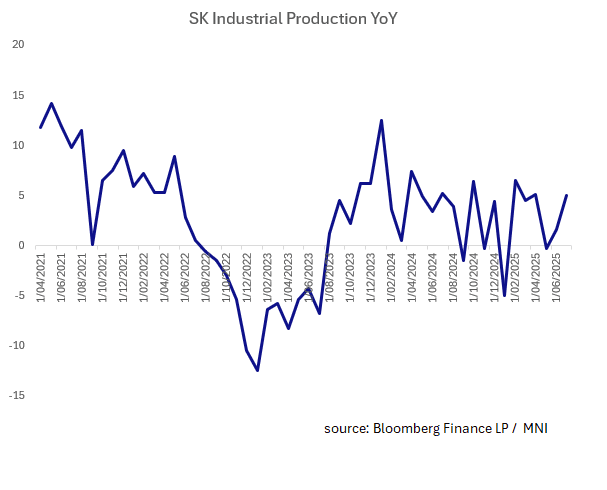

SOUTH KOREA: Industrial Production Rises After Rate Hold

Aug-28 23:29

- A significant uptick in the July industrial production a day after the BOK held rates, shows that the Central Bank has time to consider their next move.

- South Korea's July industrial production rose +5.0%, beating estimates of +3.9% YoY

- The month-on-month figure rose +0.3%, ahead of expectations, but down significantly on the prior month's revised result of +1.7%.

- The Cyclical change index rose to +0.5%, from +0.2% prior.

- The BOK held rates steady yesterday at 2.50%. The Governor noted that the decision reflected concerns about rapidly rising mortgage debt, especially in Seoul, and ongoing financial instability from slowing growth, albeit with some early signs of improvement. Export growth remained solid for a second consecutive month, driven by strong demand in semiconductors and automobiles, aided in part by front-loading amid tariff concerns . Whilst growth projections were slightly upgraded-from 0.8% to 0.9% for the year-this still marks the slowest growth since 2020 . Inflation risks appear manageable, supporting the likelihood of a more gradual easing cycle. The press conference emphasized a balanced approach to monetary easing with market commentators now expecting a possible 25 basis point rate cut in October, contingent on economic developments

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Richer With US Tsys Ahead Of Q2 CPI

Jul-29 23:16

ACGBs (YM +2.5 & XM +3.5) are stronger after US tsys finished richer and near session bests ahead of today’s FOMC decision.

- US tsys rallied after lower-than-expected JOLTS openings, quits level lower (prior down-revised), and layoffs broadly lower than expected.

- A strong 7Y note auction helped rates extend gains after the $44B note sale stopped through again: 4.092% high yield vs. WI of 4.120%; bid-to-cover 2.79x from 2.46x prior.

- Today will see Q2 CPI data. It is expected to show the underlying trimmed mean measure making further progress towards the band midpoint of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Cash ACGBs are 2-3bps richer with the AU-US 10-year yield differential at -3bps.

- The bills strip is slightly stronger, with pricing flat to +2.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in August is given a 90% probability, with a cumulative 61bps of easing priced by year-end.

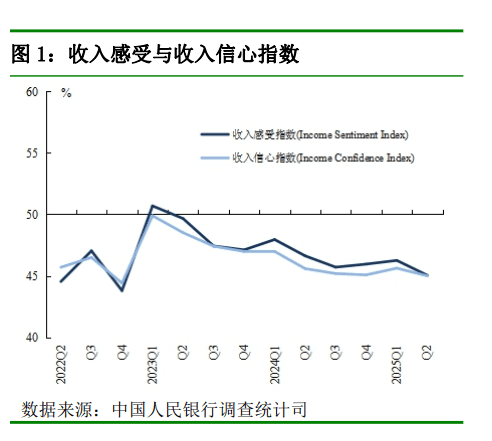

CHINA: PBOC Consumer Survey Shows Consumer Sentiment Poor

Jul-29 23:07

- In Q2 of 2025, the PBOC undertook a survey of households with 20,000 responders across 50 cities.

- The Income Perception Index fell 1.2% to 45.0% from the previous quarter with 20% of respondents believing their income had decreased, dragging the Income Confidence Index Lower.

Source: PBOC/MNI

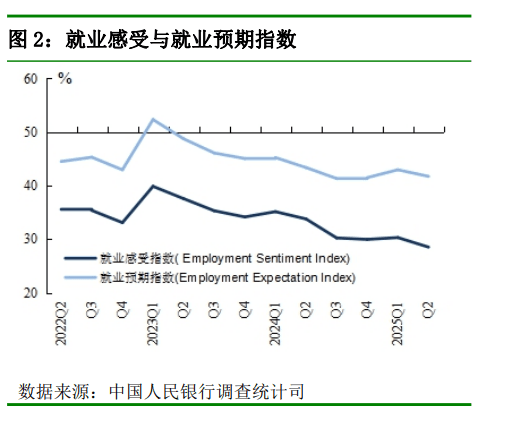

- The Employment Feeling Index and the Employment Expectation Index also softened. The employment sentiment index declined 1.8% to 28.5% with 53.7% of respondents describing the 'situation for finding a job' as severe.

Source: PBOC/MNI

- The Price Expectation Index is a measure for inflation expectations and relative to the prior quarter was down 0.7% as 9% of respondents expected prices to fall and 60.1% expected no change and 77.9% of respondents expect house prices to either fall or remain the same.

- Respondents consumption, savings and investment intentions saw a preference for more savings by 63% and those that prefer to invest more falling. Top investment preferences were non principal guaranteed bank wealth management products which are provide fixed income type returns with a return kicker.

- The survey points to a pessimistic consumer, likely underpinned by the ongoing deflationary pressures in the housing market.

BONDS: NZGBS: Richer, US Tsys Rally On Data & Strong Auction Ahead Of FOMC

Jul-29 23:01

In local morning trade, NZGBs are 3-4bps richer after UU tsy bulls ran with supportive data, solid auction results, and technical factors to post strong gains on the day.

- The combination of weaker-than-expected JOLTS, cooler inflation, and a good 7-year auction added to already growing bullish momentum.

- Swap rates are 2-4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing is little changed across meetings. 20bps of easing is priced for August, with a cumulative 35bps by November 2025.

- The local calendar will feature the release of ANZ business confidence for July today. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year, but still off December's 100.2. Rate cuts, which take time to be reflected in mortgage payments, have helped improve households' financial situations and reduced the time to buy component.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond. NZ Treasury also announced plans to sell NZ$1.8bn of bonds in August.