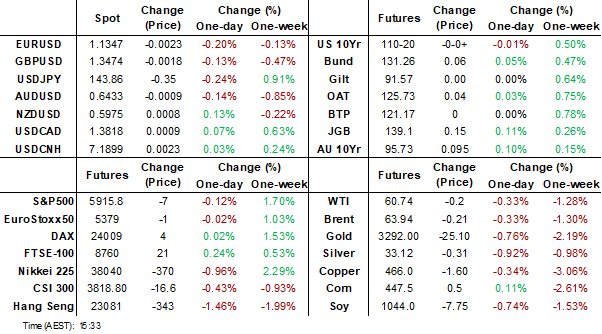

MNI EUROPEAN MARKETS ANALYSIS: US-China Talks 'A Bit Stalled'

- Aggregate USD and US Tsy yield moves were modest in Asia Pac on Friday. Earlier remarks by US Tsy Secretary Bessent stated that US-China trade talks have stalled somewhat.

- On the data front, Tokyo CPI was stronger than expected for the core measures. JGB futures are stronger, +12 compared to settlement levels. Australian retail sales fell modestly.

- Looking ahead, in the US we have Personal Spending, PCE, MNI Chicago PMI, U. of Mich Survey.

MARKETS

US TSYS: Asia Wrap - A Subdued Session

The TYM5 range has been 110-19+ to 110-23 during the Asia-Pacific session. It last changed hands at 110-21+, almost unchanged from the previous close.

- The US 2-year yield has edged higher, dealing around 3.945%, up 0.01 from its close.

- The US 10-year yield has extended higher, dealing around 4.42%, up 0.03 from its close.

- (Bloomberg) - “FED'S LOGAN SAYS STIMULATIVE FISCAL POLICY COULD BOOST DEMAND, IF HIGH INF. EXPECTATIONS GET ENTRENCHED, COSTLY TO FIX, IF BALANCE OF RISK SHIFTS, FED WELL PREPARED TO RESPOND.”

- Bloomberg - “ President Trump just sent out a long social media post making it clear his commitment to tariffs is as strong as ever following a court ruling that deemed the levies were illegal. That underscores that efforts to contest the measures via the courts may do more to boost uncertainty than to ameliorate the impact of the imposts, adding to pressure on the US dollar and equities.”

- The 10-year has come back down to test its support, likely aided by month-end rebalancing. Yields need to hold above 4.35% to continue to build for a move higher.

- Data/Events : Personal Spending, PCE, MNI Chicago PMI, U. of Mich Survey.

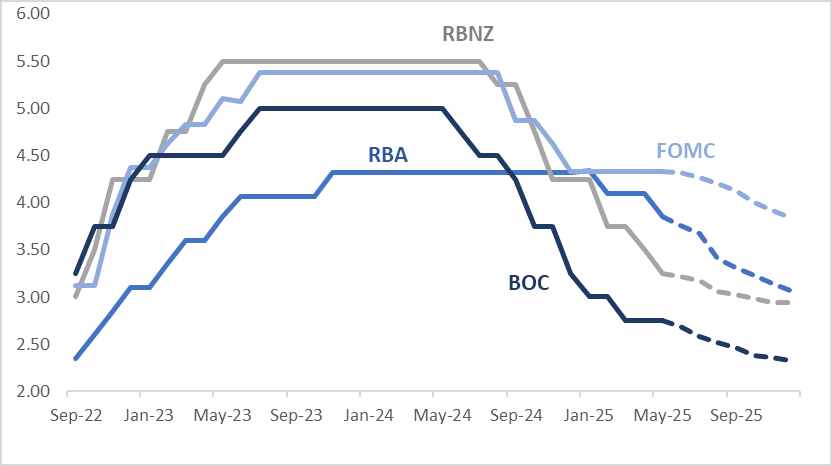

STIR: $-Bloc Markets Show Mixed Results Over Past Week, NZ The Outlier

Interest rate expectations across dollar-bloc economies were mixed through December 2025 over the past week, with New Zealand as the outlier. Canada and Australia saw the most significant shift, with around a 10bp softening in expected year-end rate. The US rate saw a 2bp softening, while New Zealand saw a 101bp firming.

- In New Zealand, the RBNZ cut rates 25bp to 3.25% following a vote that included an option to leave rates unchanged. The vote wasn’t unanimous, with one dissenter. There appears to be some disagreement over the impact of increased trade protectionism on NZ inflation. Despite this, the OCR path was revised down to show a trough 25bp below February’s at 2.85%, which signals that the impact of current global developments would require stimulatory policy by end-2025.

- In his first press conference as Governor, Hawkesby noted that this was the first vote on the direction of rates in two years—something that typically occurs at inflection points and highlights the current high level of uncertainty.

- In Australia, the April headline CPI was a touch above expectations at 2.4% y/y (2.3% was forecast). The trimmed mean rose 2.8% y/y (against a 2.7% prior outcome; there is no consensus estimate for this print).

- Across the $-bloc more broadly, markets appear content to consolidate recent repricing, which has largely stemmed uncertainty surrounding trade policy and generally solid economic data.

- The next key event for the region is the BoC’s June 4 policy meeting, where a 25bp rate cut is currently given a ~25% probability.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.81%, -52bps; Canada (BOC): 2.33%, -42bps; Australia (RBA): 3.07%, -78bps; and New Zealand (RBNZ): 2.94%, -31bps.

Figure 1: $-Bloc STIR (%)

Source: MNI – Market News / Bloomberg

JGBS: 20Y Leads Rally, Ueda: BoJ To Assess JGB Tapering Program

JGB futures are stronger, +12 compared to settlement levels.

- The 2-year bond auction showed mixed results today. The low price came in above expectations and an increase in the cover ratio. The auction tail, however, widened slightly compared to last month.

- (MNI) The BoJ is closely monitoring developments in the JGB market, including its overall functioning, amid growing concerns over worsening supply-demand dynamics, Governor Kazuo Ueda told lawmakers Friday. The BoJ will conduct an interim assessment of its JGB tapering program at the June 16-17 policy meeting based on feedback from financial institutions and recent market conditions, he said.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session.

- Bloomberg - “President Trump just sent out a long social media post making it clear his commitment to tariffs is as strong as ever following a court ruling that deemed the levies were illegal.”

- Cash JGBs are 1-4bps richer across benchmarks, with the 20-year leading. The benchmark 2-year yield is 1.2bps lower at 0.746% after today's supply.

- Swap rates are 2-3bps higher. Swap spreads are wider.

- On Monday, the local calendar will see Capital Spending, Company Profits/ Sales and Jibun Bank PMI Mfg.

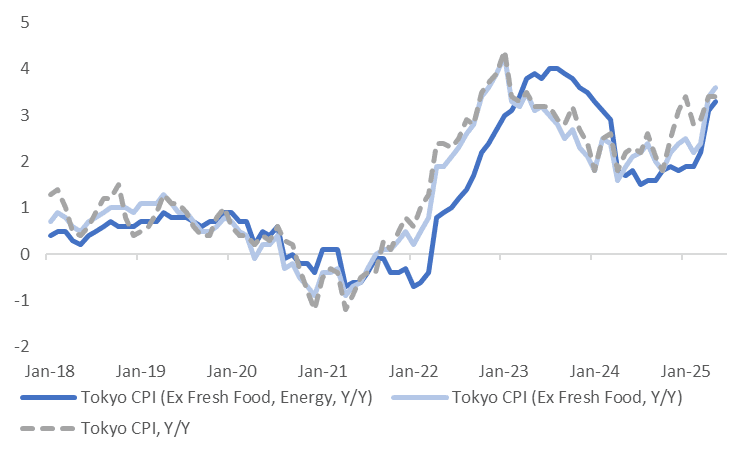

JAPAN DATA: Tokyo CPI Core Measures Continue To Firm

May Tokyo CPI saw core measures print firmer than expected. Headline rose 3.4% y/y, in line with consensus estimates, which was also the prior outcome (revised down from 3.5% originally reported). The ex fresh food measure rose 3.6%y/y (3.5% was the forecast and 3.4% prior). Ex fresh food and energy was 3.3%y/y, against a 3.2% forecast and 3.1% April print.

- The chart below plots the trend y/y outcomes for these three metrics. The continued upward momentum in the core outcomes should, at face value, add to BoJ confidence around achieving its inflation target sustainably. BoJ Governor Ueda continues to hint at progress on this front, but the inflation goal has not yet been reached.

- The core measure excluding fresh food and energy is now back to early 2024 levels in y/y terms.

- In m/m (seasonally adjusted terms), headline rose 0.3%, while the core measures were up 0.4-0.5%. Good prices rose 0.6% after a flat April. Services were up 0.2%, after a 0.3% gain in April. The measure which excludes all food and energy only rose 0.1%m/m (non seasonally adjusted), but still ticked up to 2.1%y/y (from 2.0%).

- By segment, drags came from fresh food (-2.5%m/m), but overall food was +0.3%m/m. Household goods eased -0.1%m/m, so did medical care. Utilities rose a solid 3.0%m/m, while entertainment was up 0.2%m/m after a strong gain in April. Utility bill relief is expected in Q3 of this year, while policy initiatives are also steeping up to curb food inflation.

- Y/Y momentum by segment was similar to April trends. Housing is the lower y/y pace at 1.5%, while other segments are either close to the 2% pace, or higher.

Fig 1: Tokyo CPI Y/Y - Core Measures Continue To Accelerate

Source: MNI - Market News/Bloomberg

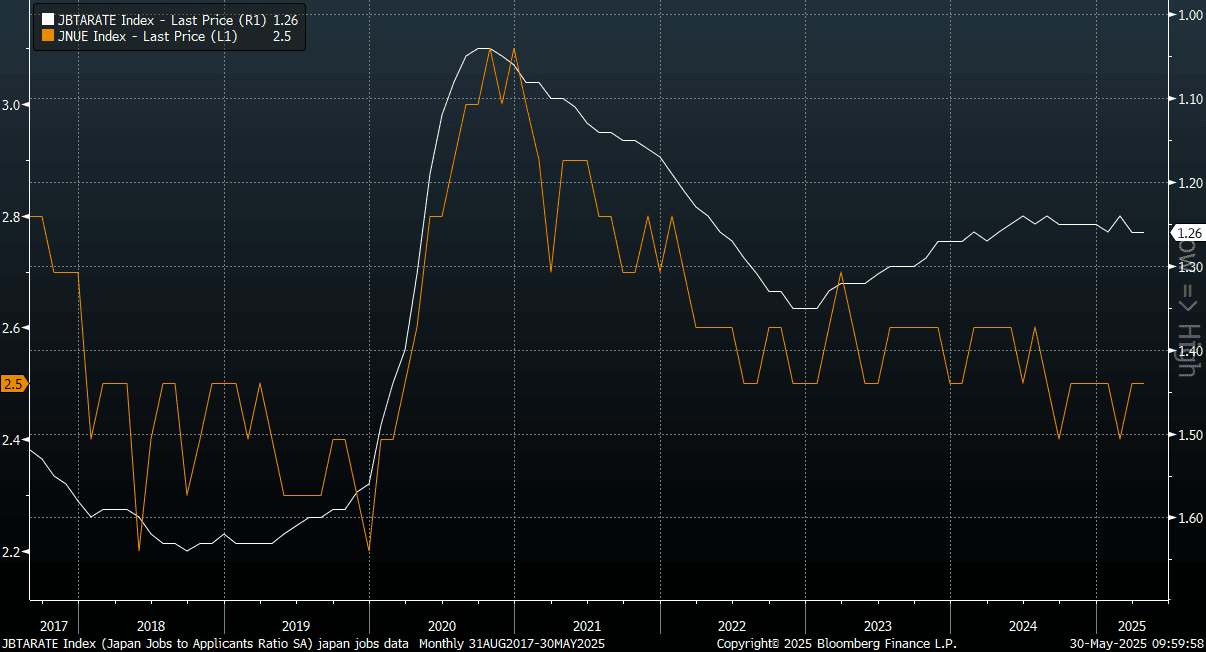

JAPAN DATA: April Data Still Points To Tight Labor Market

Japan's April jobless rate printed at 2.5%, in line with the consensus and the March outcome. It was the same story for the job-to-applicant ratio, which came in at 1.26. The chart below plots the two series, with the job-to-applicant ratio inverted on the chart (the white line). The jobless rate is still close to recent cycle lows and suggesting a tight labor market. The job to applicant ratio is well off late 2022 highs but is not showing trend weakness either.

- The number of people employed fell by a further 40k m/m, but this was at a reduced pace of -80k seen in March. The participation rate edged up to 63.7% from 63.3%.

Fig 1: Japan Jobless Rate & Job-To-Applicant Ratio

AUSSIE BONDS: Richer & Near Bests, Tariff HLs In Focus, Q1 GDP Wednesday

ACGBs (YM +9.0 & XM +10.0) are hovering near Sydney session highs.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session.

- Bloomberg - “President Trump just sent out a long social media post making it clear his commitment to tariffs is as strong as ever following a court ruling that deemed the levies were illegal. That underscores that efforts to contest the measures via the courts may do more to boost uncertainty than to ameliorate the impact of the imposts, adding to pressure on the US dollar and equities.”

- Cash ACGBs are 9bps richer, with the AU-US 10-year yield differential at -14bps.

- The bills strip has bull-flattened, with pricing +2 to +10.

- RBA-dated OIS pricing is 3-10bps softer across meetings today, with early 2026 leading. A 25bp rate cut in July is given a 69% probability, with a cumulative 76bps of easing priced by year-end.

- On Monday, the local calendar will see Cotality Home Value, S&P Global PMI Mfg, MI Inflation and Job Advertisements data. Q1 GDP prints on Wednesday, with market consensus at +0.4% q/q 1.5% y/y.

- Next week, the AOFM plans to sell A$1200mn of the 3.75% 21 April 2037 bond on Tuesday and A$800mn of the 1.50% 21 June 2031 bond on Friday.

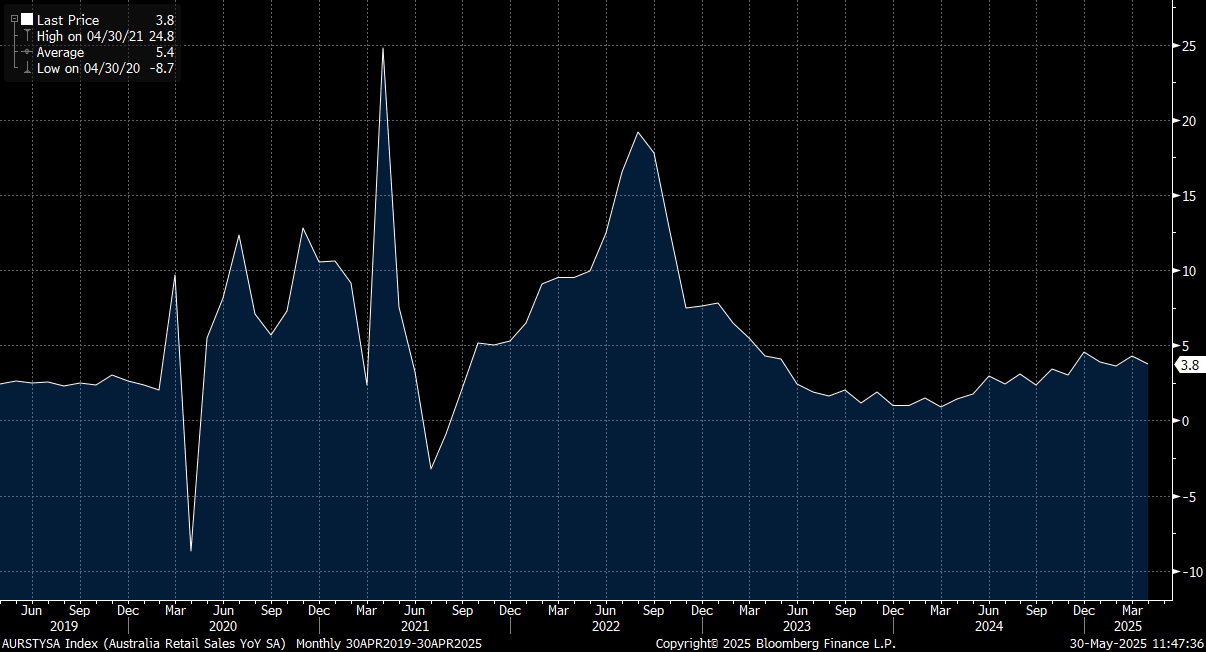

AUSTRALIA DATA: Retail Sales Surprise Lower, Weather May Have Influenced

Australian April retail sales were weaker than forecast, falling 0.1%m/m, against a +0.3% forecast, which was also the March outcome. Data on building approvals was also weaker than forecast, down 5.7%m/m, against a 3.0% forecast rise. The prior month was -7.1%m/m, slightly better than originally reported. Private sector home approvals were better at +3.1%m/m (versus -1.9%m/m in March). Private sector credit was +0.7%m/m, better than the 0.5% forecast.

- For retail sales, the industry break down saw food off 0.3%m/m, while apparel and department stores were both down 2.5% in the month. This follows falls for these segments in March as well.

- Positives were in terms of cafes, up +1.1%m/m and household goods, +0.6%m/m. Both these segments were down in March in m/m terms.

- The ABS notes: "‘Falls were partly offset by a bounce-back in Queensland as businesses recovered from the negative impacts of ex-Tropical Cyclone Alfred last month.’" It added: "Clothing retailers told us that the warmer-than-usual weather for an April month saw people holding off on buying clothing items, especially new winter season stock,’ Mr Ewing said."

- Outside of the rise in spending in QLD, we had a modest rise in spending in WA, both all other states and territories saw falls, speaking to a generally soft underlying result.

- In y/y spending was 3.8%, see the chart below. In nominal terms spending trends have moves sideways since the start of the year, as fiscal incentives from H2 2024 have waned.

Fig 1: Australia Retail Sales Y/Y

Source: MNI - Market News/Bloomberg

BONDS: NZGBS: Bull-Flattener To End a Hawkish Week

NZGBs closed showing a bull-flattener, with benchmark yields just off session bests, 2-7bps lower.

- Swap rates closed 4-8bps lower, with implied short-end swap spreads tighter.

- Nevertheless, the week will be noted for the fact that, as Governor Hawkesby remarked, Wednesday’s policy meeting was the first vote on the direction of rates in two years—something that typically occurs at inflection points and highlights the current high level of uncertainty.

- “The Reserve Bank of New Zealand needs more time to assess the impact of global trade turmoil on the local economy before deciding on the appropriate path for the Official Cash Rate, Assistant Governor Karen Silk said.” (per BBG)

- Interest rate expectations across dollar-bloc economies were mixed through December 2025 over the past week, with New Zealand as the outlier. Canada and Australia saw the most significant dovish shift, with around a 10bp softening in expected year-end rate. The US rate saw a 2bp softening, while New Zealand saw a 11bp firming.

- The local market will be closed on Monday for King’s Birthday.

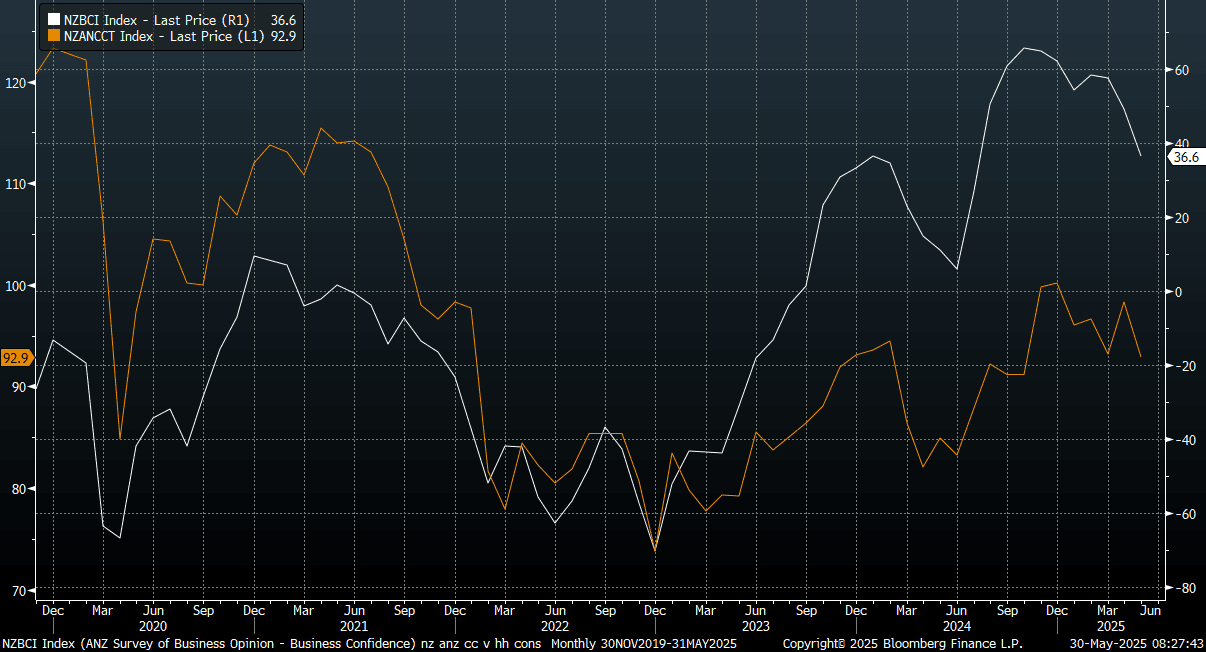

NEW ZEALAND: ANZ Consumer Confidence Back Down In May, Unwinds April Gains

New Zealand's ANZ consumer confidence survey fell 5.5% in May, completely reversing April's gain. This puts the index back just under 93.0. This is lows back to October last year. The general improving trend in consumer seen up to end 2024 has stalled in the first half of 2025.

- In terms of the detail, most sub components fell. Family finances for the year ahead eased to -16 from -13, whilst for the year ahead were at +12 from +23 in April.

- Views on the economy were also down, -20 for the year ahead, -1 for 5yrs ahead (from +9 in April).

- Today's result follows yesterday's softer business confidence read from ANZ, the chart below plots the two series. Business confidence (the white line) is coming off higher levels but has generally faltered since late last year as well.

- This underscores the RBNZ cut this week, with potentially more work to do to aid the growth recovery, albeit with one eye on inflation and inflation expectations.

Fig 1: ANZ Consumer & Business Confidence Measures Softening

Source: ANZ/MNI - Market News/Bloomberg

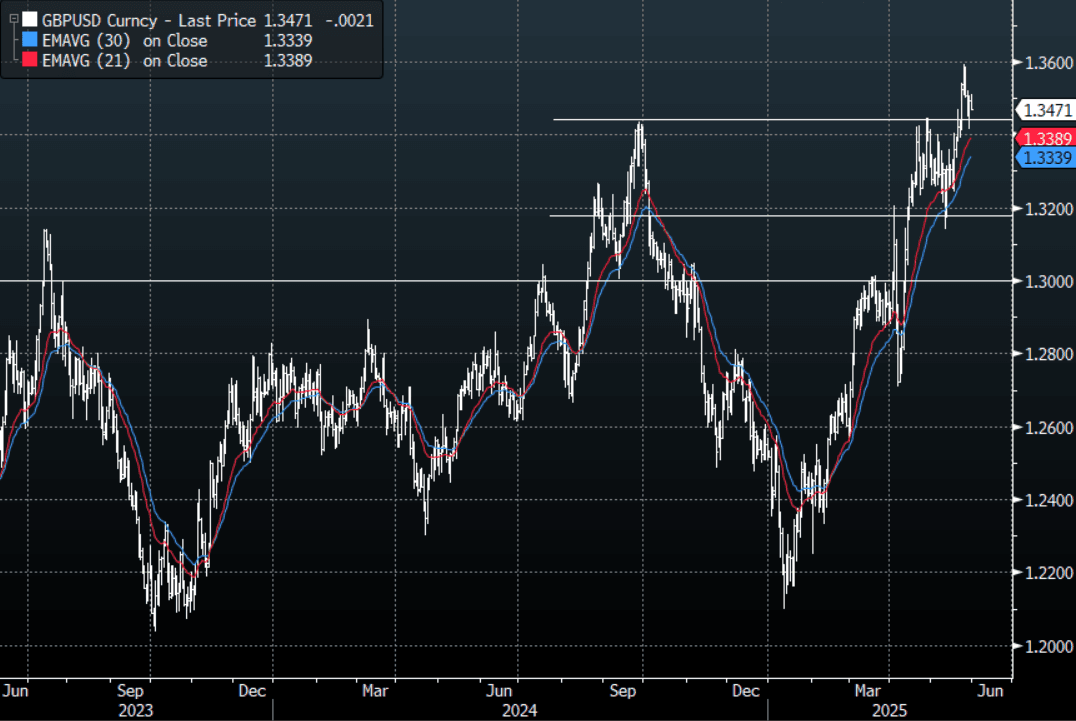

FOREX: Asia FX Wrap - Market Wants To Be Short USD's

The BBDXY has had a range of 1213.32 - 1216.38 in the Asia-Pac session, it is currently trading around 1216. “The BOE’s Andrew Bailey urged closer EU trade ties to improve growth and “minimize negative effects” of Brexit”(BBG).“U.S. officials are weighing their options should they need to find a new legal authority to impose the president's steep tariffs, which he argues will help rebalance trade in America's favor." WSJ

- EUR/USD - Asian range 1.1350 - 1.1390, Asia is currently trading 1.1350. EUR has drifted lower during the Asian session as US stock futures trade weaker. Dips should continue to find support, the demand back towards 1.1200 proved to be solid yesterday.

- GBP/USD - Asian range 1.3471 - 1.3511, Asia is currently dealing around 1.3470. The GBP could not hold above the pivotal 1.3500 area for now. Look for an opportunity to buy again back towards the 13300/3400 area.

- USD/CNH - Asian range 7.1812 - 7.1907, the USD/CNY fix printed 7.1848. Asia is currently dealing around 7.1870. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX -0.24%, Gold $3295, US 10-Year 4.416%, BBDXY 12166, Crude oil $60.60

Data/Events : Ger Retail Sales & CPI, Spain CPI, Italy GDP & CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

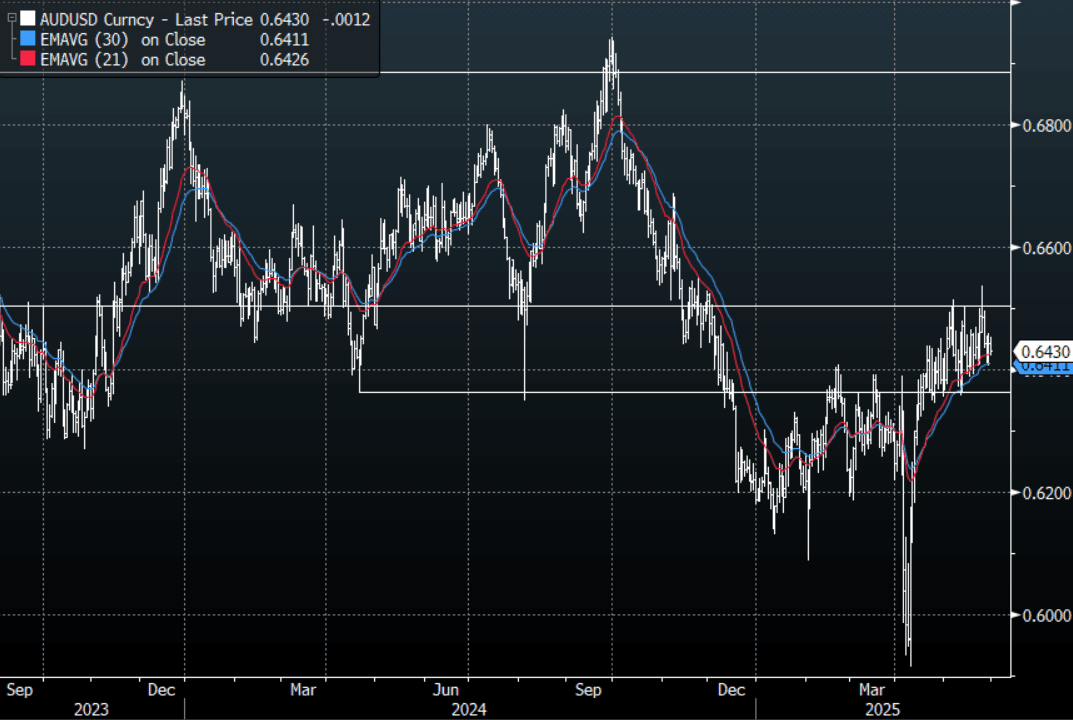

AUD: Asia Wrap - Lower Retail Print Sees The Aud Dip

The AUD/USD has had a range of 0.6424 - 0.6453 in the Asia- Pac session, it is currently trading around 0.6430. The AUD has underperformed across the board today after some weaker data.

- AUSTRALIA DATA: Retail Sales Surprise Lower, Weather May Have Influenced: Australian April retail sales were weaker than forecast, falling 0.1%m/m, against a +0.3% forecast, which was also the March outcome.

- Smooth Digestion Of Mar-36 Supply But Lower Demand: The latest ACGB Mar-36 auction saw adequate demand, with the weighted average yield coming in 0.39bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions.

- The AUD sold off on the surprise in the lower retails sales print, with the USD back under pressure the crosses still look a better way to express AUD weakness.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6555(AUD389m). Upcoming Close Strikes : 0.6400(AUD 786m June 2)

AUD/JPY - Today's range 92.40 - 92.99, it is trading currently around 92.50. Price action yesterday showed the market was short, but was also very quick to re-instate positions. Range looks 92.00 - 94.00 for now, a sustained break below 91.50/92.00 needed to bring focus back to towards the lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

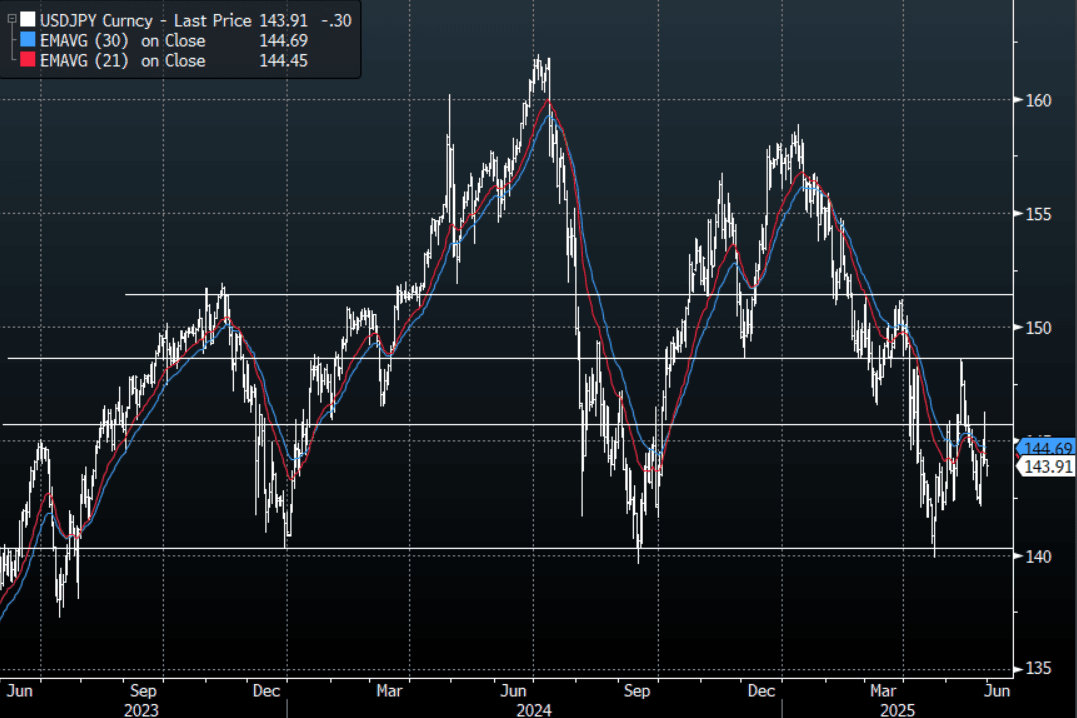

JPY: Asia Wrap - Risk Drifting Lower, The JPY Benefits

The Asia-Pac USD/JPY range has been 143.44 - 144.21, Asia is currently trading around 143.90. USD/JPY has remained offered in our session as the market's focus returns to selling the USD once more as US Stocks drift lower.

- (JAPAN DATA) Tokyo CPI Core Measures Continue To Firm : May Tokyo CPI saw core measures print firmer than expected. Headline rose 3.4% y/y, in line with consensus estimates, which was also the prior outcome (revised down from 3.5% originally reported).

- The continued upward momentum in the core outcomes should, at face value, add to BoJ confidence around achieving its inflation target sustainably. BoJ Governor Ueda continues to hint at progress on this front, but the inflation goal has not yet been reached.

- UEDA: “SET SHORT-TERM POLICY RATE TO HIT INFLATION TARGET, UNREALIZED JGB LOSSES WON'T AFFECT REVENUE" - BBG

- US Stocks came under some pressure as the WSJ reports Trump is actively looking for alternative ways to impose his agenda should the appeal fail, this saw some renewed demand for safe currencies like the JPY.

- The market was very quick to reinstate short USD/JPY positions overnight as the “sell America” trade gains in popularity.

- The market seems very confident of a move lower in USD/JPY but with positioning quite large now the price action of the last couple of days highlights the increased risks of pullbacks. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action. The next pivotal trigger points look to be below 140.00 on the downside and above 146.50 on the topside.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.00($3.39b May 30), 140.00($2.78b May 30). Upcoming Close Strikes : 147.50($475m June 2), 147.75($476m June 3)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

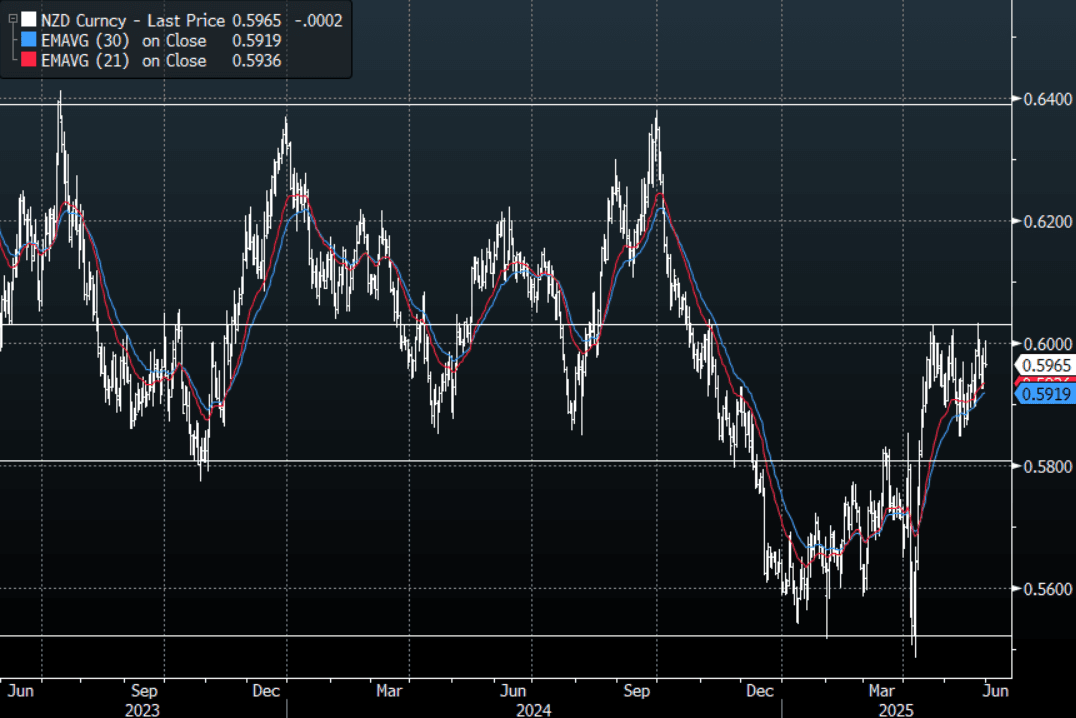

NZD: Asia Wrap - NZD Holding Up, Eyes 0.6000 Again

The NZD/USD had a range of 0.5960 - 0.5990 in the Asia-Pac session, going into the London open trading around 0.5965. The NZD has consolidated in a tight range in our session. US Stocks came under some pressure as the WSJ reports Trump is actively looking for alternative ways to impose his agenda should the appeal fail.

- “U.S. officials are weighing their options should they need to find a new legal authority to impose the president's steep tariffs, which he argues will help rebalance trade in America's favor." WSJ

- "TRUMP TEAM MULLS STOPGAP TARIFFS UNDER TRADE ACT PROVISION, TRUMP ADMIN PLAN ALLOWS FOR TARIFFS UP TO 15% FOR 150 DAYS: WSJ" - BBG

- The NZD continues to trade in a 0.5850/0.6050 range, the hawkish slant from the RBNZ has probably seen a good portion of the new shorts added last week by leveraged accounts pared back.

- The support back towards 0.5800/50 has held very well, and while this continues to hold expect buyers to be around on dips. A break above 0.6050 is needed to provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6100(NZD375m June 3), 0.5900(NZD401m June 4)

AUD/NZD range for the session has been 1.0760 - 1.0801, currently trading 1.0775. A top looks in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ this week and AUD/NZD should now see supply on bounces. The sell zone is back towards 1.0825/50 with the first target being around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Stocks Lower on Ongoing Tariff Uncertainty

Major bourses across the region fell today as uncertainty remains over tariffs. The on again off again nature of the current situation does not bode well for risk appetite and investors drove equities lower today . US Treasury Secretary Bessent described talks between China and the US as 'stalled' weighing on sentiment.

- China's Hang Seng fell -1.48% today and is on track for a five day decline of -1.60%; CSI 300 is down -0.33% and -0.94% for the week, Shanghai down -0.31% yet remains just in positive territory, up +0.14% and Shenzhen is down -0.94% leaving it just +0.05% higher for the week.

- The KOSPI has had a strong week on the back of a cut from the Central Bank and is up +3.8%, yet down just over 1% today.

- The FTSE Malay KLCI is down moderately today and down -1.10% for the week.

- The Jakarta Composite is closed today but up over +0.47% for the week.

- FTSE Straits Times in Singapore is flat today and +0.85% higher today, whilst PSEi in the Philippines is lower today by -0.65% and similar levels for the week.

- The NIFTY 50 has had a slow week, down just -0.15% today and -0.20% for the week.

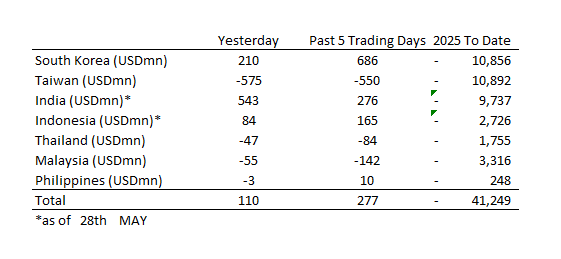

ASIA STOCKS: Big Flows for South Korea and India

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows, with Taiwan the latest to experience a significant outflow yesterday.

- South Korea: Recorded inflows of +$210m yesterday, bringing the 5-day total to +$686m. 2025 to date flows are -$10,856. The 5-day average is +$137m, the 20-day average is +$91m and the 100-day average of -$107m.

- Taiwan: Had outflows of -$575m as yesterday, with total outflows of -$550m over the past 5 days. YTD flows are negative at -$10,892. The 5-day average is -$110m, the 20-day average of +$378m and the 100-day average of -$110m.

- India: Had inflows of +$543m as of the 28th, with total inflows of +$276m over the past 5 days. YTD flows are negative -$9,737m. The 5-day average is +$55m, the 20-day average of +$141m and the 100-day average of -$107m.

- Indonesia: Had inflows of +$84m as of the 28th, with total inflows of +$165m over the prior five days. YTD flows are negative -$2,726m. The 5-day average is +$33m, the 20-day average +$17m and the 100-day average -$29m.

- Thailand: Recorded outflows of -$47m as of yesterday, outflows totaling -$84m over the past 5 days. YTD flows are negative at -$1,755m. The 5-day average is -$17m, the 20-day average of -$2m and the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$55m as of yesterday, totaling -$142m over the past 5 days. YTD flows are negative at -$3,316m. The 5-day average is -$33m, the 20-day average of +$18m and the 100-day average of -$23m.

- Philippines: Saw outflows of -$3m yesterday, with net inflows of +$10m over the past 5 days. YTD flows are negative at -$248m. The 5-day average is +$2m, the 20-day average of +$2m the 100-day average of -$3m.

OIL: Declines Continue In Asia Trading

- Oil's overnight fall continued in the Asia trading day with WTI and Brent lower

- WTI opened at US$60.94 bbl and moved steadily lower to $60.64, a fall of -0.45%.

- The places WTI on course for a weekly decline of nearly -1.5% and would represent a second week in a row of similar falls.

- Brent opened at US$64.11 bbl and moved steadily lower to $63.82, a fall of -0.50%

- The places WTI on course for a weekly decline of nearly -1.5% also and would represent a second week in a row of similar falls.

- Kazakhstan says it cannot cut oil production and hopes to increase output beyond planned levels later this year, despite its commitments to OPEC+. The country's Energy Minister stated that Kazakhstan has minimal impact on production output, and has notified OPEC of its position.

- In an OPEC+ meeting this Saturday, the market expects announcements around an increase in supply by June of a further 1.3m bbl per day from July onwards.

- It remains unclear why the sudden desire to increase production at a time when global growth prospects are challenged. The move no doubt will please President Trump who is determined to see lower prices.

- Wildfires are threatening about 5% of Canada's crude output as a blaze in Alberta's oil sands region spreads and approaches major production sites.

Gold Gives Back Overnight Gains

- Gold had a volatile nights as markets adjusted to the tariff headlines post the court ruling and has given back some of the overnight gains.

- Gold opened today at $3,317.94, and traded lower throughout the day to reach $3,293.01. A fall of -0.75%

- The move lower sees gold approaching the 20-day moving average of $3,288.38.

- For the week gold has fallen -1.95%

- The move higher was underpinned by a move lower in the USD as strategists suggested that there are plenty of alternative routes the president can take to pursue his trade agenda.

- Gold ETFs have experienced a multi week period of outflows, the first in some time and the renewed uncertainty may predicate a return to buying for some investors.

- Burkina Faso's industrial gold mining is set to increase this year with a project by Soleil Resources International Ltd. reaching full production and a new mine by West African Resources Ltd. starting output later this year. Production by the country's large-scale operations will increase by 4% to 55.7 tons this year, a

INDIA: Country wrap: RBI to Cut Next Week

- India’s transition to a delta-based measure of open interest from notional is positive for exchanges, clearing members like Nuvama Wealth and proprietary traders, according to Jefferies. “As planned, SEBI to transition to Delta-based OI limits, new caps on market-wide position limits and other initiatives to better manage the F&O market,” analyst Prakhar Sharma wrote in a note (source BBG)

- RBI Preview: The Reserve Bank of India meets on June 06 to decide the next monetary policy move. At time of writing there is a heavy consensus for a further cut. At the last meeting in April, the RBI cut rates and signalled that more cuts were ahead, as it seeks to boost the sluggish economy in the face of fresh US tariffs. Since that meeting, economic data has shown resilience with PMI's rising very strongly, exports surprising to the upside, industrial production resilient all against a backdrop of moderating inflation. During the last month the RBI has repeatedly provided strong liquidity support to markets, a sign that the transmission mechanism for monetary policy may not be as effective as required. Market consensus is very strongly for a cut with all economists surveyed on BBG advocating a cut and -23bps priced in by the bond market. We align our thinking with consensus and expect a cut and for now and are focused on the RBI liquidity injections in the near term. (source MNI Market News)

- The NIFTY 50 has had a slow week, down just -0.15% today and -0.20% for the week.

- The rupee is stronger today by +0.16% yet down for the week by -0.20%

- Bonds have had a quiet week, ending where they started for the 10YR at 6.25%

CHINA: Country Wrap: AI Patents 40% of Global

- China has built a relatively comprehensive artificial intelligence (AI) industrial system, with the value of its core sector nearing 600 billion yuan (about 83.45 billion U.S. dollars) by April 2025, the National Development and Reform Commission (NDRC) announced on Thursday. These details were included in an introduction to China's AI development delivered by NDRC official Huang Ru at the China-Shanghai Cooperation Organization (SCO) Artificial Intelligence Cooperation Forum, which was held in north China's Tianjin Municipality on May 29. Huang highlighted that China's AI patent applications have surpassed 1.5 million in number, accounting for nearly 40 percent of the global total. (source Xinhua)

- China may boost its pledged supplementary lending (PSL) facility and offer interest subsidies in the second quarter to help stabilize trade amid U.S. tariff pressure, Securities Times reports, citing analysts. The tools are also expected to help China expand investment, report said, without giving details such as the amount of the loans. The PSL is a monetary policy tool offered by the Chinese central bank to provide low-cost, long-term funding to policy banks, which fund government-prioritized sectors. The policy support loans are seen as “quasi-fiscal” stimulus, to support targeted sectors without broad-based monetary easing (source Securities Times)

- China's Hang Seng fell -1.48% today and is on track for a five day decline of -1.60%; CSI 300 is down -0.33% and -0.94% for the week, Shanghai down -0.31% yet remains just in positive territory, up +0.14% and Shenzhen is down -0.94% leaving it just +0.05% higher for the week.

- Yuan Reference Rate at 7.1848 Per USD; Estimate 7.1708

- The 10YR CGB is lower by -1.5bp, retracing yesterday's sell off. The 10YR CGB has traded in a 1.62-1.71% yield range all month as the PBOC maintains liquidity with modest daily injections most days.

SOUTH KOREA: Country Wrap: Industrial Production Rises in April

- South Korea's tax revenue rose by 16.6 trillion won (US$12.1 billion) in the first four months of this year from a year earlier, driven largely by a surge in corporate tax collection, the finance ministry said Friday. The government collected 142.2 trillion won in taxes during the January-April period, up from 125.6 trillion won in the same period last year, according to data from the Ministry of Economy and Finance. The increase was mainly attributed to higher corporate tax revenue, which amounted to 35.8 trillion won during the four-month period, up 57 percent from the same period the previous year. (source Yonhap)

- South Korea's Industrial Production YoY for April rises +4.9%, beating expectations of a rise in +4.0%. March's result however was revised down from +5.3% to +4.4%.

- The MoM figure was less than flattering with a decline of -0.9% following March's expansion of +2.9%. The Cyclical Leading Index rose +0.3% MoM. (source MNI and Korea Times)

- The KOSPI has had a strong week on the back of a cut from the Central Bank and is up +3.8%, yet down just over 1% today.

- The won is down today by -0.5% at 1,379.15 and 1% lower for the week.

- Bonds have had an up and down week and are ending up in line with where it started for the 10YR at 2.77%

ASIA FX: Mixed Trends, USD/KRW Higher, PHP & THB Modestly Lower

Asian currencies have seen mixed trends so far in Friday trade, in NEA we are seeing some USD gains, albeit mostly versus KRW. In SEA, the bias is more towards USD weakness, although a chunk of this reflects catch up to USD weakness post Thursday onshore closes in these markets.

- USD/CNH is around 7.1900 in latest dealings, slightly up on end Thursday levels. The USD/CNY fixing was lower but comfortably above market estimates. Headlines crossed earlier from a Fox News interview with US Tsy Secretary Bessent, in which described US-China talks as having stalled somewhat. he is pushing for a call between China President Xi and US President Trump.

- Spot USD/KRW is around 0.60% higher, last near 1379/80. Month end may be a factor, while the Kospi is also giving back some of its recent outperformance, last down around 1% and back under the 2700 level. For spot USD/KRW we found selling interest above 1385 yesterday.

- Taiwan markets are shut today.

- In SEA, the early bias was for weaker USD levels, but we are mostly higher now. USD/MYR is back to unchanged last near 4.2435.

- USD/THB got under 32.50, but is back to the 32.65/70 region. IP data was better than forecast, we wait for trade data later.

- USD/PHP was last at 55.60/65. The April trade deficit was narrower than forecast, boosted by better exports and lower imports.

- Indonesian markets are closed today.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 30/05/2025 | 0600/0800 | *** | GDP | |

| 30/05/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/05/2025 | 0600/0800 | ** | Retail Sales | |

| 30/05/2025 | 0630/0730 | DMO to release FQ2 (Jul-Sep) issuance ops calendar | ||

| 30/05/2025 | 0700/0900 | *** | HICP (p) | |

| 30/05/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/05/2025 | 0800/1000 | ** | M3 | |

| 30/05/2025 | 0800/1000 | *** | GDP (f) | |

| 30/05/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/05/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/05/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/05/2025 | 0900/1100 | *** | HICP (p) | |

| 30/05/2025 | 1000/1200 | ** | PPI | |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 30/05/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 30/05/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 30/05/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 30/05/2025 | 2045/1645 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/1930 | Chicago Fed's Austan Goolsbee | ||

| 31/05/2025 | 0130/0930 | *** | CFLP Manufacturing PMI | |

| 31/05/2025 | 0130/0930 | ** | CFLP Non-Manufacturing PMI |