ASIA STOCKS: Big Flows for South Korea and India

After an exceptional period of inflows into the major markets, it appears that this trend has stalled for now as constant daily flows are interrupted with outflows, with Taiwan the latest to experience a significant outflow yesterday.

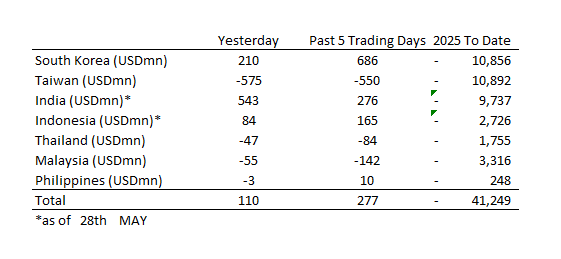

- South Korea: Recorded inflows of +$210m yesterday, bringing the 5-day total to +$686m. 2025 to date flows are -$10,856. The 5-day average is +$137m, the 20-day average is +$91m and the 100-day average of -$107m.

- Taiwan: Had outflows of -$575m as yesterday, with total outflows of -$550m over the past 5 days. YTD flows are negative at -$10,892. The 5-day average is -$110m, the 20-day average of +$378m and the 100-day average of -$110m.

- India: Had inflows of +$543m as of the 28th, with total inflows of +$276m over the past 5 days. YTD flows are negative -$9,737m. The 5-day average is +$55m, the 20-day average of +$141m and the 100-day average of -$107m.

- Indonesia: Had inflows of +$84m as of the 28th, with total inflows of +$165m over the prior five days. YTD flows are negative -$2,726m. The 5-day average is +$33m, the 20-day average +$17m and the 100-day average -$29m.

- Thailand: Recorded outflows of -$47m as of yesterday, outflows totaling -$84m over the past 5 days. YTD flows are negative at -$1,755m. The 5-day average is -$17m, the 20-day average of -$2m and the 100-day average of -$18m.

- Malaysia: Recorded outflows of -$55m as of yesterday, totaling -$142m over the past 5 days. YTD flows are negative at -$3,316m. The 5-day average is -$33m, the 20-day average of +$18m and the 100-day average of -$23m.

- Philippines: Saw outflows of -$3m yesterday, with net inflows of +$10m over the past 5 days. YTD flows are negative at -$248m. The 5-day average is +$2m, the 20-day average of +$2m the 100-day average of -$3m.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: CHINA APR CAIXIN MANUFACTURING PMI 50.4 VS 51.2 IN MAR

- CHINA APR CAIXIN MANUFACTURING PMI 50.4 VS 51.2 IN MAR

NEW ZEALAND: Businesses Less Certain On Outlook, Gradual Recovery Continues

ANZ business confidence fell to 49.3 in April from 57.5, the lowest level since July 2024, the month before the start of the RBNZ’s easing cycle. The activity outlook moderated to 47.7 from 48.6, which remains above February’s 45.1. On a more positive note, the assessment of activity compared to a year ago rose 10 points to 11 driven by services and signalling a strong start to Q2 for GDP growth. Price/cost components trended higher over Q1 but were mixed in April but inflation expectations were stable around 2.6%.

NZ ANZ business activity outlook vs employment intentions

Source: MNI - Market News/LSEG

- It is likely that the survey was impacted by US tariff announcements, as ANZ noted that “forward-looking activity indicators were sharply lower in the late-month responses”. Export intentions fell 5 points to 12.2 with manufacturing down 7.6 points, while investment intentions were steady around 17.2.

- Employment compared to a year ago rose to +1.5 from -6.2 with services, construction and agriculture showing more jobs, while employment intentions rose 2.5 points to 18.1, the highest since July 21. This is in line with filled jobs and vacancy data showing a turn in the labour market. Wages expectations a year ahead rose over a point to 81.3.

- Cost expectations 3 months ahead rose to 77.9 from 74.1, highest since September 2023, while pricing intentions moderated almost 2 points to 49.4, signalling some margin squeeze. Profit expectations fell 1 point.

NZ ANZ business survey costs/prices

CHINA: Official PMI Slips into Contraction

- As anticipated following the release of the EPMI Index, China’s official PMI manufacturing slipped into contraction in April.

- Following March’s result of +50.5 April fell to +49.0, below expectations of +49.7.

- The Non-Manufacturing PMI slipped to +50.4 from +50.8 last month

- These are the first PMI readings since the trade war kicked off with the imposition of 145% tariffs on Chinese goods to the US and as shipments to the US crater the official forecast of 5% growth now looks challenging.

- Authorities have announced measures to support exporters with access to loans and continues to seek ways of boosting the domestic economy.

- However today’s result seems likely a taste of things to come as the trade war impacts not just China corporates, but the region as a whole.