported that there was a 2.8mn barrel US oil inventory drawdown last week, according to people familiar with the API data. Gasoline inventories rose 4.4mn and distillate 4.9mn. The official EIA data is out Wednesday.

- Later on Wednesday US December ADP employment, November JOLTS job openings, December ISM services and final October orders print. The Fed’s Bowman speaks on banking regulation. In Europe, preliminary December euro area CPI and November German unemployment & retail sales are released.

FOREX: A$ Gains The Standout, AUD/NZD At Fresh Cycle Highs, Steady Elsewhere

Outside of AUD gains, the price action in the G10 has been very muted so far today. The USD BBDXY index sits little changed near 1205.10 in latest dealings. The A$ sits up 0.35% to 0.6760/65, fresh highs back to 2024. We saw a brief dip to 0.6717 post a slightly softer Nov CPI read, but this was well supported. We are just above the Oct 11 2024 high of 0.6759, with the 0.6800 region now likely to come into focus. AU rates, particularly at the front end, were also supported from a yield stand point. RBA tightening expectations for 2026 sit slightly firmer versus pre CPI levels. Outside of rate expectations, the metals commodity backdrop is also aiding the AUD, with iron ore gains notable today.

- Shifts elsewhere in the G10 space are less than 0.1% at this stage. NZD/USD is little changed, last 0.5780/85, while USD/JPY is just under 156.60. EUR/USD is up a touch but still under 1.1700 at this stage.

- The AUD/NZD cross is trending towards 1.1700, fresh highs back to 2013. AUD/JPY is near 105.90, fresh highs back to mid 2024.

- We are seeing softer gold and silver trends so far today, but the BBG metals spot sub index is up 16% since late Nov lows. Iron ore is above $108.50/ton per the active SGX contract.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.