AUD: GBP/AUD-Tops Out Above 1.9800 And Resumes Move Lower, AUD Outperforming

The GBP/AUD range overnight was 1.9608 - 1.9729, Asia is trading around {GBPAUD Curncy}. The pair st...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: Gas Prices Rise On Colder Weather & Falling Inventories

Natural gas prices started the week higher on wintery weather but are on track to finish December down. Europe rose 2.0% to EUR 28.655 reaching EUR 28.90 early in the session due to forecasts of a cold snap in the north-west. Prices are still down slightly on the month as mild weather and Ukraine peace talks weighed.

- Russia has demanded that an agreement include an easing of sanctions which would result in higher global gas supplies. However, talks are progressing slowly on a deal and Russia is stating that it will now appraise its negotiating position after it claimed that President Putin’s Novgorod residence was attacked by Ukrainian drones, which President Zelenskyy has denied.

- Cold weather is forecast to continue in northwestern Europe until mid-January, according to Bloomberg, which is likely to drive further inventory drawdowns. Storage was 63.8% full on Sunday after starting the month around 75%.

- US gas prices rose on forecasts for colder-than-average weather across the Northeast in the first week of January but the second week should see higher temperatures.

- They were also supported by a larger-than-normal inventory drawdown of 166bcf compared to 110bcf 5-year average, reported by the EIA for the week ending 19 December. Storage is 0.7% below this average, according to Bloomberg. US lower-48 production rose 6.8% y/y on Monday with demand up 34.6% y/y.

- The January Henry Hub contract rallied 6.8% to $4.663 into its 29 December expiry but was down 3.9% in December. The February contract was more muted rising only 1.7% to $3.943 but is down 10.8% on the month. It reached $4.029 but breaks above $4 were short lived.

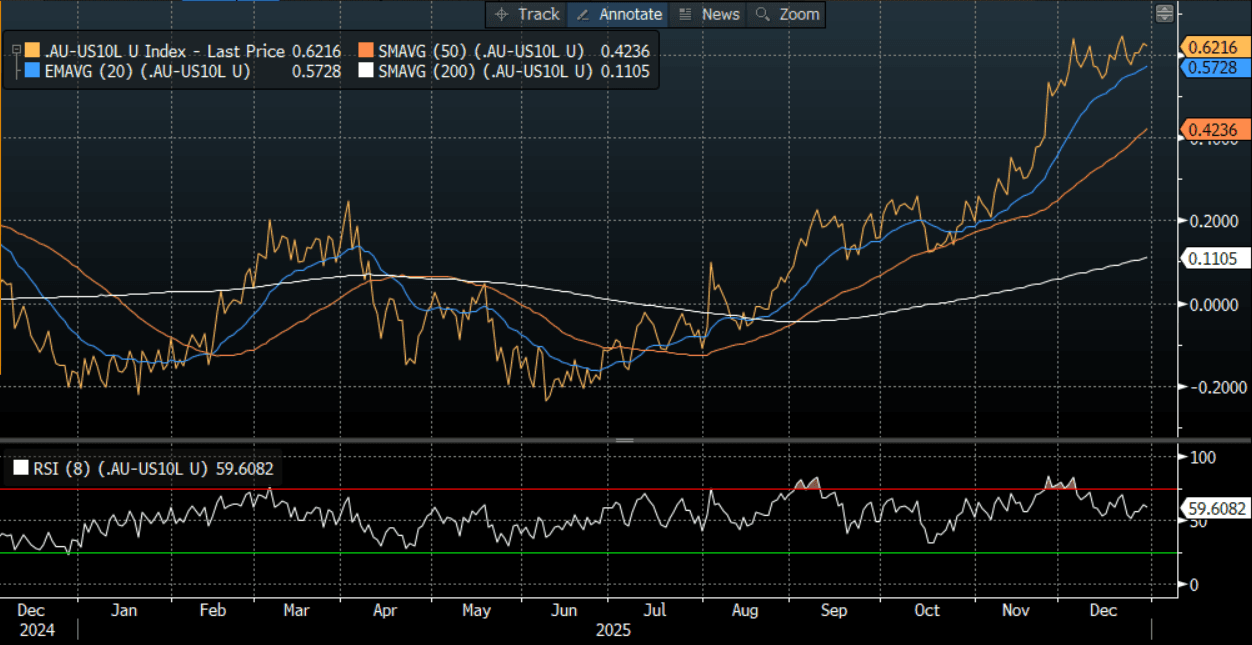

AUSSIE BONDS: Richer But AU-US 10Y Diff At Highest Since Mid-2022

ACGBs (YM +2.5 & XM +2.0) are slightly stronger after the positive lead from US tsys’ close on Monday.

- Cash US tsys are slightly richer in today’s Asia-Pac session. The Fed will release minutes of its Dec. 9-10 meeting, where the central bank lowered the policy rate by 25bps. Fed Governor Stephen Miran voted against the decision in favour of lowering rates by twice as much.

- Cash ACGBs are 2bps richer with the AU-US 10-year yield differential at +63bps. At this level, the differential sits around its cycle high, the widest since mid-2022 (see chart).

- The bills strip is mostly stronger, +1 to +2 across contracts beyond the first two contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 37% for February to 97% by June and 147% by December 2026.

- By the end of January, Australians should have a clearer picture of whether they can expect interest rate hikes in 2026. Quarterly inflation data, due to be released on January 28, will confirm or allay RBA fears that upward price pressures are entrenched in the economy.

Bloomberg Finance LP

OIL: Crude Starts Tuesday Lower Following US Inventory Data Showing Builds

After falling sharply on Friday, crude was higher on Monday driven by already slow progress on a Ukraine peace deal but Russia then stating that it will now appraise its negotiating position after it claimed that President Putin’s Novgorod residence was attacked by Ukrainian drones, which President Zelenskyy has denied. Holiday-related illiquidity is also causing volatility.

- The EIA reported delayed US inventory data for the week ending 19 December. It showed a stock build of 0.4mn barrels which followed two consecutive drawdowns. Distillate inventories rose 0.2mn and gasoline 2.86mn, 6th straight weekly increases. Refinery utilization fell 0.2pp to 94.6%, 2.1pp higher than the same time in 2024.

- WTI rose 1.9% to $57.83/bbl on Monday but off the intraday high at $58.30. It has started today lower at $57.74 likely pressured by the latest US crude & product inventory build.

- Brent was up 2.1% to $61.94/bbl following a peak of $62.19. The benchmark is still down 1.0% in December. The December average is on track to post its lowest level since Covid-impacted January 2021, as excess supply has been the main market driver.

- Geopolitics have provided some support and remain a watch point with the US announcing a strike on another Venezuelan narcotics vessel and threatening to attack Iran if it resumes building nuclear weapons, as well as higher uncertainty over Ukraine peace talks.

- China’s Ministry of Finance said Sunday that it would extend the breadth of government spending in 2026 to support economic growth, which would likely increase energy demand.

- Bloomberg is reporting that Venezuela began to shut oil wells on Sunday as the US blockade has driven an increase in crude and product inventories which have filled storage. While the country has the largest known deposits, it was only the 17th largest oil exporter in 2023, according to the IEA.