MNI EUROPEAN MARKETS ANALYSIS: US PCE In Focus Later

- The USD has edged a little higher in the first part of Friday trade, with US Tsy yields up a touch. The Fed's Waller stated that data would determine the pace of Fed cuts.

- Tokyo CPI was in line with forecasts, while some services components were firmer in the month of August. JGB futures remain range bound. In South Korea the fiscal deficit will expand to 4% of GDP next year to spur economic transformation. China equities continue to rally.

- Looking ahead, prelim CPIs from France, Italy and Germany keep markets busy ahead of the US open, with July PCE, trade balance, MNI Chicago PMI and UMich sentiment data set to follow.

MARKETS

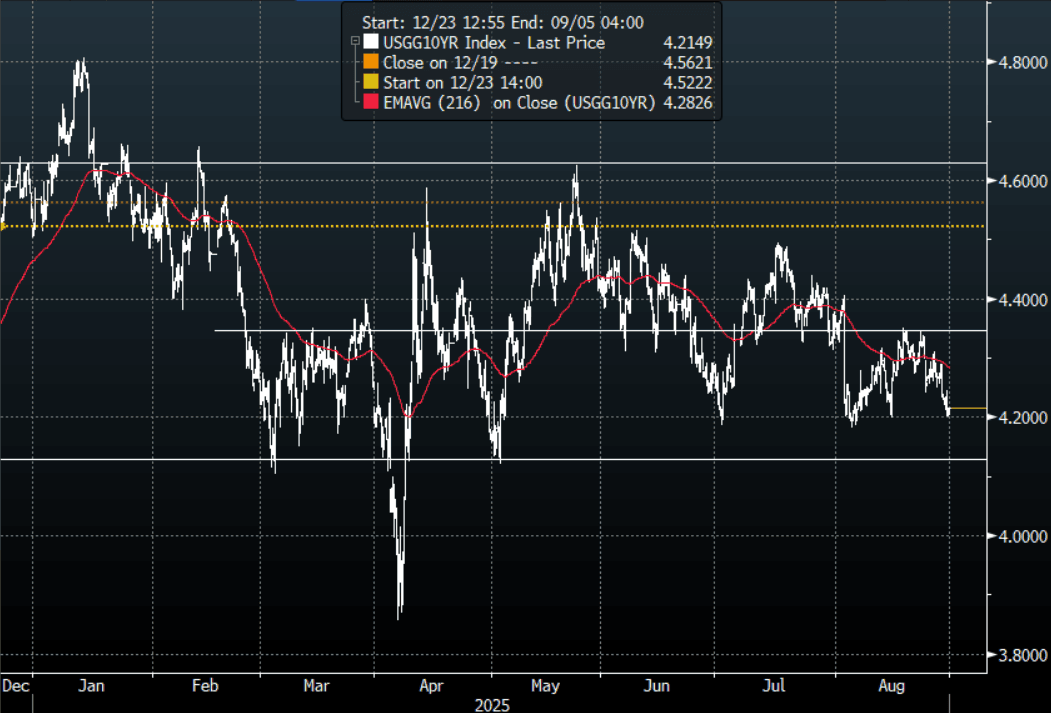

US TSYS: Yields Edge Higher In A Quiet Session

The TYU5 range has been 112-17 to 112-20+ during the Asia-Pacific session. It last changed hands at 112-17, down 0-02 from the previous close.

- The US 2-year yield is trading around 3.63%.

- The US 10-year yield has edged higher trading around 4.215%, up 0.01 from its close.

- (Bloomberg) -- A block of 3,800 contracts in five-year bond December futures traded at a price of 109-15 on CBOT.

- 10-Year Yields extended their move lower as demand increased as we head into month-end. While the 4.35% area holds, bounces should be met with demand. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

- Eric Daugherty on X: “BREAKING: FHFA Director Bill Pulte has filed ANOTHER CRIMINAL REFERRAL against Democrat Federal Reserve Governor Lisa Cook over mortgage fraud on a 3rd property, and misrepresentations about her properties to the U.S. government while serving on the Fed Board. “These inconsistencies appear Cook made additional, multiple false representations, including to the U.S. Government, regarding the status of her mortgages and properties.”

- Financelot on X: “Federal Reserve Lisa Cook's emergency hearing for a temporary restraining order and injunction against Trump is scheduled Aug 29, 2025 at 10 am.”

- MNI Brief: Waller Says Data Will Determine Fed Cut Pace. Waller said Thursday the pace of interest rate cuts will be determined by incoming data, but the direction lower to neutral is clear.

- Data/Events: Personal Income, PCE, Inventories, MNI Chicago PMI, U. of Mich. Sentiment, Kansas City Fed Services Activity

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: 30yr Yields Lower As Authorities Ask For Views On Longer Dated Supply

JGB futures sit off Thursday highs, last near 137.49, +.06 versus settlement levels. Recent lows sub 137.30 continue to hold though. Helping futures off recent highs has been a slightly softer tone for US Tsys futures so far today, although aggregate moves have been modest.

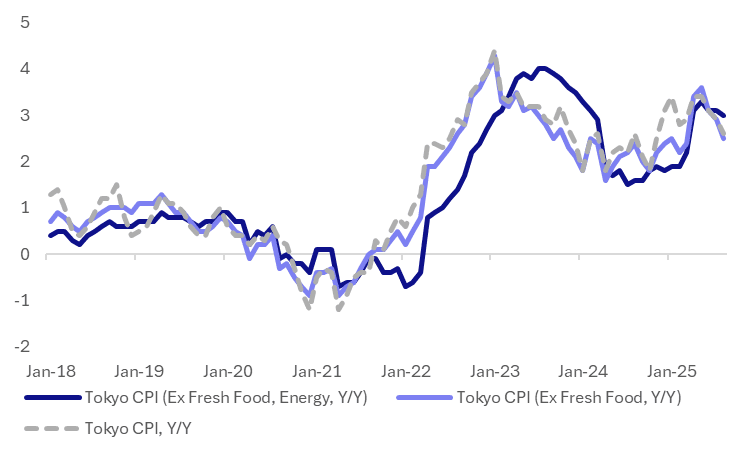

- Earlier we had a number of monthly data prints, which were mixed relative to expectations. Most notable was August Tokyo CPI, where the y/y outcomes all came in line with market expectations. Headline is now back to 2.6%y/y, against recent highs of 3.4%.

- However, the detail showed some firmness in m/m services inflation, led by a 2% gain for entertainment. In y/y terms services inflation was still edged down to 2% from 2.1%, so near term BoJ thinking may not be impacted.

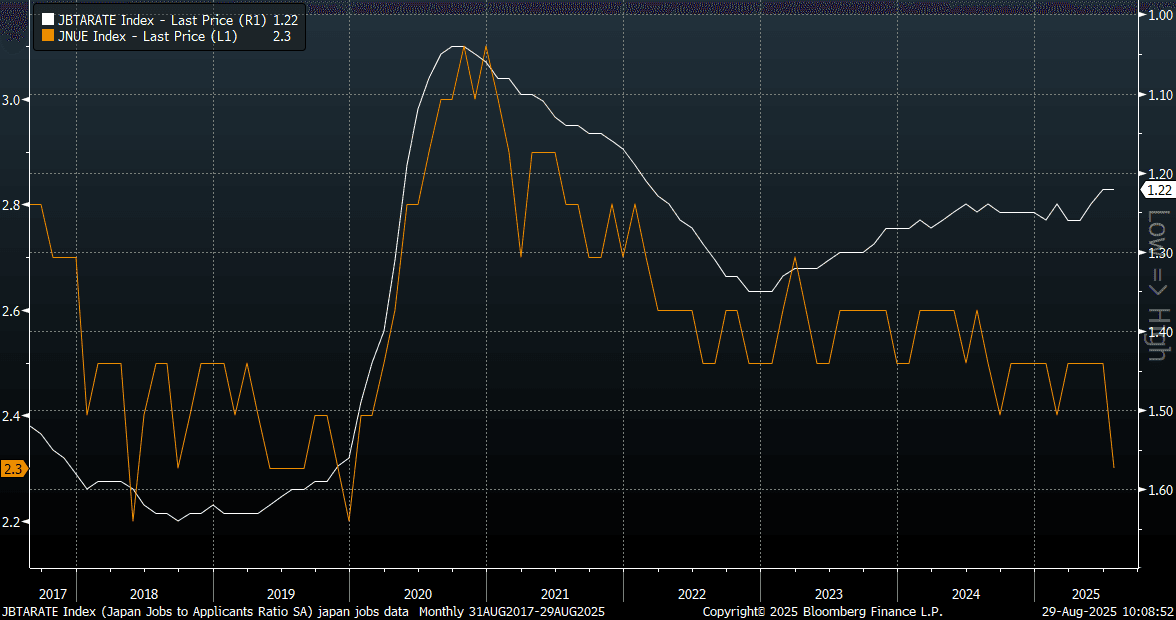

- Other data showed a dip in the jobless rate, but the job-to-applicant ratio was steady. Industrial output fell 1.6%m/m in July, against a -1.1m/m forecast. Automobile production declined 6.7%, the first fall in three months, reversing a 0.5% rise in June as front-loaded exports ahead of U.S. tariffs weighed.

- In the cash JGB space we have seen some softness in back end yields. The 30yr is down by around 2bps, last near 3.20%. The 10yr is holding under 1.62% at this stage. The 2/30's JGB curve is flatter by around 4bps to +232bps.

- New wires are reporting that the authorities are asking primary dealer for views around cutting longer term bond supply. BBG notes: "- Japan’s Ministry of Finance has asked primary dealers for their views on further reducing issuance of longer-maturity government bonds, according to people familiar with the matter." (see this link for more details).

- Next Monday we get Q2 capex, while on Tuesday BoJ Deputy Governor Himino speaks.

JAPAN DATA: Tokyo August CPI Y/Y In Line, But Services Inflation Edges Up M/M

The August Tokyo CPI print was in line with market expectations in terms of the y/y outcomes. The headline rose 2.6%y/y, versus 2.9% prior (2.6% was also the consensus estimate). Ex fresh food CPI was 2.5%y/y (2.9% prior), while the measure excluding fresh food and energy was 3.0%y/y (prior was 3.1%). The chart below plots these inflation trends, with headline lower, but core sticky in terms of ex fresh food, energy.

- In terms of the m/m details, there were slightly stronger themes. In seasonally adjusted terms, we rose 0.1%m/m for the headline while ex fresh food and energy was up 0.2%m/m. Goods prices were flat, but services were up 0.2%.

- In non-seasonally adjusted terms, the ex food, energy index rose 0.4%m/m, the strongest gain since April.

- In terms of the sub categories we saw a sharp fall in utilities of 5.1%m/m. This reflected government utility subsidies. Clothing fell by another 0.6%m/m.

- Other categories were mostly firmly, with entertainment rising 2.2%m/m, which follows a 0.6% rise in July. Food prices were up 0.8%m/m, while fresh food rose 3.2%.

- So outside of the sharp fall in utilities, inflation pressures were mostly firmer in August on a m/m basis.

Fig 1: Tokyo CPI Y/Y Trends, Core Still Elevated

Source: Bloomberg Finance L.P./MNI

JAPAN DATA: U/E Rate Down, But Divergences From Steady Job-To-Applicant Ratio

Japan's jobless rate surprised on the downside in July, printing at 2.3%, versus 2.5% forecast, which was also the June outcome. The job-to-applicant ratio ticked down a touch to 1.22, versus 1.23 forecast, while the June outcome was 1.22.

- The chart below shows the widening divergence between the jobless rate, which is now at fresh lows back to late 2019, and the job to applicant ratio (which is inverted on the chart).

- The labour force participation rate eased to 63.9% from 64.2% in June, with the m/m change for those not in the labour force rising by 150k. The number of people employed fell by -10k, after a -50k dip in June.

- So, whilst the jobless rate suggests a tight labour market, other indicators are painting a less hawkish picture.

Fig 1: Japan Jobless Rate & Job-To-Applicant Ratio (Inverted)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Futures Down, Led By Front End, AU-US10yr Spread Elevated

Aussie bond futures sit down a touch in Friday trade to date, with 3yr (YM) futures slightly softer, last at 96.575, off 2.5bps. 10yr futures (XM), were down 1bps to 95.68. Broader ranges are holding in both benchmarks, but the 10yr has underperformed US moves this week.

- For cash ACGB yields, we sit higher today, led by the front end. The 3 yr was last around 3.40%, up +2bps, while the 10yr was back near 4.29%. Both benchmarks are down a little over the past week, but not as much as US yield losses. The AU-US 10yr spread is threatening to test multi month highs, we were last near +8bps.

- Earlier July private credit data showed a 0.7%m/m rise, against a 0.6% forecast. We sit +7.2% in y/y terms.

- On the bond supply front via BBG: "Australia sold A$1 billion ($653.6 million) of bonds due Nov. 21, 2028 on Aug. 29. Investors offered to buy 4.12 times the amount of securities sold."

- Next week, the main focus will be on Wednesday's Q2 GDP print. Before then we get more partials, but at the momentum the markets is forecasting a 0.5%q/q gain, after +0.2% was recorded for Q1.

- We also have RBA speak from Governor Bullock next Wednesday, then Deputy Governor Hauser speaks with Rtrs on Thursday.

BONDS: NZGBS: Lower Yield Trend Persists, 2yr Off 8bps Past Week

NZGB yields have maintained a negative bias in Friday trade. This has been a fairly consistent theme this week, with the 2yr breaking under 3%, off close to 9bps since end levels last week (last around 2.94%). The 10yr is tracking at 4.31%, down close to 6bps in the past week.

- NZGB yields have bucked the slightly firmer US Tsy yield backdrop so far today, but the underlying theme from Thursday's session was mostly yield softness in terms of the majors.

- The 2yr swap rate is little changed so far today, last near 2.72%, off close to 8bps in the past week. By the Feb RBNZ meeting the market expects the RBNZ policy rate to be just above 2.50% per OIS pricing. This is little changed over the past week.

- The data trends have been mixed over the past week. Today's ANZ consumer confidence print underscores the fragility of the recovery, with sentiment back to late 2024 lows.

- Next week we have mostly second tier data, with building permits, terms of trade, ANZ commodity prices and Q2 volume of building work done all on tap.

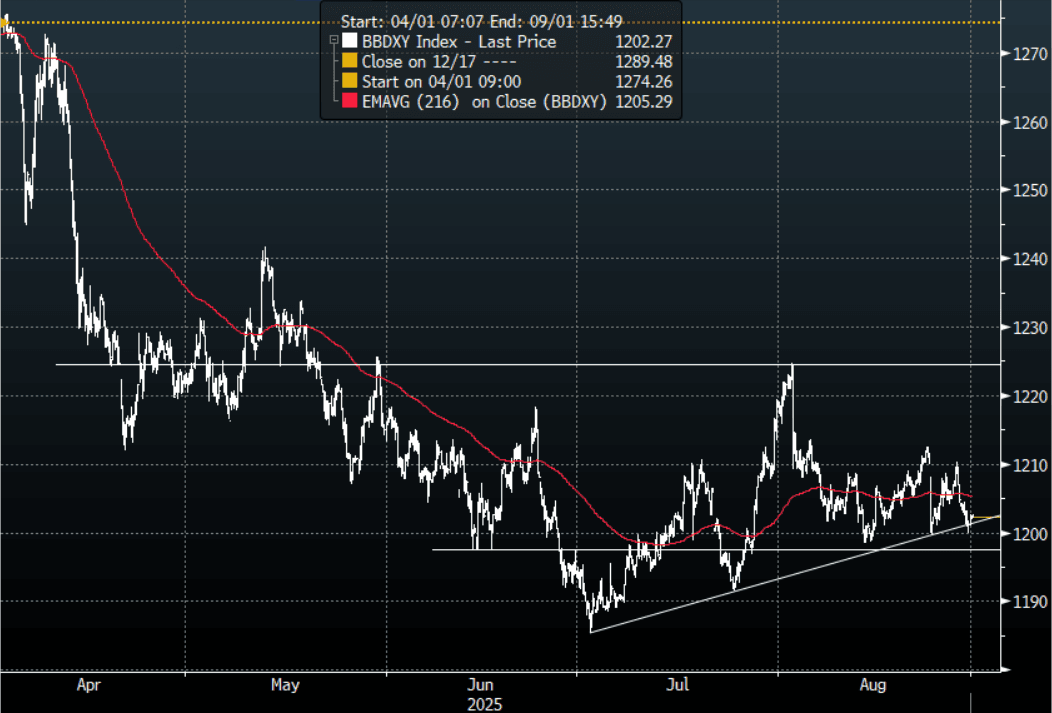

FOREX: Asia FX Wrap - USD Holding Above Support For Now

The BBDXY has had a range of 1201.01 - 1202.67 in the Asia-Pac session, it is currently trading around 1202, +0.10%. The broad USD selling continued overnight. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. The USD’s is holding just above this support but is trading very with a very heavy tone. Zerohedge on X: “Time to go long USD and TSYs, The judge assigned on the Lisa Cook case is Jia Cobb: she was appointed by Biden in 2021, and has repeatedly ruled against Trump.” https://www.politico.com/news/2025/08/28/federal-reserve-lawsuit-judge-jia-cobb-00533672

- EUR/USD - Asian range 1.1656 - 1.1683, Asia is currently trading 1.1665. The pair is consolidating just above its support. First support is back towards 1.1550, a move back below here could signal a deeper pullback as the market tries to find a base from which to build for another extension higher.

- GBP/USD - Asian range 1.3496 - 1.3513, Asia is currently dealing around 1.3500. The pair is consolidating around the 1.3500 area. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1159-7.1292, the USD/CNY fix printed 7.1030, Asia is currently dealing around 7.1250. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX -0.10%, Gold $3409, US 10-Year 4.213%, BBDXY 1202, Crude Oil $64.21

- Data/Events : Italy GDP/CPI, EZ ECB 73 Year CPI Expectations, Germany Retails Sales/Unemployment/CPI, France Consumer Spending/CPI/GDP/Payrolls/PPI, Spain CPI/Retails Sales/ Current Account Balance

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

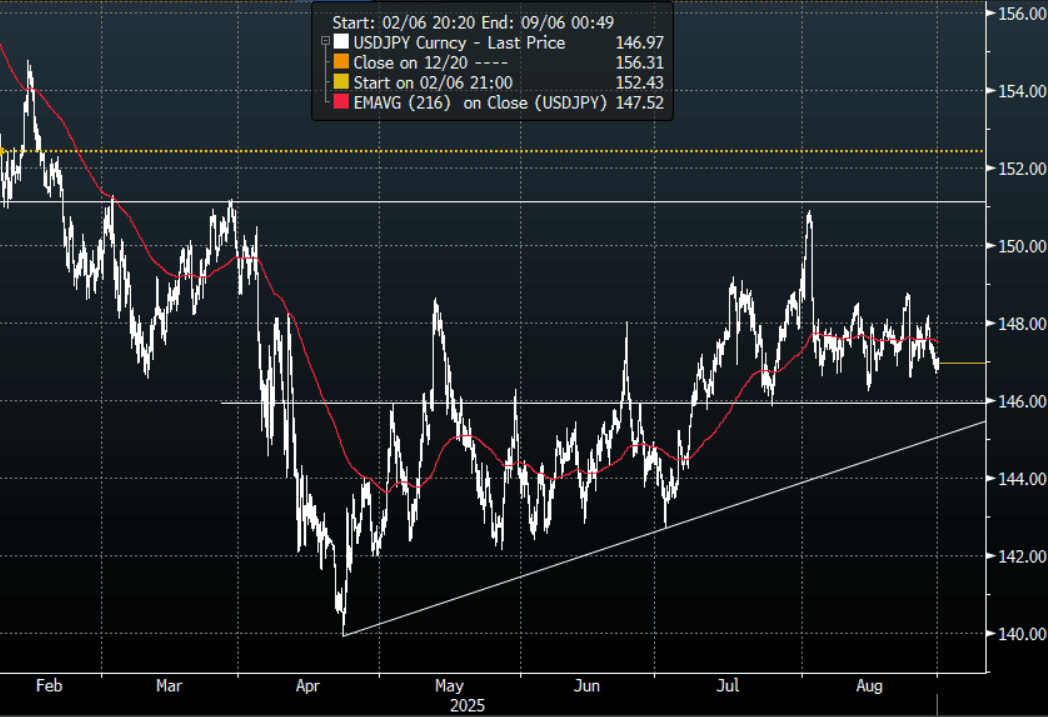

JPY: Asia Wrap - USD/JPY Consolidates Around 147.00

The Asia-Pac USD/JPY range has been 146.77-147.11, Asia is currently trading around 147.00, +0.05%. USD/JPY has consolidated around 147.00 in a quiet session. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so they will be betting on the support to continue to hold. A sustained break below 145.50/146.00 is needed to to turn the focus back to the year's lows towards 140.00.

- MNI Brief: Japan Aug Tokyo Core CPI Rises 2.5% Vs. July 29% - Tokyo’s core inflation slowed to 2.5% y/y but remained above 2% for the 10th straight month. The BOJ expects underlying CPI to weaken temporarily on softer growth before moving back toward its 2% target. Officials judged recent inflation to be stronger than expected, with high rice prices boosting food costs.

- MNI Brief: Japan July Factor Output Posts 1st Drop In 2 Months - Japan’s industrial output fell 1.6% m/m in July, the first drop in two months, after rising 2.1% in June due to weaker auto production. BOJ officials remain cautious over the impact of US tariffs on exports and production, with a focus on potential spillovers to corporate profits and wage growth.

- U/E Rate Down, But Divergences From Steady Job-To-Applicant Ratio: Japan's jobless rate surprised on the downside in July, printing at 2.3%, versus 2.5% forecast, which was also the June outcome. The job-to-applicant ratio ticked down a touch to 1.22, versus 1.23 forecast, while the June outcome was 1.22. Whilst the jobless rate suggests a tight labour market, other indicators are painting a less hawkish picture.

- “AKAZAWA: JAPAN STAFF MEMBERS IN US TO DISCUSS TRADE MATTERS, SEEK EARLY EXECUTIVE ORDER TO LOWER TARIFFS ON JAPAN, EXPECT TO VISIT US BEFORE EXECUTIVE ORDER COMES" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 145.00($1.17b Aug 29), 146.50($1.14b Aug 29), 147.50($806m Aug 29) - BBG.

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

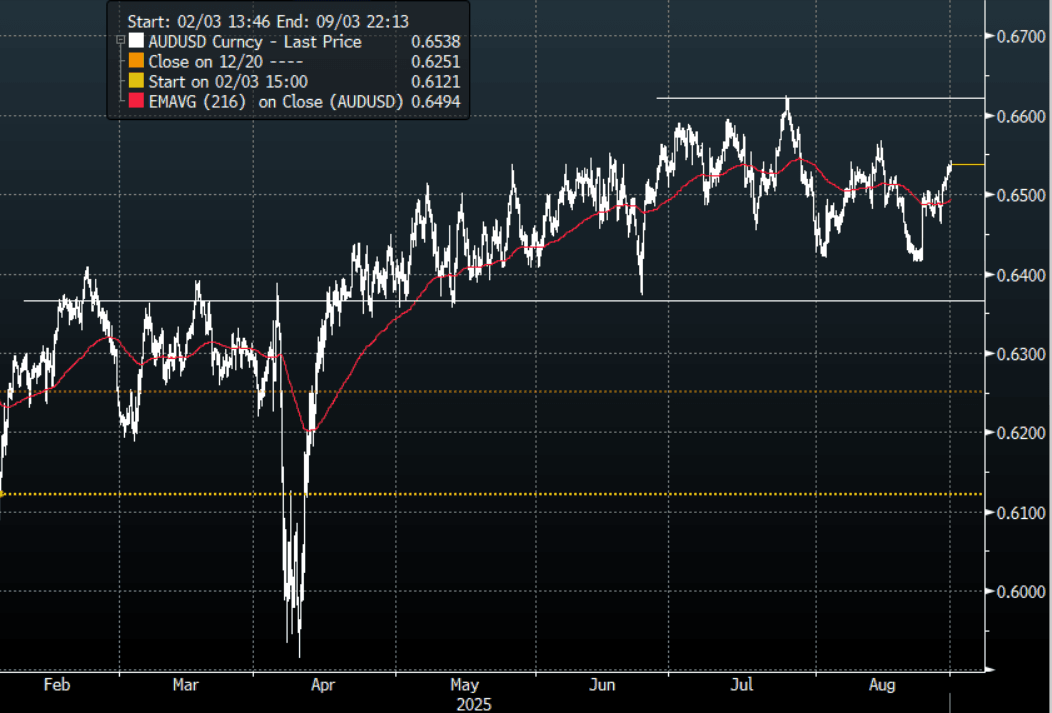

AUD: Asia Wrap - AUD/USD Drifts Higher In Quiet Session

The AUD/USD has had a range of 0.6527 - 0.6542 in the Asia- Pac session, it is currently trading around 0.6535, +05%. The AUD drifted higher in a very quiet Friday session. US Equity futures have traded a little lower, E-minis -0.10%, NQU5 -0.20%. The AUD is probing back above 0.6500 but with little momentum for the moment. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 with little clear long-term direction.

- "AUSTRALIA JULY PRIVATE CREDIT RISES 0.7% M/M; EST. +0.6%, AUSTRALIA JULY PRIVATE CREDIT RISES 7.2% Y/Y" - BBG

- “Lisa Cook sued to block Donald Trump’s attempt to fire her over alleged mortgage fraud. Her lawyers suggested the dispute may have stemmed from a “clerical error.”” - BBG

- Financelot on X: “Federal Reserve Lisa Cook's emergency hearing for a temporary restraining order and injunction against Trump is scheduled Aug 29, 2025 at 10 am.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD946m), 0.6515(AUD477m), 0.6560(AUD483m). Upcoming Close Strikes : 0.6400(AUD768m Sept 2), 0.6475(AUD569m Sept 3) - BBG

- AUD/JPY - Asia-Pac range 95.85 - 96.16, Asia is trading around 96.10. The pair continues to push up against the 96.00 area. This pair’s direction will be determined by the market's ability to follow on with this risk-on move or not. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Drifts Higher In Quiet Session

The NZD/USD had a range of 0.5880 - 0.5895 in the Asia-Pac session, going into the London open trading around 0.5890, +0.10%. The NZD has drifted higher in a quiet session. Data overnight showed the US economy is still expanding and risk reacted in kind, but the USD can’t catch a break and remains heavy. The NZD has bounced off its support toward 0.5800, sellers should continue to be around looking to fade the move back towards the 0.5950 area initially.

- ANZ Consumer Confidence Measure Falters, Back To Late 2024 Levels: The ANZ August consumer confidence print fell by 2.9% to 92.0. This is back to levels from late last year. The chart below plots the headline consumer confidence measure against NZ private consumption growth from the national accounts. The current sentiment backdrop is not implying a dramatic lift in spending trends, although we have seen divergences in the past.

- New Zealand July Residential Lending Rises 5.1% From Year Ago: RBNZ publishes sector lending figures for July, on website. Total housing lending rises by ~NZ$1.3b m/m to NZ$380.5b, Gains by NZ$18.4b or 5.1% y/y — fastest annual pace since October 2022.

- “FONTERRA JULY NZ MILK COLLECTION RISES 1% Y/Y:FSF NZ" - BBG

- “NEW ZEALAND WEIGHS RELAXING HOME-BUYING BAN FOR RICH FOREIGNERS" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD500m Sept 2), 0.5700(NZD384m Sept 3) - BBG

- AUD/NZD range for the session has been 1.1095 - 1.1119, currently trading 1.1100. The dovish RBNZ has seen the Cross surge higher breaking back above 1.1000 convincingly. First signs overnight of momentum stalling above 1.1100, look for dips back towards 1.1000/1.1030 to be supported.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China's Rally Continues as Turnover Leaps

Data on turnover for the month for China stocks shows the key equity bourses are heading for a record month for turnover, as per BBG. The average turnover for August has topped the previous monthly record. Naturally this has seen the major bourses deliver strong returns as retail investor led momentum is growing rapidly.

- The Hang Seng delivered decent gains Friday of +0.63%, yet not enough to turn the weekly performance to positive as it remains down just over -0.70%. The onshore bourses however have had a different week with the CSI 300 up +0.58% today and +2.55% for the week, Shanghai up +016% today and +0.63% for the week, and Shenzhen rising +0.45% today and +2.06% over the last five days.

- The NIKKEI stumbled into the end of the week with a fall of -0.25% and is barely holding onto a weekly gain of +0.20%.

- In Taiwan, the TAIEX is up +0.48% and +2.47% for the week even as foreign flows turn negative.

- The KOSPI has had a weak end to the week, down -0.22%, yet remains up by +0.65% for the week as it heads into a big week of data next week.

- The FTSE Malay KLCI has had a tough period and is down -1.33% for the week, with falls of -0.66% today.

- The Jakarta Composite fell heavily today by -2.27%, which looks more technically driven as it hit new all time highs earlier this week.

- In Singapore, the Straits Times is up +0.37% for the week whilst the PSEi in the Philippines is down -1.8%

- India's NIFTY 50 is one of the worst regional performers down modestly today, but over -2.4% for the week.

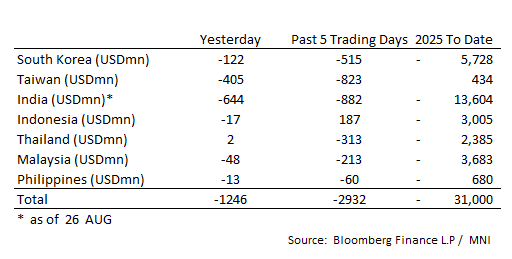

ASIA STOCKS: Significant Outflows for the Week for Major Markets

The outflows continue across the region with the 5-day total nearing $3bn .

- South Korea: Recorded outflows of -$122m yesterday, bringing the 5-day total to -$515m. 2025 to date flows are -$5,728. The 5-day average is -$103m, the 20-day average is -$44m and the 100-day average of +$15m.

- Taiwan: Had outflows of -$405m yesterday, with total outflows of -$823 m over the past 5 days. YTD flows are positive at +$434. The 5-day average is -$165m, the 20-day average of -$96m and the 100-day average of +$183m.

- India: Had outflows of -$644m as of the 26th, with total outflows of -$882m over the past 5 days. YTD flows are negative -$13,604m. The 5-day average is -$176m, the 20-day average of -$187m and the 100-day average of -$8m.

- Indonesia: Had outflows of -$17m yesterday, with total inflows of +$187m over the prior five days. YTD flows are negative -$3,005m. The 5-day average is +$37m, the 20-day average +$33m and the 100-day average -$12m.

- Thailand: Recorded inflows of +$2m yesterday, with outflows totaling -$313m over the past 5 days. YTD flows are negative at -$2,385m. The 5-day average is -$63m, the 20-day average of -$27m and the 100-day average of -$13m.

- Malaysia: Recorded outflows as of -$48m yesterday, totaling -$213m over the past 5 days. YTD flows are negative at -$3,683m. The 5-day average is -$43m, the 20-day average of -$37m and the 100-day average of -$13m.

- Philippines: Recorded outflows of -$13m yesterday, with net outflows of -$60m over the past 5 days. YTD flows are negative at -$680m. The 5-day -$12m, the 20-day average of -$3m the 100-day average of -$5m.

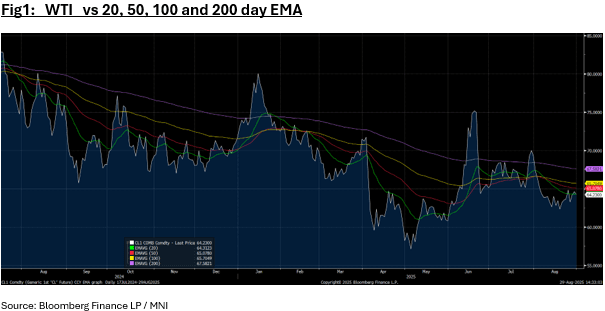

Oil Holding on to Modest Weekly Gain

- Whilst gold has delivered overall gains this week, it remains down over 7% in August, for it's biggest monthly loss since the start of the trade war in April.

- Down -0.57%, WTI at US$64.23 bbl remains up over +0.90% for the week.

- The falls today sees WTI trading through the 20-day EMA of $64.31 and closing below could point to further downward pressure on prices next week.

- Brent is down -0.55% today at US$68.24, yet remains up +0.75% for the week. For August, Brent is down -5.9%.

- Oil markets will be focusing in on Ukraine, Russia developments

- This comes as the German Chancellor says that the meeting between Ukrainian President Volodymyr Zelenskiy and Russia's Vladimir Putin "won't happen", thus increasing the likelihood of further action from the US.

- The European Union is considering introducing secondary sanctions to prevent third countries from helping Russia circumvent existing punitive measures to complement the US pressure, with President Trump possibly about to release a statement on the situation that could ultimately impact the flow of Russian oil.

- Despite further risks from the US, President Putin met with President Xi and PM Modi to discuss their energy needs and the supply of Russian oil.

- White House trade adviser Peter Navarro is pressuring India to halt its purchases of Russian oil, accusing New Delhi of funding the Kremlin's campaign in Ukraine.

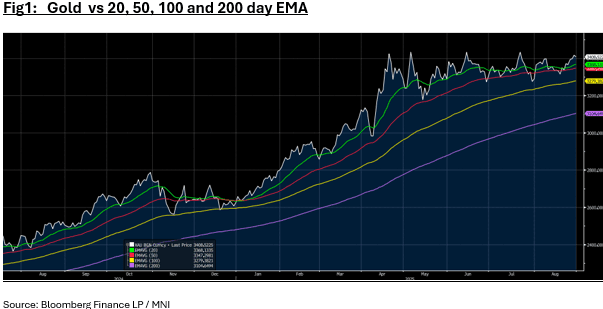

Gold Softens in Asia Trading Ahead of US Data Release

- Whilst gold has given back some of the overnight gains in Asia today, it remains close to it's all time high of US$3,418.38 and set for another weekly gain.

- Up +1.12% for the week, gold has fallen -0.22% during the day to be $3,409.70 yet retain its position above all major moving averages; underscoring a modest bullish momentum.

- Gold had edged higher in the US trading session leading into the Friday release of the US personal consumption report - the Fed's preferred inflation gauge.

- The PCE is expected to accelerate at the fastest annual pace in five months; a result that may limit the central bank's ability to ease policy and just a day after stronger than expected GDP for second quarter.

- A data release that creates doubts for a rate cut will continue to heap pressure on the Federal Reserve from the White House.

- The Federal Reserve Chair opened the door last week at Jackson Hole on a rate cut, with swaps markets pricing moving rapidly to increase the probability.

- Gold is up +30% year to date and looking for a trigger for a further rally and a rate cut could be that catalyst.

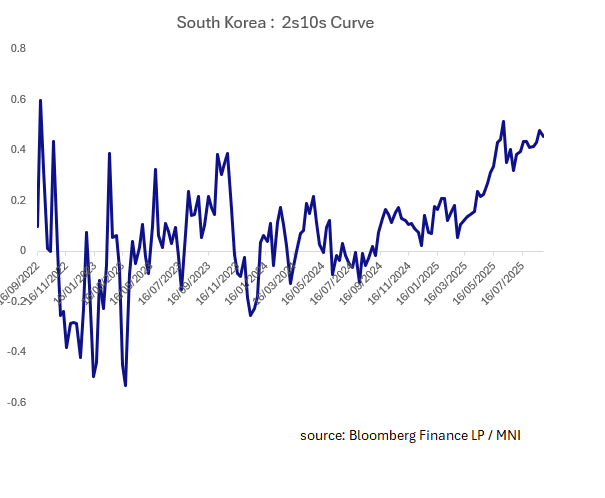

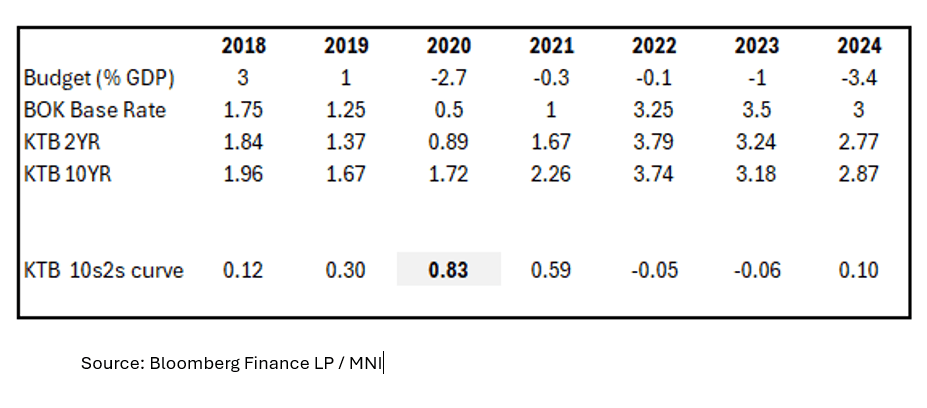

SOUTH KOREA: 2s10s Curve Update

- The steepening of the curve had taken a breather leading up to the BOK meeting this week having reached +48 late last week.

- After a year high of +51bps in early June, the 2s10s curve differential had backed off to +35bps by the end of June before issuance led-steepening in August.

- Following the BOK no change this week, the curve stands at +45

- Next week is a big week for data with exports, PMI Manufacturing, CPI and 2Q GDP preliminary.

- The Korean bond market has the highest correlation to the US bond market according to our analysis. The UST 10s2s steepening began at the start of April when the US curve started to move.

- The Korean curve could start to re-calibrate growth expectations for 2025, particularly with today's announcement from the Korean Government.

- Current forecasts suggest a mere +1.0% GDP growth for 2025 as South Korea’s new government plans a significant increase of its annual budget to revive an economy under pressure from US tariffs, rising welfare costs and an aging population.

- The proposed budget for 2026 is an +8.1% increase and includes ramped-up defense spending and aims to spur an “economic transformation” by channeling support into sectors including artificial intelligence, semiconductors, shipbuilding and K-culture.

- The government plans to issue a record amount of bonds to fund the government spending and will target technology-driven growth, stronger small businesses and more balanced regional development.

- In 2020 the COVID impacted budget resulted in a deficit of -2.7% and GDP growth the following year of 4.6%. The deficit for 2024 was -3.4% with a skew towards the back end of the year. The 2025 budget forecast increase and would be two meaningful deficits in two years for the first time in some time following 2024's deficit of -3.4%.

- Looking back at 2020, the curve finished the year end at 0.83 as the COVID economy required significant budget spend. It then moved higher again in early 2021 before trending lower.

- This could suggest potential steepening to occur in Q3 for 2025 for KTBs as growth is recalibrated. Additionally, if the BOK were to cut one more time (as some market observers are suggesting) when combined with supplementary budgets, the impact on growth could be meaningful.

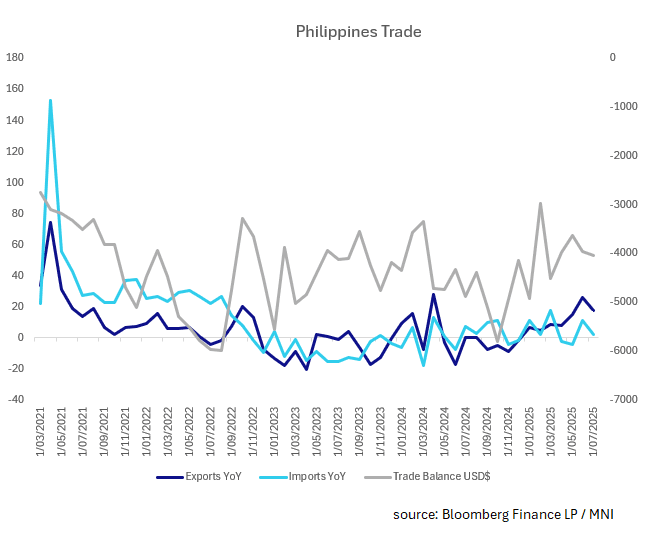

PHILIPPINES: July Exports Surprise to the Upside

- Against expectations for a rise of +10.5%, Philippines July exports rose +17.3% with June's release revised up to +26.9%.

- Regional exports have remained volatile for Asia's exporters yet since the period in April when tariffs were first announced, the Philippines is one of the few to not report a month of contraction.

- Mining and agriculture remain the main stay of exports, alongside electronic products and clothing.

- The largest contraction was in petroleum products.

- By country, the largest declines were to the US which at +9.7%, was materially down from June's result of +35.2%.

- Hong Kong and China saw significant rebounds whilst all others moderated month on month.

- Imports rose more than expected at +2.3%, but significantly down from the revised June result of +15.7%.

- The trade deficit rose to US$4.05bn with the US and Germany being the only major trading partners with a surplus (of $446m and $109m respectively). China's trade deficit increased to $2.5bn, whilst with the exception of Thailand, all others saw modest increases in their deficits.

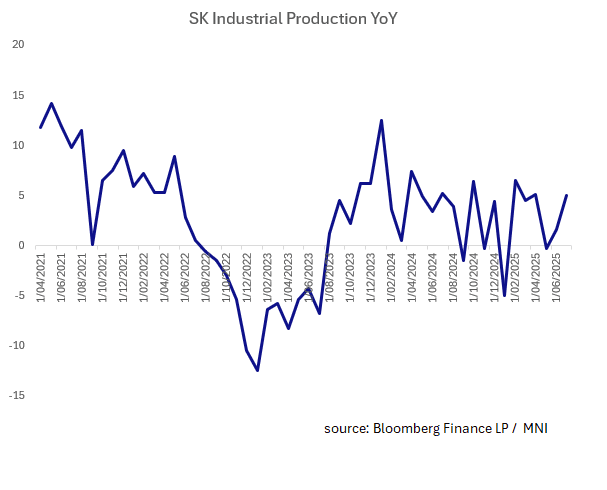

SOUTH KOREA: Industrial Production Rises After Rate Hold

- A significant uptick in the July industrial production a day after the BOK held rates, shows that the Central Bank has time to consider their next move.

- South Korea's July industrial production rose +5.0%, beating estimates of +3.9% YoY

- The month-on-month figure rose +0.3%, ahead of expectations, but down significantly on the prior month's revised result of +1.7%.

- The Cyclical change index rose to +0.5%, from +0.2% prior.

- The BOK held rates steady yesterday at 2.50%. The Governor noted that the decision reflected concerns about rapidly rising mortgage debt, especially in Seoul, and ongoing financial instability from slowing growth, albeit with some early signs of improvement. Export growth remained solid for a second consecutive month, driven by strong demand in semiconductors and automobiles, aided in part by front-loading amid tariff concerns . Whilst growth projections were slightly upgraded-from 0.8% to 0.9% for the year-this still marks the slowest growth since 2020 . Inflation risks appear manageable, supporting the likelihood of a more gradual easing cycle. The press conference emphasized a balanced approach to monetary easing with market commentators now expecting a possible 25 basis point rate cut in October, contingent on economic developments

ASIA FX: Mixed Trends In NEA, USD/CNH Edges Higher After Thursday Slump

In North East Asia FX, trends have been mixed. The won has struggled but USD/KRW remains sub recent highs. We have seen a modest bound in USD/CNH, but the majority of Thursday's break lower has held. TWD and HKD haven't shifted dramatically.

- USD/CNH got to lows of 7.1159 prior to the USD/CNY fixing. The fix was set lower at 7.1030, but the market was arguably looking for greater downside. USD/CNH was supported post the fixing but didn't test back above 7.1300. The pair was last near 7.1250. Onshore equities continued to push higher, the CSI 300 up a further 0.60%.

- Spot USD/KRW has pushed back above 1388, up around 0.25% versus end Thursday levels. The authorities are stepping up fiscal stimulus, with a wider fiscal deficit next year (4% of GDP, versus 2.8% this year). Local bond yields are little changed though. IP for July was stronger than expected, up 5.0%y/y. Local equities have ticked lower, off 0.20%, with offshore investors net sellers of local stocks this week (-$593.5mn).

- Spot USD/TWD is little changed, last around 30.55.

- USD/HKD spot is near 7.7910, with Hibor rates up strongly in the past week. This keeps us below the mid point of the peg band.

ASIA FX: USD/IDR Higher On Onshore Protests

In South East Asia FX, USD/IDR gains are the standout. We last tracked near 16445/50, against earlier highs of close 16494. Indonesian asset markets have been under pressure in the aftermath of onshore protests. Via BBG: "Indonesia is bracing for more protests on Friday after a motorcycle taxi driver was killed in clashes between demonstrators and the police, fueling public anger against the government and raising questions about President Prabowo Subianto’s handling of dissent." (see this link). Earlier headlines also crossed that BI has been in the market to stabilize IDR. Local equities are off over 2%.

- Elsewhere, markets are more quiet. USD/PHP has been supported sub 57.00 after yesterday's BSP cut, but recent ranges prevail.

- USD/THB is around 32.35/40, up from earlier lows of 32.26. A Thailand court is also expected to decide the fate of Prime Minister Paetongtarn Shinawatra today.

- USD/MYR is under 4.2200, little changed for Friday dealings so far.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/08/2025 | 0600/0800 | *** | GDP | |

| 29/08/2025 | 0600/0800 | ** | Retail Sales | |

| 29/08/2025 | 0600/0800 | ** | Import/Export Prices | |

| 29/08/2025 | 0600/0800 | ** | Retail Sales | |

| 29/08/2025 | 0630/0730 | DMO to release FQ3 (Oct-Dec) issuance ops calendar | ||

| 29/08/2025 | 0645/0845 | *** | HICP (p) | |

| 29/08/2025 | 0645/0845 | ** | PPI | |

| 29/08/2025 | 0645/0845 | *** | GDP (f) | |

| 29/08/2025 | 0645/0845 | ** | Consumer Spending | |

| 29/08/2025 | 0700/0900 | *** | HICP (p) | |

| 29/08/2025 | 0755/0955 | ** | Unemployment | |

| 29/08/2025 | 0800/1000 | *** | GDP (f) | |

| 29/08/2025 | 0800/1000 | *** | Bavaria CPI | |

| 29/08/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 29/08/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 29/08/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/08/2025 | 0900/1100 | *** | HICP (p) | |

| 29/08/2025 | 0900/1100 | ECB de Guindos at Cursos Europeos de Verano | ||

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1200/1400 | *** | Germany CPI (p) | |

| 29/08/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 29/08/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 29/08/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 29/08/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 29/08/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/08/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 29/08/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 29/08/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 29/08/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 29/08/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |