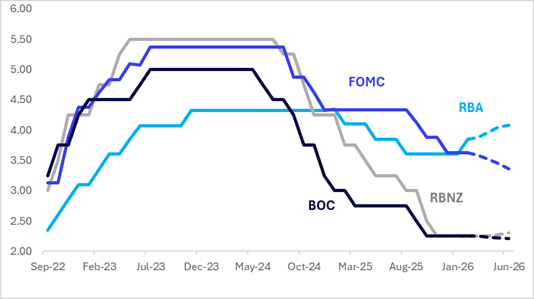

STIR: AUS Is A Hawkish Outlier In The $-Bloc

Interest-rate expectations across the $-bloc over the past three weeks, looking out to June 2026, have softened slightly, with the notable exception of Australia, where expectations firmed by 27bps. Elsewhere, US and Canada pricing moved 7bps and 3bp lower, respectively, while New Zealand nudged 2bps higher.

- The key event of the past week was the RBA’s decision to hike interest rates by 25bps to 3.85% on Tuesday.

- The RBA raised the cash rate to 3.85%, as expected by the sell-side consensus and which was largely priced by the market (around 75% priced in per OIS markets prior to the decision). The decision was unanimous by the board. The risks appear skewed towards further action to ensure that inflation moves sustainably back into the target band of 2-3%. (see MNI RBA Review here).

- RBA Governor Bullock was before the Australian Parliament this morning and stated that the RBA is watching inflation risks, particularly in terms of how much of the recent uptick is temporary versus persistent, and in turn capacity constraints, which will be the key watch points around further tightening.

- The next major regional policy event is the RBNZ meetings on 18 February. No tightening is priced for February, while December 2026 assigns 43bps.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.36%, -26bps; Canada (BOC): 2.21%,-4bp; Australia (RBA): 4.08%, +23bps; and New Zealand (RBNZ): 2.33%, +8bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Twist-Steepener On A Data-Light Session

In Tokyo morning trade, JGB futures are stronger, +9 compared to settlement levels, but off session bests.

- (MT Newswires) Japan's service sector growth momentum slowed in December 2025, with the Services PMI falling to 51.6 from 53.2 in November, indicating the softest expansion in business activity since May 2025, according to S&P Global's report.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

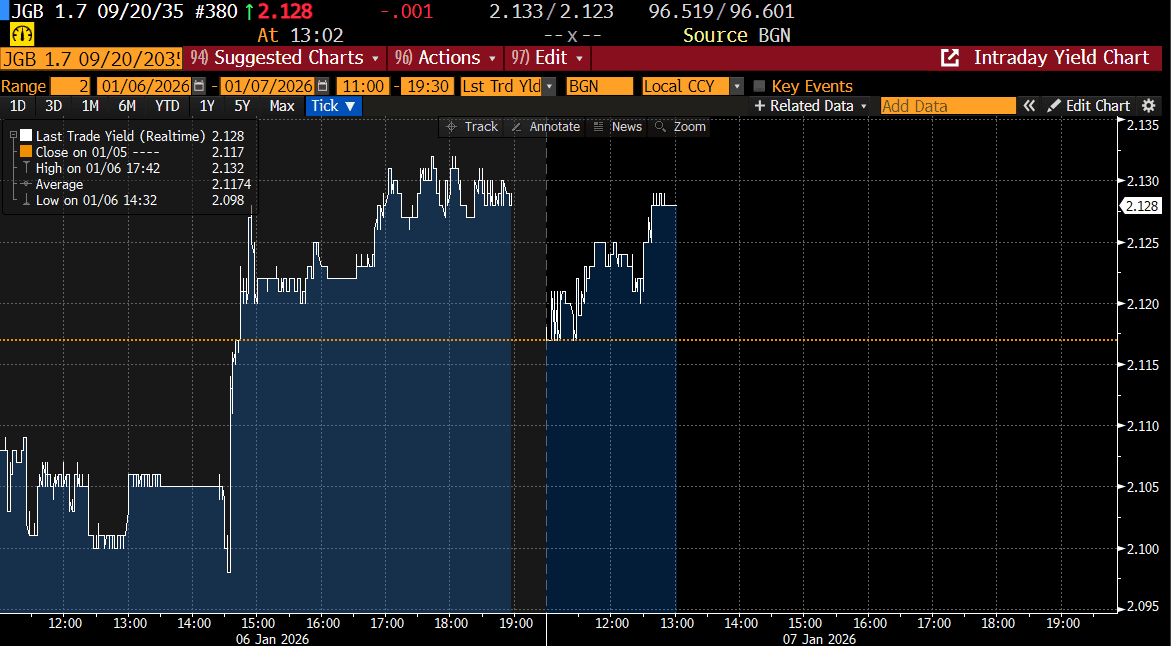

- Cash JGBs have twist-steepened across benchmarks, with yields 1.5bps lower (4-year) to 2.8bps higher (40-year). The benchmark 10-year yield is 0.1bp lower at 2.128% versus the cycle high of 2.134% (see chart).

- ICYMI, the 10-year JGB auction yesterday delivered weakish results, with the low price failing to meet expectations at 100.00, according to the Bloomberg dealer poll. Moreover, the cover ratio decreased to 3.3037x from 3.5913x and the tail lengthened to 0.05 from 0.04.

- Swap rates are 1bp lower to 2.5bps higher, with a steeper curve.

Source: Bloomberg Finance LP

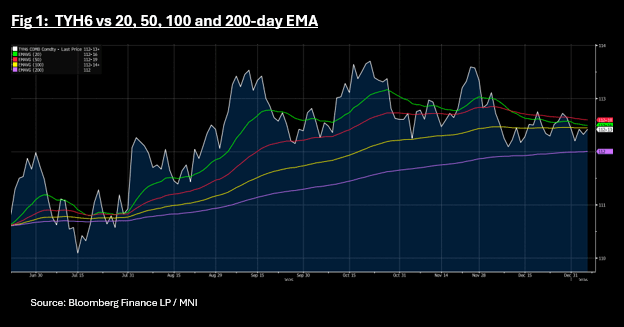

US TSYS: TYH6 Nears Key Tech Level

US treasury futures are firmer today, with all maturities higher in the Asia trading morning. The US 10-Yr future is up +03+ to 112-13 in quiet start, with volumes moderate. The move higher leaves TYH6 near to the upside resistance from the 100-day EMA of 112-14+. Downside resistance is in the form of the 200-day EMA at 112.

Cash is flat at the front end with 5-Yr and longer lower in yields. The long end is outperforming.

- The 2-Yr is flat at 3.465%

- The 5-Yr is flat at 3.712%

- The 10-Yr is lower by -1bps at 4.165%

- The 30-yr is lower by -1.1bps at 4.855%

Taking into account comments from several FOMC participants since the December Dot Plot projections were released, MNI's compilation of end-2026 funds rates by member is below (A digest of Fed commentary after the December meeting through the FOMC Minutes is here: https://media.marketnews.com/Fed_Minutes_Preview_Dec2025_bf656ac185.pdf

Three "insurance" interest rate cuts last year have left monetary policy within the range of the Federal Reserve's estimates of neutral and further moves will carefully balance both labor market and inflation goals, Richmond Fed President Tom Barkin said Tuesday.

Tonight markets will focus on the US$69bn 17-week bill auction and the ADP Employment change, ISM Services and JOLT Job openings, Factor Orders and Durable Goods orders. For the ADP, forecasts are for +50k in December, from -32k prior. Other key data out will be the ISM Services Index which is forecast to moderate to 52.2 from 52.6 in November. JOLT job openings is forecast at 7648k for December, from 7670 in November. Factory and Durable goods orders are both forecast to contract.

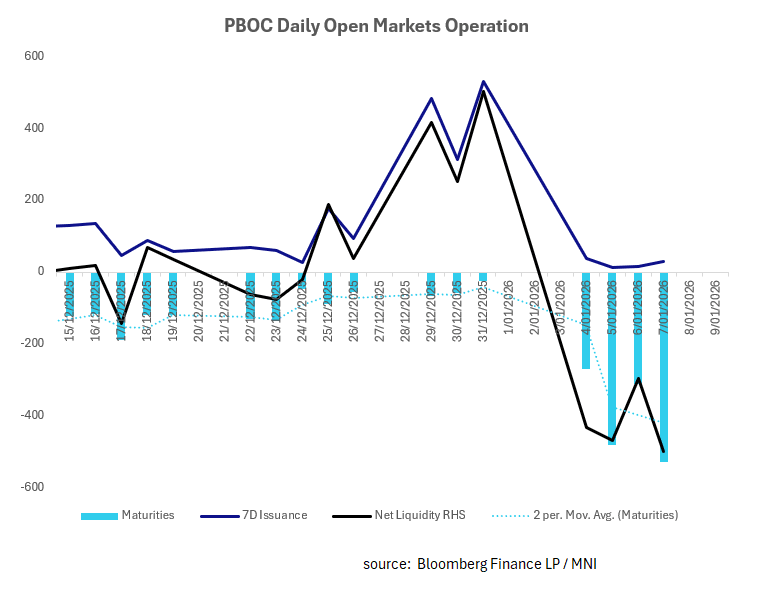

CHINA: Central Bank Withdraws CNY500.2bn via OMO

The PBOC's continues to with draw liquidity, taking the year to date withdrawal to almost CNY1.7tn in just four days operations with early signs that there may be some upward pressure on repo rates.

- The PBOC issued CNY28.6bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY528.8bn.

- Net liquidity withdrawal CNY500.2bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.43%, from prior close of 1.43%.

- The China overnight interbank repo rate is at 1.27%, from the prior close of 1.40%.

- The China 7-day interbank repo rate is at 1.44%, from the prior close of 1.48%.