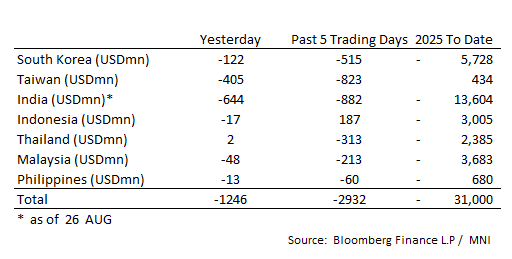

ASIA STOCKS: Significant Outflows for the Week for Major Markets

Aug-29 02:09

The outflows continue across the region with the 5-day total nearing $3bn .

- South Korea: Recorded outflows of -$122m yesterday, bringing the 5-day total to -$515m. 2025 to date flows are -$5,728. The 5-day average is -$103m, the 20-day average is -$44m and the 100-day average of +$15m.

- Taiwan: Had outflows of -$405m yesterday, with total outflows of -$823 m over the past 5 days. YTD flows are positive at +$434. The 5-day average is -$165m, the 20-day average of -$96m and the 100-day average of +$183m.

- India: Had outflows of -$644m as of the 26th, with total outflows of -$882m over the past 5 days. YTD flows are negative -$13,604m. The 5-day average is -$176m, the 20-day average of -$187m and the 100-day average of -$8m.

- Indonesia: Had outflows of -$17m yesterday, with total inflows of +$187m over the prior five days. YTD flows are negative -$3,005m. The 5-day average is +$37m, the 20-day average +$33m and the 100-day average -$12m.

- Thailand: Recorded inflows of +$2m yesterday, with outflows totaling -$313m over the past 5 days. YTD flows are negative at -$2,385m. The 5-day average is -$63m, the 20-day average of -$27m and the 100-day average of -$13m.

- Malaysia: Recorded outflows as of -$48m yesterday, totaling -$213m over the past 5 days. YTD flows are negative at -$3,683m. The 5-day average is -$43m, the 20-day average of -$37m and the 100-day average of -$13m.

- Philippines: Recorded outflows of -$13m yesterday, with net outflows of -$60m over the past 5 days. YTD flows are negative at -$680m. The 5-day -$12m, the 20-day average of -$3m the 100-day average of -$5m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bonds Mostly Richer, Focus On Tomorrow's BoJ Decision

Jul-30 02:00

In Tokyo morning trade, JGB futures are stronger but off bests, +12 compared to settlement levels.

- Today, the local calendar will be empty ahead of the BoJ Policy Decision tomorrow.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's strong gains. The focus is on today's FOMC meeting.

- The two-day Bank of Japan (BoJ) policy meeting concludes on 31 July, with the central bank set to release its quarterly “Outlook for Economic Activity and Prices”, its monetary policy statement, and hold a press conference with Governor Kazuo Ueda.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting.

- Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.

- Cash JGBs are 1-2bps richer across benchmarks, apart from the 20-30-year zone, which is slightly cheaper. The benchmark 10-year yield is 1.7bps lower at 1.561% versus the cycle high of 1.616%.

- Swap rates are flat to 2bps higher. Swap spreads are wider.

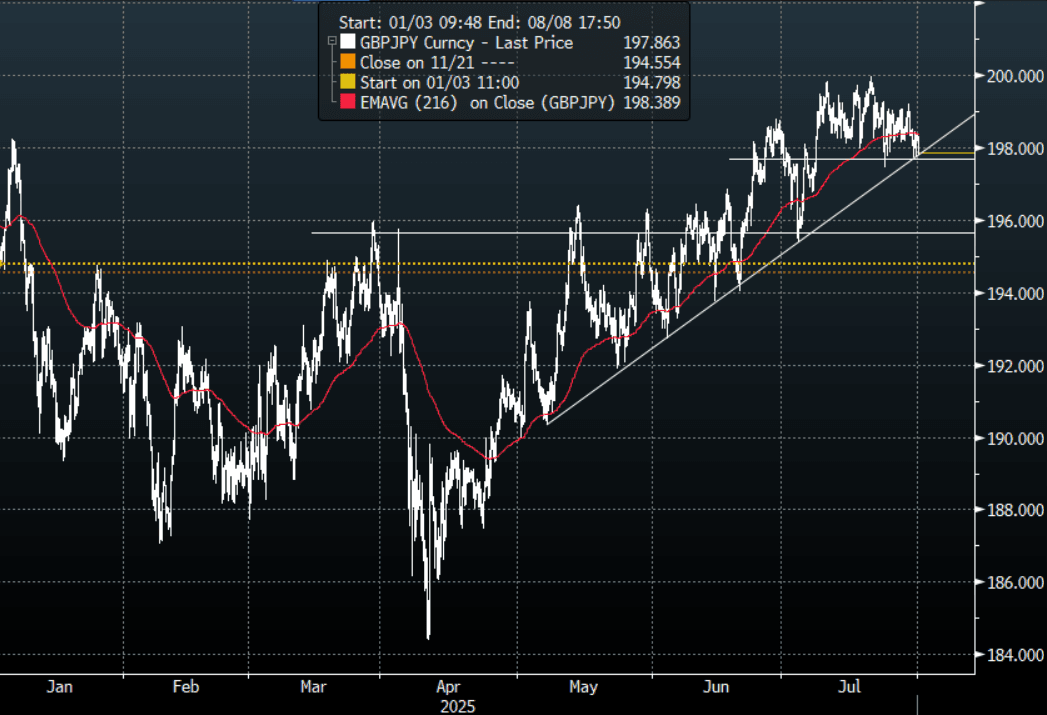

FOREX: JPY Crosses - Momentum Higher Has Stalled ?

Jul-30 01:56

US Stocks drifted lower as some risk was taken off heading into a big week. This morning has seen US futures open slightly higher, ESU5 +0.10%, NQU5 +0.15%. Price action suggests the crosses' momentum higher is stalling, event-risk posed by this week though could provide some additional short-term challenges.

- EUR/JPY - Overnight range 171.05 - 172.08, Asia is trading around 171.30. This pair has had a decent move higher and has led the charge against the JPY longs. Short-term it is starting to look a little stretched but the direction is clear and should expect demand on dips. First support 170.00 area then the more important 168.00 area.

- GBP/JPY - Overnight 197.74 - 198.46, Asia trades around 197.85. The pair continues to find strong demand just below the 198.00 area. A sustained move sub 1.9750 could signal a deeper correction back to the 195.00 area.

- NZD/JPY - Overnight range 88.34 - 88.58, Asia is currently dealing 88.35. The pair has failed to gain momentum above 89.00, with the move stalling price looks to settle back in its 87.00 - 89.00 range.

- CNH/JPY - Overnight range 20.6379 - 20.7118, Asia is currently trading around 20.6400. This pair found strong demand towards its 20.3000/20.4000 support area, but upward momentum seems to be failing again towards the 20.7000/20.8000 resistance. A sustained move back below 20.3500/20.4000 is needed to turn the pendulum back towards the Bears.

Fig 1 : GBP/JPY 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Gaps Richer After Trimmed Mean CPI Miss

Jul-30 01:49

ACGBs (YM +7.0 & XM +6.5) are sharply higher after the release of lower-than-expected trimmed mean CPI.

- Q2 trimmed mean CPI printed close to Bloomberg consensus at 0.6% q/q and 2.7% y/y, down from Q1’s 0.7% & 2.9%. This is close enough to the RBA’s May 2.6% Q2 forecast to allow it to ease on August 12. June moderated to 2.1% y/y from May’s 2.4%. Headline was lower than expected at 0.7% q/q and 2.1% y/y after 0.9% & 2.4%.

- Cash US tsys are little changed in today’s Asia-Pac session after yesterday’s strong gains. The focus is on today’s FOMC meeting.

- Cash ACGBs are 4-7bps richer after the data, with the AU-US 10-year yield differential at -6bps.

- The bills strip has shunted stronger, with pricing +4 to +8.

- RBA-dated OIS pricing is 3-7bps softer across meetings after the data. A 25bp rate cut in August is given a 100% probability, with a cumulative 66bps of easing priced by year-end (based on an effective cash rate of 3.84%).