ASIA STOCKS: China's Rally Continues as Turnover Leaps

Data on turnover for the month for China stocks shows the key equity bourses are heading for a record month for turnover, as per BBG. The average turnover for August has topped the previous monthly record. Naturally this has seen the major bourses deliver strong returns as retail investor led momentum is growing rapidly.

- The Hang Seng delivered decent gains Friday of +0.63%, yet not enough to turn the weekly performance to positive as it remains down just over -0.70%. The onshore bourses however have had a different week with the CSI 300 up +0.58% today and +2.55% for the week, Shanghai up +016% today and +0.63% for the week, and Shenzhen rising +0.45% today and +2.06% over the last five days.

- The NIKKEI stumbled into the end of the week with a fall of -0.25% and is barely holding onto a weekly gain of +0.20%.

- In Taiwan, the TAIEX is up +0.48% and +2.47% for the week even as foreign flows turn negative.

- The KOSPI has had a weak end to the week, down -0.22%, yet remains up by +0.65% for the week as it heads into a big week of data next week.

- The FTSE Malay KLCI has had a tough period and is down -1.33% for the week, with falls of -0.66% today.

- The Jakarta Composite fell heavily today by -2.27%, which looks more technically driven as it hit new all time highs earlier this week.

- In Singapore, the Straits Times is up +0.37% for the week whilst the PSEi in the Philippines is down -1.8%

- India's NIFTY 50 is one of the worst regional performers down modestly today, but over -2.4% for the week.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Richer But Underperformed The $-Bloc

NZGBs closed near session bests, 3-4bps richer.

- Nevertheless, the local market underperformed its $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 4bps and 2bps wider, respectively.

- The ACGB market was buoyed today by lower-than-expected Q2 trimmed mean CPI, which should allow the RBA to ease 25bp on August 12. Trimmed mean rose 0.6% q/q to be up 2.7% y/y, a moderation from Q1’s 0.7% & 2.9%.

- The ANZ survey showed little change in business confidence and the outlook in July with the former rising 1.5 points to 47.8 but the latter falling 0.3 to 40.6. It signals that the recovery continues but at a gradual pace.

- Swap rates closed 1-3bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed with 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- Tomorrow, the local calendar will be empty ahead of ANZ July consumer confidence data on Friday. June building permits will also be printed on Friday

- Tomorrow, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond. NZ Treasury also announced plans to sell NZ$1.8bn of bonds in August.

FOREX: Asia FX Wrap - Price Action Suggests USD Correction Could Have More To Go

The BBDXY has had a range of 1207.77 - 1210.21 in the Asia-Pac session, it is currently trading around 1209, -0.05%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking has been seen. Monday’s US-EU trade deal was seen as a big loss for the European Union and this has provided the USD bounce with further tailwinds. There is lots of event risk coming up this week with FOMC tomorrow morning and NFP on Friday being chief among them. Price action does suggest this correction higher in the USD could have more to play out should the data allow.

- EUR/USD - Asian range 1.1546 - 1.1573, Asia is currently trading 1.1555. The pair saw some heavy selling putting in a top towards 1.1800 for now. The price looked a little stretched in the short term, and with the USD making a recovery the EUR is set for a correction of sorts. First support around the 1.1550 area then the more important 1.1350/1.1450 area where I would expect demand first up.

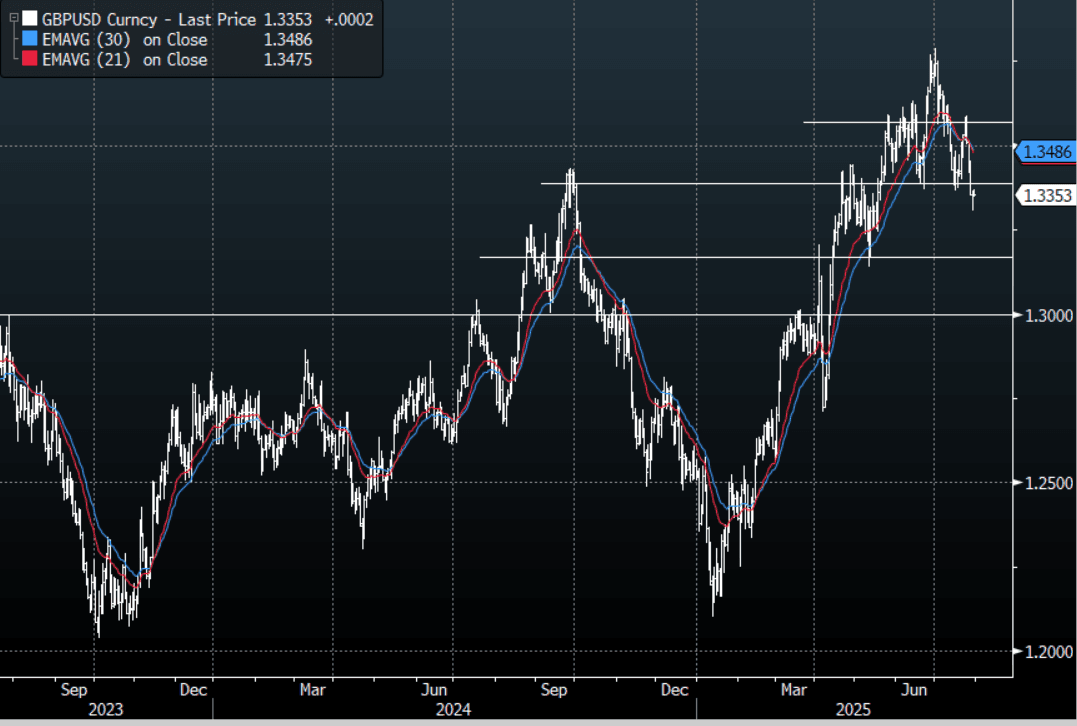

- GBP/USD - Asian range 1.3308 - 1.3364, Asia is currently dealing around 1.3355. This pair looks like it is now breaking lower indicating a deeper correction. Support seen now back towards 1.3100/1.3200 and look for supply now on bounces back towards 1.3500.

- USD/CNH - Asian range 7.1753 - 7.1827, the USD/CNY fix printed 7.1441, Asia is currently dealing around 7.1800. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3327, US 10-Year 4.326%, BBDXY 1209, Crude Oil $69.28

- Data/Events : France Consumer spending & GDP, Germany Retail Sales & GDP, Spain CPI, Italy GDP & Industrial Sales, EZ Consumer/Economic/Industrial Confidence & GDP

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: South Korea & China Firmer, Mixed Trends In SEA

Asia Pac markets are mixed in the first part of Wednesday trade. There have been lots of headlines around Tsunami warnings stretching across Asia Pac to the US, after a very large earthquake struck off the coast of Russia. Market impact in the equity space has been limited so far, with markets awaiting damage done in aftermath of any large Tsunami's that reach major coastlines. US equity futures are a little higher, but this comes ahead of the FOMC later, which is likely to keep interest light ahead of this risk event.

- Japan markets are a touch firmer, with the Topix up close to 0.30% in latest dealings, while the NKY 225 is around flat. Yen strengthened modestly on the tsunami headlines but has seen little follow through. Authorities have noted the tsunami risk could remain in place for the next day.

- China and Hong Kong markets are mixed. The HSI is off 0.40%, while the CSI 300 continues to rally, last up 0.50% to 4170/75. This is fresh highs back to Nov last year for the index. Positive tones around US-China trade talks are likely helping, while the government's efforts to remove excessive competition in certain sectors is also likely being seen as a positive for the profit outlook.

- South Korea's Kospi is up over 1% as the index extends its break above 3200. President Lee noted earlier that the government will become pragmatic and more market orientated, while also looking to abolish unnecessary regulations. Taiwan stocks are also higher, recovering most of yesterday's dip, the Taiex last near +0.90% firmer.

- In South East Asia, most markets are down, albeit modestly. Indonesia's JCI is down around 0.70%. Thailand's SET is the exception, up +0.35%. The MOF nudged up the 2025 GDP forecast, but lowered its inflation projection, which should be conducive for easier BoT policy settings.

- India stocks are a little higher, after underperforming recently. US President Trump stated yesterday that the country may see a 20-25% tariff rate, although this isn't final.