AUD: Asia Wrap - Lower Retail Print Sees The Aud Dip

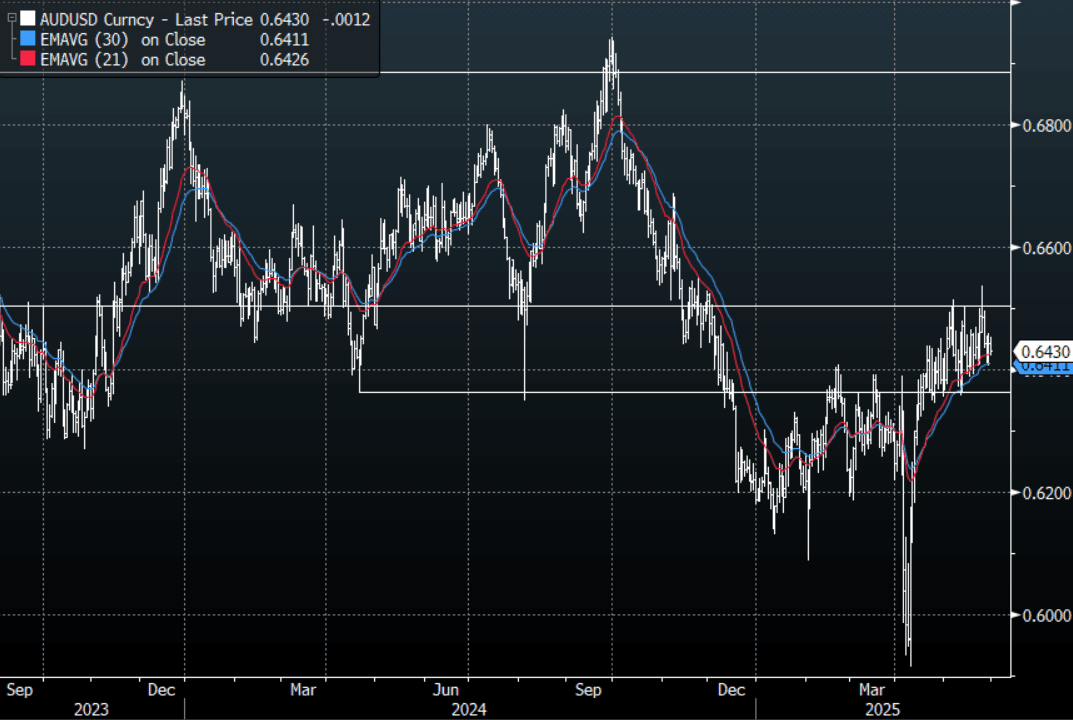

The AUD/USD has had a range of 0.6424 - 0.6453 in the Asia- Pac session, it is currently trading around 0.6430. The AUD has underperformed across the board today after some weaker data.

- AUSTRALIA DATA: Retail Sales Surprise Lower, Weather May Have Influenced: Australian April retail sales were weaker than forecast, falling 0.1%m/m, against a +0.3% forecast, which was also the March outcome.

- Smooth Digestion Of Mar-36 Supply But Lower Demand: The latest ACGB Mar-36 auction saw adequate demand, with the weighted average yield coming in 0.39bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions.

- The AUD sold off on the surprise in the lower retails sales print, with the USD back under pressure the crosses still look a better way to express AUD weakness.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6555(AUD389m). Upcoming Close Strikes : 0.6400(AUD 786m June 2)

AUD/JPY - Today's range 92.40 - 92.99, it is trading currently around 92.50. Price action yesterday showed the market was short, but was also very quick to re-instate positions. Range looks 92.00 - 94.00 for now, a sustained break below 91.50/92.00 needed to bring focus back to towards the lows again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: A$ Outperforms Following Slightly Higher Q1 CPI Print, US GDP Out Later

AUDUSD jumped on the moderately higher-than-expected Q1 CPI data that included upward revisions to Q4 and Aussie is now outperforming the rest of the G10, despite mixed equities and lower commodity prices. It reached a low of 0.6379 before the data and then jumped to 0.6407 following the print but has struggled to hold the break above 64c and is currently around 0.6398 to be up 0.2% today. The USD index is little changed.

- AUDNZD has trended higher through most of the session and is now +0.3% to 1.0792, close to today’s peak.

- AUDJPY is up 0.2% to 91.09, close to the intraday high of 91.22. AUDEUR rose to 0.5634 following Australia’s inflation data and is now +0.3% to 0.5624. AUDGBP is also 0.3% higher at 0.4777 off the peak of 0.4781.

- Equities are mixed with the ASX up 0.2% but Hang Seng down 0.4% and S&P e-mini -0.5%. Oil continues to sell off with WTI -0.9% to $59.90. Copper is down 1.2% and iron ore is around $98/t.

- Later US Q1 GDP & employment costs, March core PCE prices, April MNI Chicago PMI & ADP employment print. Also preliminary April euro area CPI, Q1 GDP including Germany, France & Italy, German March retail sales & unemployment are released. BoE’s Lombardelli speaks.

JGBS: Slightly Mixed After Domestic Data Drop

At the Tokyo lunch break, JGB futures are little changed, +1 compared to the settlement levels.

- March preliminary industrial production was below market forecasts, down 1.1%m/m, versus -0.4% expected. In y/y terms, we came in at -0.3% versus 0.8% forecast (0.1% was the prior outcome). The y/y trend hasn't been able to see much upside traction for a number of years now. The current y/y pace is slightly above averages for 2023/24, but only marginally.

- Retail sales were slightly below market forecasts. We were -1.2%m/m, against a 0.7% forecast, with Feb revised to a 0.4% gain. In y/y terms, we rose 3.1%, against a 3.5% forecast and 1.3% in Feb. The y/y trend is around mid-range of the past 12 months, as we have oscillated between flat to +5%. The authorities remain focused on driving sustained/positive real household spending growth, aided by positive real wages growth. The next round of labour earnings data is due next Friday.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are mixed, with benchmark yields 1bp lower (5-year) to 1bp higher (30-year). The benchmark 10-year yield is 0.3bp higher at 1.321% versus the cycle high of 1.596%.

- Swap rates are 1-2bps lower. Swap spreads are mixed.

AUSTRALIA DATA: Monthly CPI Inflation Stabilises At End Of Quarter

Monthly trimmed mean and headline data for March were unchanged from February at 2.7% y/y and 2.4% respectively. The latter was higher-than-forecast. The trimmed mean has been around 2.7% for four consecutive months now, which is consistent with the RBA’s projection that it could remain around this rate and not make any further progress towards the 2.5%-target mid-point in 2025. Given global developments though, the outlook remains highly uncertain.

Australia CPI trimmed mean vs services y/y%

- March seasonally adjusted headline CPI rose 0.5% m/m to be steady at 2.4% y/y, while excluding volatile items & holiday travel also rose 0.5% m/m but eased 0.1pp to 2.6% y/y, also close to the mid-point of the 2-3% target band. However, 3-month annualised momentum has picked up to 4.0% for both.

Australia CPI headline vs ex volatile items 3-mth annualised momentum % sa

Source: MNI - Market News/ABS

- March services inflation rose to 3.9% y/y from 3.6%, while non-tradeables were steady at 3.2%. Goods moderated 0.2pp to 1.1% y/y, lowest since November, and tradeables were unchanged at 0.9%.

- The ABS observes that food & non-alcoholic beverages (+3.4%), alcohol & tobacco (+6.7%) and housing (+1.8%) made the largest contributions to annual headline inflation in March.