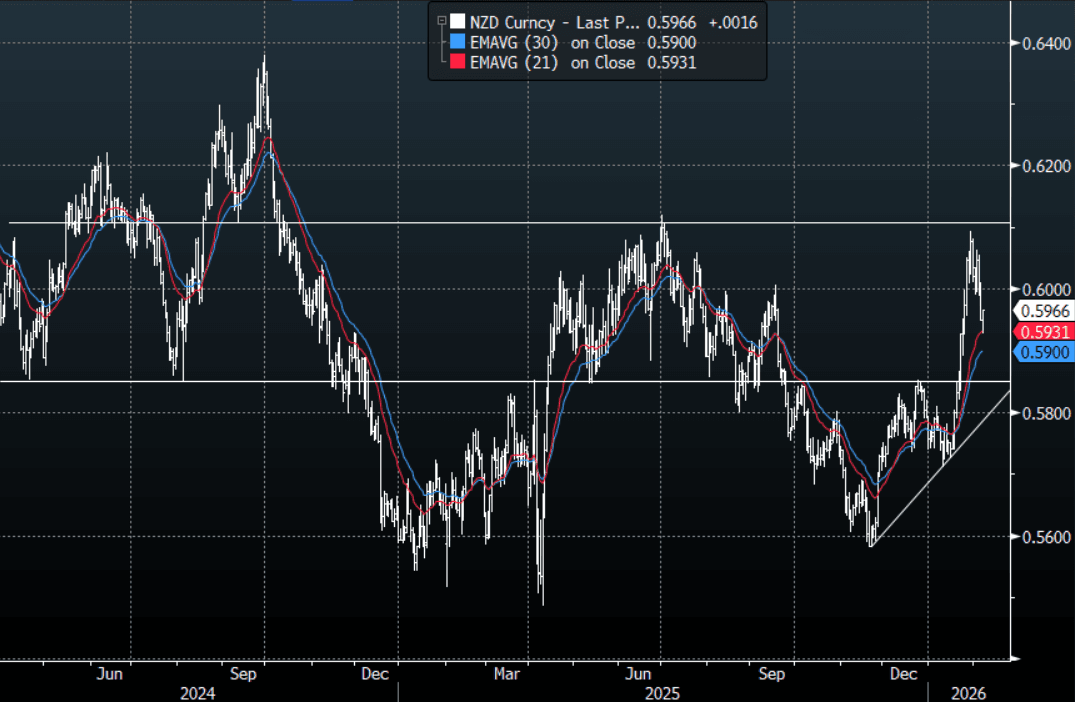

NZD: NZD/USD - Finds Buyers Toward 0.5900 As Risk Pares Back Early Losses

The NZD/USD had a range today of 0.5928-0.5967 in the Asia-Pac session, it is currently trading around 0.5966, +0.30%. The NZD got hit hard early as the Asia open gapped lower following on from the rout overnight in risk, as the market settled and pared back some of its early losses the NZD regained those losses and moved back into positive territory. The NZD has come under pressure as the risk-off back-drop has started to broaden with Crypto deciding Metals could not have all the fun and collapsed over 12%. US Stocks are again under pressure as Tech begins to falter, this time the broader market is not balancing out the move. On the day, the NZD is trading heavy back under 0.6000, and how risk trades going into the weekend will determine if we have another look toward the 0.5850-0.5900 area. This ugly rejection above 0.6000 looks to have put the test of 0.6100 on hold for now.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 60 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA STOCKS: Tech/Govt Initiatives In Focus, Attractive Valuations Help Gains

- Artificial Intelligence (AI): The AI sector, particularly AI chips, has been a primary driver of the recent market rally, benefiting from investor optimism and policy support. Though the AI / tech sector has somewhat lagged behind that of Korean and Japanese names, an opportunity some asset allocators are focusing on

- Domestic Semiconductor Production: A central pillar of Beijing's push for tech self-reliance, with directive-driven demand for Chinese-made AI chips in state data centers.

- New Energy Technologies: This sector is expected to benefit from continued government policy support and the country's pivot toward innovation-led growth.

- Innovative Drugs: The innovative pharmaceuticals industry is another area identified for potential growth within the new market phase.

AUSSIE BONDS: Slightly Richer Post-CPI, Mixed On The Day

ACGBs (YM -1.0 & XM +2.0) are 2-3bps stronger versus pre-CPI levels, but well off post-date highs.

- November trimmed mean CPI inflation moderated 0.1pp to 3.2% y/y in line with consensus, while headline fell more than expected at 3.4% after 3.8%. The complete monthly series is new with little track record and so the RBA will focus on the quarterly data for now with Q4 printing on 28 January.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- Cash ACGBs are flat to 2bps richer with the AU-US 10-year yield differential at +59bps.

- The bills strip is -2 to -4 across contracts.

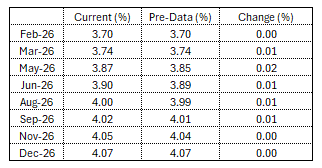

- RBA-dated OIS is slightly firmer versus pre-CPI levels. The pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 41% for February to 121% by June and 189% by December 2026.

- TCV A$ Nov 2037 Benchmark Bond Tap, 10Y EFP+88-90bp Area

- Tomorrow, the local calendar sees Trade balance data for November.

Figure 1: RBA-Dated OIS – Current

Source: Bloomberg Finance LP / MNI

BONDS: NZGBS: Bull-Flattener But Swap Curve Remains At Highs

NZGBs closed showing a bull-flattening, with benchmark yields flat to 2bps.

- NZ-US and NZ-AU 10-year yield closed unchanged at +33bps and -28bps.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

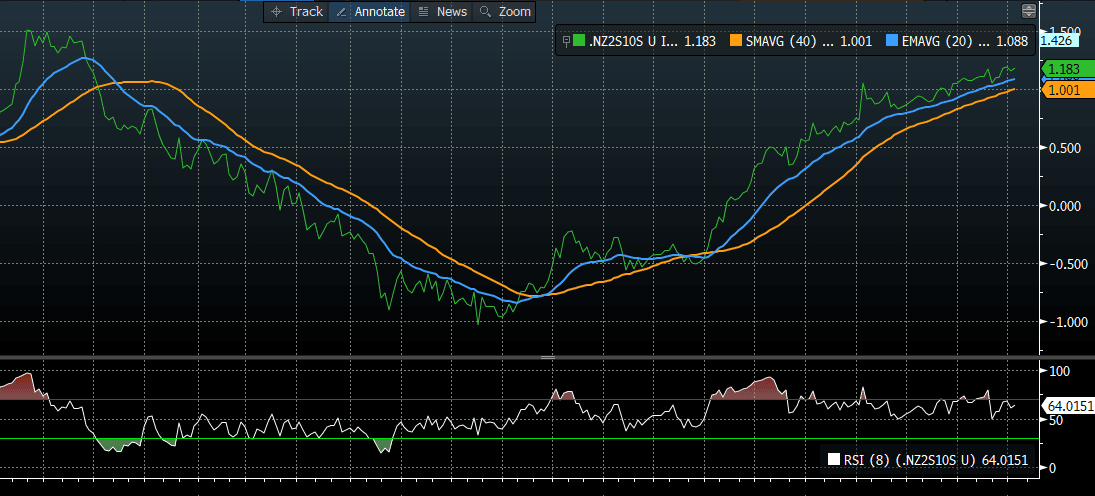

- NZ swap rates are flat to 3bps, with a flatter curve. Nevertheless, the 2s10s curve remains near cycle highs, the steepest since 2021.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

- The local data calendar is very light this week. Next week we get Nov filled jobs, along with food prices as well.

Bloomberg Finance LP