AUSSIE BONDS: Richer But AU-US 10Y Diff Back At Cycle High

ACGBs (YM +3.5 & XM +3.0) are stronger but off session bests as risk assets rebounded from yesterday’s carnage. Silver and Gold are 1% and 3% stronger, NDX and SPX futures have pared early losses while Bitcoin is up ~2%.

- In her testimony before the Australian Parliament this morning, RBA Governor Bullock stated the RBA is watching inflation risks, particularly in terms of how much of the recent uptick is temporary versus persistent, and in turn capacity constraints, which will be the key watch points around further tightening.

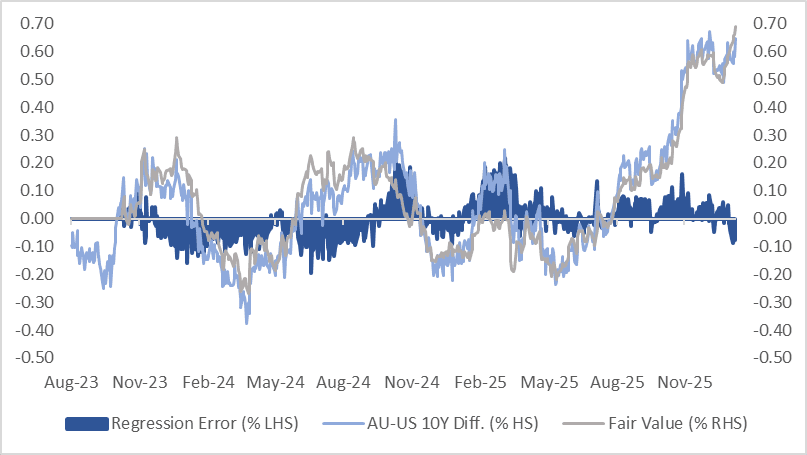

- While the cash ACGBs are 3bps richer today, the AU-US 10-year yield differential has returned to its cycle high of +65bps.

- Since early December, price action has effectively consolidated the differential’s 50-65bps trading range following the breakout above the ±30bps range that had prevailed since November 2022. This widening has coincided with a steady lift in market-implied expectations for the RBA cash rate.

- The bills strip has bull-flattened, with pricing +1 to +6 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 15% for March to 94% by June and 149% by December 2026.

- On Monday, the local calendar will see Household Spending data.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Bull-Flattener But Swap Curve Remains At Highs

NZGBs closed showing a bull-flattening, with benchmark yields flat to 2bps.

- NZ-US and NZ-AU 10-year yield closed unchanged at +33bps and -28bps.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

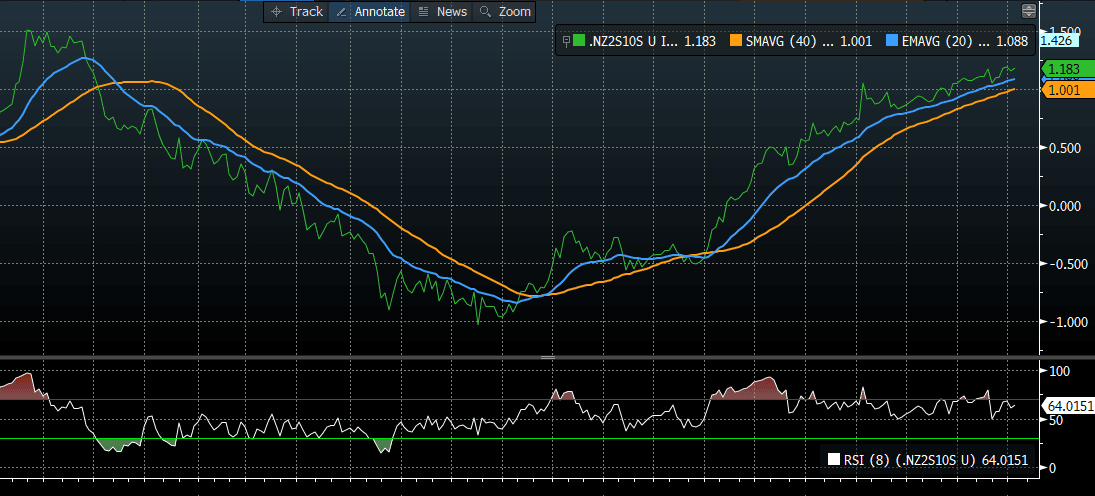

- NZ swap rates are flat to 3bps, with a flatter curve. Nevertheless, the 2s10s curve remains near cycle highs, the steepest since 2021.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

- The local data calendar is very light this week. Next week we get Nov filled jobs, along with food prices as well.

Bloomberg Finance LP

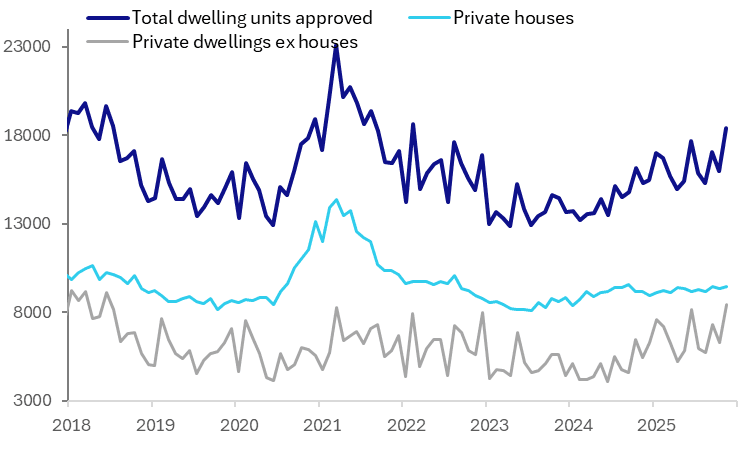

AUSTRALIA DATA: Multi-Dwellings Jump But House Approvals Remain Soft

The number of building approvals in November jumped 15.2% m/m after falling 6.1% m/m driven by the volatile multi-dwelling component. Private houses rose 1.3% m/m after falling 1.3% in October but were still up only 3.2% y/y. They appear to be recovering from the Q2/Q3 2025 dip. Momentum is picking up across both houses and apartments but the former is still soft.

- Strong demand and supply shortages have driven home prices higher. Approvals have struggled to improve as needed. A gradual uptrend in the total has been due to the non-house component but it remains 20% below the 2021 peak.

- Queensland and Victoria drove the jump in multi-dwelling approvals, which were their highest since June 2018 and up 55.3% y/y.

- The level of house approvals has been moving sideways since Q3 2024. The November rise was due to NSW and Queensland while they fell in SA.

Australia number of dwellings approved

Source: MNI - Market News/ABS

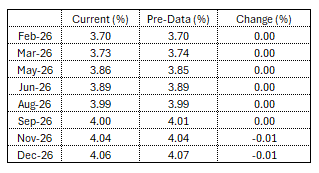

STIR: RBA-Dated OIS Little Changed Versus Pre-CPI Levels

RBA-dated OIS is little changed versus pre-CPI levels. The pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 38% for February to 116% by June and 184% by December 2026.

Figure 1: RBA-Dated OIS – Current

Source: Bloomberg Finance LP / MNI