BONDS: NZGBS: Lower Yield Trend Persists, 2yr Off 8bps Past Week

NZGB yields have maintained a negative bias in Friday trade. This has been a fairly consistent theme this week, with the 2yr breaking under 3%, off close to 9bps since end levels last week (last around 2.94%). The 10yr is tracking at 4.31%, down close to 6bps in the past week.

- NZGB yields have bucked the slightly firmer US Tsy yield backdrop so far today, but the underlying theme from Thursday's session was mostly yield softness in terms of the majors.

- The 2yr swap rate is little changed so far today, last near 2.72%, off close to 8bps in the past week. By the Feb RBNZ meeting the market expects the RBNZ policy rate to be just above 2.50% per OIS pricing. This is little changed over the past week.

- The data trends have been mixed over the past week. Today's ANZ consumer confidence print underscores the fragility of the recovery, with sentiment back to late 2024 lows.

- Next week we have mostly second tier data, with building permits, terms of trade, ANZ commodity prices and Q2 volume of building work done all on tap.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBA: VIEW: Westpac Expects Cuts At Next Four SoMP Meetings

Q2 trimmed mean inflation printed at 0.6% q/q and 2.7% y/y after 0.7% & 2.9% in Q1. Westpac believes two consecutive prints at seasonally-adjusted 0.6-0.7% q/q show that underlying inflation is within the band and so the RBA can continue easing in August. It believes that will be followed by 25bp cuts in November, February and May – all Statement on Monetary Policy meetings that include updated staff forecasts.

- Westpac notes that Q2 CPI data “removes any awkwardness posed by inflation remaining too high for the RBA’s comfort, at the same time that the labour market might be starting to ease again”.

- “Further softening in the labour market would sit uncomfortably with a decision to hold the cash rate at restrictive levels when underlying inflation is so close to target.”

- “We expect the RBA to cut the cash rate by 25bps at its August meeting to 3.6%. With internal members likely switching their votes from hold to cut, we expect the external members who voted to hold in July will also switch to a vote to cut, leading to a unanimous decision.”

- “Assuming our expectations are borne out, that would take the cash rate to a trough of 2.85%. We think this is at the lower end of what could be regarded as neutral, and would reflect the RBA’s response to a path for underlying inflation that turns out a little lower than what it forecast in May.”

- RBA Deputy Governor Hauser speaks on Thursday and could give more information on “how the RBA staff are seeing the data and whether the ongoing disinflation revealed in today’s data is expected to continue”. “The Governor and Deputy Governor will not give guidance in public appearances between meetings. That would front-run the meeting and pre-empt the MPB’s decision.”

BOJ: MNI BoJ Preview - July 2025: Focus On Presser After Trade Deal

EXECUTIVE SUMMARY

- The two-day Bank of Japan (BoJ) policy meeting concludes on 31 July, with the central bank set to release its quarterly “Outlook for Economic Activity and Prices”, its monetary policy statement, and hold a press conference with Governor Kazuo Ueda.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting.

- Most analysts continue to expect the next rate hike to occur in late 2025 or January 2026. However, timing remains fluid.

- Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.

- However, with OIS markets pricing in a 65% chance of a 25bp rate hike by end-2025, the bar for a hawkish surprise is high. As a result, even a mild shift in tone could be interpreted as dovish, relative to expectations.

- Full preview here

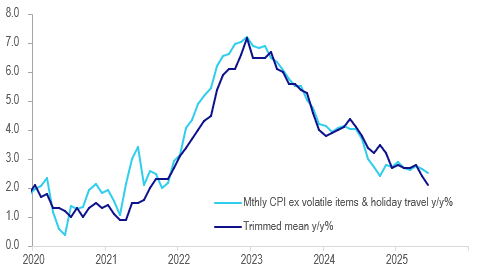

AUSTRALIA DATA: Complete Monthly CPI In November, June Prints Around 2%

The RBA has been reluctant to rely on the monthly CPI series as it only covers around two thirds of the quarterly index. However, in November the ABS will move to a complete monthly CPI for the October release which will run alongside the quarterly series until full seasonal adjustment factors are included. In June, the current trimmed mean CPI moderated to 2.1% y/y from 2.4% in May, the lowest since August 2021, and headline to 1.9% from 2.1%.

Australia monthly core CPIs y/y%

Source: MNI - Market News/ABS

- Another measure of underlying inflation, CPI ex volatile items & holiday travel, continued to run above the trimmed mean at 2.5% y/y but did moderate from 2.7% in May. However, June remained above the 2024 low of 2.4% and the 3-month annualised rate is 3.8%.

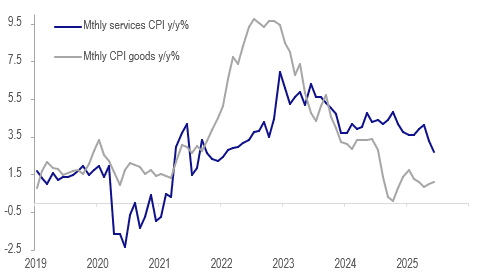

- Services and non-tradeables also moderated in June to 2.7% y/y and 2.8% y/y respectively. Services is its lowest since January 2022’s 2.4%.

- Goods inflation was steady at 1.1% and tradeables remained flat on the year.

Australia monthly goods vs services CPIs y/y%