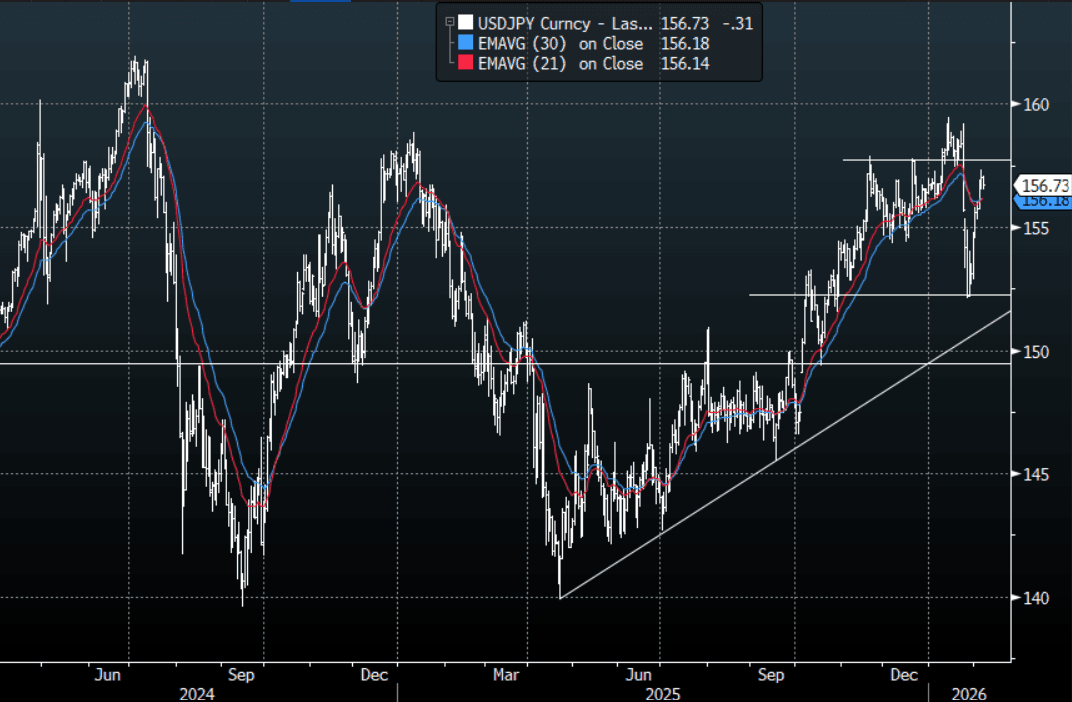

JPY: USD/JPY - Treading Water Below 157.00 Going Into The Weekend

The USD/JPY range today has been 156.52 - 157.10 in the Asia-Pac session, it is currently trading around 156.70, -0.20%. USD/JPY looks to be consolidating just below 157.00 as we head into the weekend's elections. The large move lower was more down to overextended positioning than fundamentals and as we head toward this weekend's election all the reasons for the Yen short have come back to the fore. This should keep USD/JPY well supported on dips now as the market looks toward the 160.00 area once again. It stalled above 157.00 overnight but I suspect a dip back toward the first support around 155.75-156.25 should find buyers first up.

- MNI: BOJ's Masu Sees Timely Hikes To Keep Inflation Below 2%. Bank of Japan board member Kazuyuki Masu said on Friday that the BOJ needs to raise the policy rate in a timely manner to ensure underlying inflation remains below 2%, but he did not give a timeline.

- “Donald Trump said he would meet with Sanae Takaichi at the White House on March 19. He also endorsed the PM’s coalition in Japanese elections set for Sunday.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 156.00($991m), 157.00($808m). Upcoming Close Strikes : 156.50($938m Feb 11), 157.00($754m Feb 10), 158.25($773m Feb 11) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 130 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

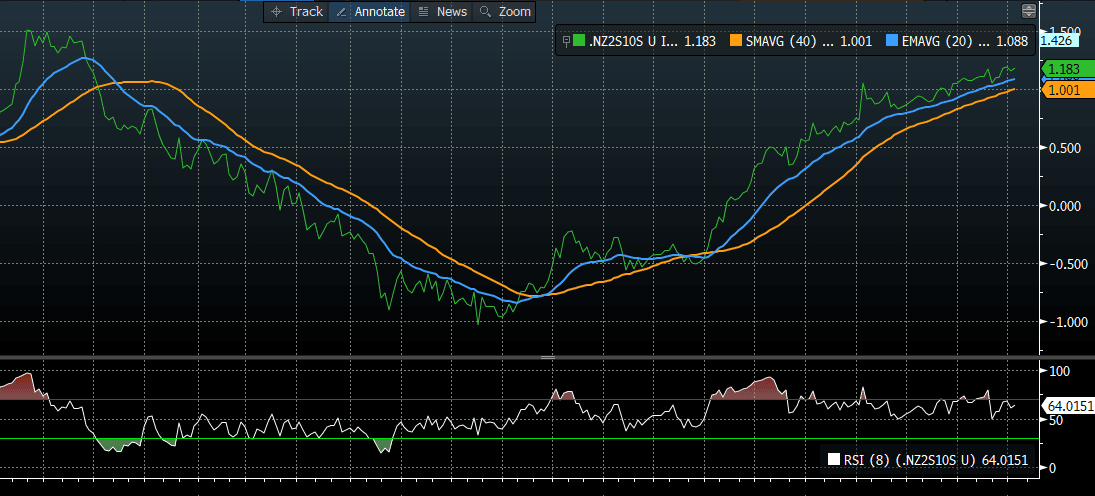

BONDS: NZGBS: Bull-Flattener But Swap Curve Remains At Highs

NZGBs closed showing a bull-flattening, with benchmark yields flat to 2bps.

- NZ-US and NZ-AU 10-year yield closed unchanged at +33bps and -28bps.

- Cash US tsys are flat to 1bp richer, with a flattening bias, in today's Asia-Pac session. US ADP private employment & JOLTS data today, NFP Friday.

- NZ swap rates are flat to 3bps, with a flatter curve. Nevertheless, the 2s10s curve remains near cycle highs, the steepest since 2021.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

- The local data calendar is very light this week. Next week we get Nov filled jobs, along with food prices as well.

Bloomberg Finance LP

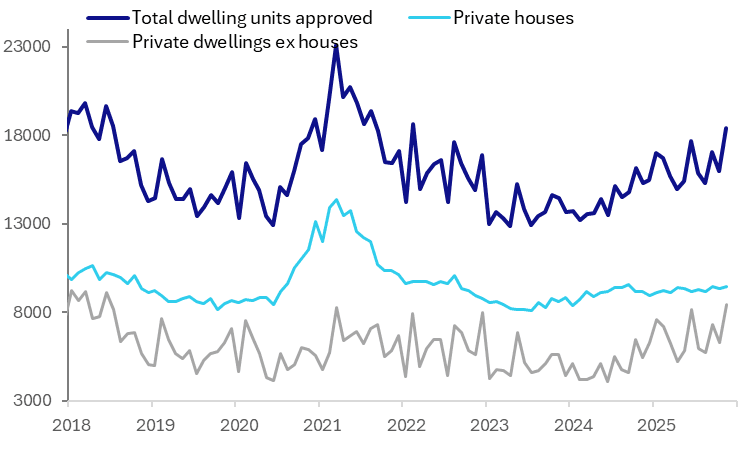

AUSTRALIA DATA: Multi-Dwellings Jump But House Approvals Remain Soft

The number of building approvals in November jumped 15.2% m/m after falling 6.1% m/m driven by the volatile multi-dwelling component. Private houses rose 1.3% m/m after falling 1.3% in October but were still up only 3.2% y/y. They appear to be recovering from the Q2/Q3 2025 dip. Momentum is picking up across both houses and apartments but the former is still soft.

- Strong demand and supply shortages have driven home prices higher. Approvals have struggled to improve as needed. A gradual uptrend in the total has been due to the non-house component but it remains 20% below the 2021 peak.

- Queensland and Victoria drove the jump in multi-dwelling approvals, which were their highest since June 2018 and up 55.3% y/y.

- The level of house approvals has been moving sideways since Q3 2024. The November rise was due to NSW and Queensland while they fell in SA.

Australia number of dwellings approved

Source: MNI - Market News/ABS

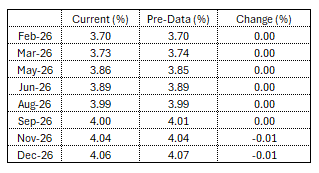

STIR: RBA-Dated OIS Little Changed Versus Pre-CPI Levels

RBA-dated OIS is little changed versus pre-CPI levels. The pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 38% for February to 116% by June and 184% by December 2026.

Figure 1: RBA-Dated OIS – Current

Source: Bloomberg Finance LP / MNI