INDIA: RBI on Hold, Governor Calls it a Wait and See Approach

- As we expected, the RBI held rates steady today at 5.25% with unanimous vote, maintaining their focus on prior policy adjustments. The MPC noted that the transmission of previous rate cuts to bank lending rates is still in progress, and further immediate easing might be premature until the full effects of the 125 bps cumulative reduction are realized.

- The RBI raised its GDP growth forecast for FY26 to 7.4% (up from 7.3%), noting that domestic momentum remains resilient and is supported by a growth-focused Union Budget and upside potential from the US trade deal

- Headline inflation remains benign (projected at 2.1% for FY26), the RBI revised its FY27 projections slightly upward to 4% for Q1 and 4.2% for Q2, necessitating a cautious stance to ensure price stability remains within the target band.

- The central bank maintained its immediate focus toward active liquidity management rather than further rate actions, aiming to address tight banking system liquidity and stabilize the yield curve

- IGB 10-Yr is up on the day, climbing +4.5bps to 6.696% whilst the NIFTY 50 is down -0.45% in early trade, following regional leads.

- We expect further focus on liquidity to translate to more injections in the coming months via OMO. Swaps have little priced in the near terms but have the potential to re-price in the coming weeks as volatility declines.

- RBI next meeting details are yet to be released.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: A$ Gains The Standout, AUD/NZD At Fresh Cycle Highs, Steady Elsewhere

Outside of AUD gains, the price action in the G10 has been very muted so far today. The USD BBDXY index sits little changed near 1205.10 in latest dealings. The A$ sits up 0.35% to 0.6760/65, fresh highs back to 2024. We saw a brief dip to 0.6717 post a slightly softer Nov CPI read, but this was well supported. We are just above the Oct 11 2024 high of 0.6759, with the 0.6800 region now likely to come into focus. AU rates, particularly at the front end, were also supported from a yield stand point. RBA tightening expectations for 2026 sit slightly firmer versus pre CPI levels. Outside of rate expectations, the metals commodity backdrop is also aiding the AUD, with iron ore gains notable today.

- Shifts elsewhere in the G10 space are less than 0.1% at this stage. NZD/USD is little changed, last 0.5780/85, while USD/JPY is just under 156.60. EUR/USD is up a touch but still under 1.1700 at this stage.

- The AUD/NZD cross is trending towards 1.1700, fresh highs back to 2013. AUD/JPY is near 105.90, fresh highs back to mid 2024.

- We are seeing softer gold and silver trends so far today, but the BBG metals spot sub index is up 16% since late Nov lows. Iron ore is above $108.50/ton per the active SGX contract.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

PRECIOUS METALS: Gold & Silver Lower Ahead Of The Week’s US Jobs Data

After rallying on Tuesday as geopolitical risks drove safe haven flows, gold & silver are lower in Wednesday’s APAC session. Precious metals appear to be steadying ahead of this week’s US jobs data, which finishes with payrolls on Friday and is likely to influence Fed easing expectations. Also the discussion of security guarantees Tuesday may have brought a Ukraine deal closer. US yields are little changed while the US dollar is down slightly.

- Gold is down 0.6% to $4465.5/oz after falling to $4459.92. It approached the 26 December record high at $4549.92 on Tuesday, which is the bull trigger. Any sell off is still corrective for now.

- Silver is 1.9% lower at $79.78/oz, close to the intraday low. It rose to $82.754 early in trading below the 28 December record at $84.0075, which is also the bull trigger. It remains in an uptrend but is also in overbought territory.

- Precious metals will be watching this week’s US labour market data closely given OIS pricing seems unsure if there will be another Fed rate cut in Q1 with a full 25bp not priced in before June.

- Later on Wednesday US December ADP employment prints and is forecast to rise 50k after falling 32k in November. There are also November JOLTS job openings, December ISM services and final October orders. The Fed’s Bowman speaks on banking regulation.

- Equities are mixed with the S&P e-mini is slightly lower, the CSI is flat and Hang Seng down 1.0%. Oil continues to sell off with WTI -1.5% to $56.26/bbl. Copper is down 1.1%.

JGBS: Twist-Steepener Ahead Of Tomorrow's 30Y Supply

JGB futures are stronger, +16 compared to settlement levels, but off session bests.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- (Bloomberg) “JGB traders continue to be aggressive sellers of bonds in the mid-section of the curve when the BOJ comes calling at Rinban operations. The selling ratio rose today to 3.11 in the three-to-five year sector, up from 2.37 at the previous round.”

- Nevertheless, the cash JGB curve has twist-steepened across benchmarks, with yields 1.3–1.7bps lower in the 3–5-year sector and around 2.5bps higher at the 40-year point, ahead of tomorrow’s long-end supply.

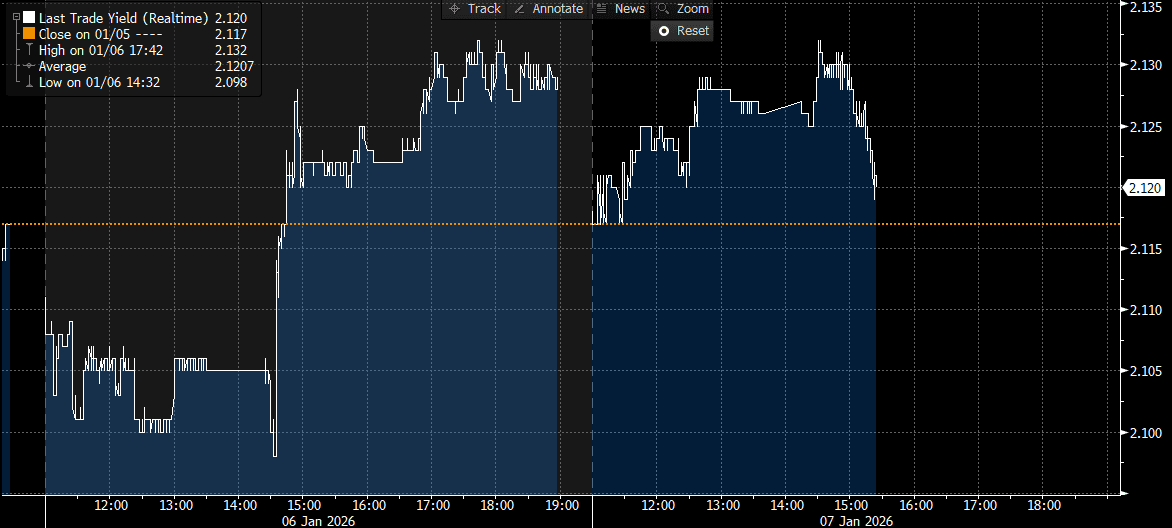

- The benchmark 10-year yield is 0.9bp lower at 2.120% versus the cycle high of 2.134% (see chart).

- The 10-year JGB auction yesterday delivered weakish results, with the low price failing to meet expectations at 100.00, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3037x from 3.5913x.

- Swap rates are 1bp lower to 1bp higher, with a steeper curve.

- Tomorrow, the local calendar will see Cash Earnings, Tokyo Avg Office Vacancies, Consumer Confidence and Weekly International Investment Flows alongside 30-year supply.

Source: Bloomberg Finance LP