JAPAN DATA: Tokyo CPI Core Measures Continue To Firm

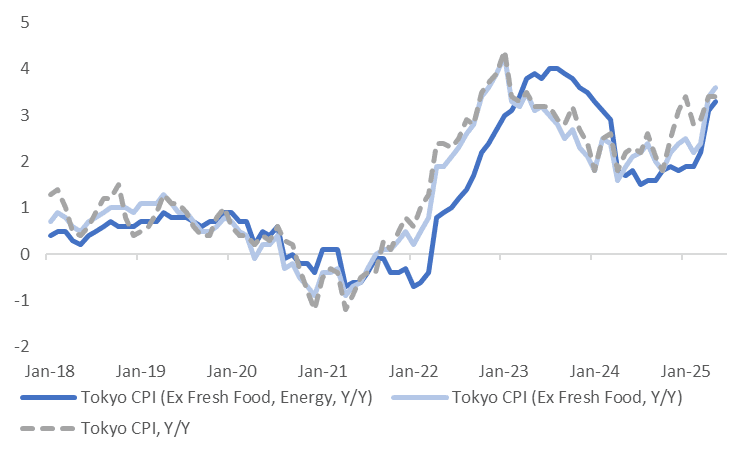

May Tokyo CPI saw core measures print firmer than expected. Headline rose 3.4% y/y, in line with consensus estimates, which was also the prior outcome (revised down from 3.5% originally reported). The ex fresh food measure rose 3.6%y/y (3.5% was the forecast and 3.4% prior). Ex fresh food and energy was 3.3%y/y, against a 3.2% forecast and 3.1% April print.

- The chart below plots the trend y/y outcomes for these three metrics. The continued upward momentum in the core outcomes should, at face value, add to BoJ confidence around achieving its inflation target sustainably. BoJ Governor Ueda continues to hint at progress on this front, but the inflation goal has not yet been reached.

- The core measure excluding fresh food and energy is now back to early 2024 levels in y/y terms.

- In m/m (seasonally adjusted terms), headline rose 0.3%, while the core measures were up 0.4-0.5%. Good prices rose 0.6% after a flat April. Services were up 0.2%, after a 0.3% gain in April. The measure which excludes all food and energy only rose 0.1%m/m (non seasonally adjusted), but still ticked up to 2.1%y/y (from 2.0%).

- By segment, drags came from fresh food (-2.5%m/m), but overall food was +0.3%m/m. Household goods eased -0.1%m/m, so did medical care. Utilities rose a solid 3.0%m/m, while entertainment was up 0.2%m/m after a strong gain in April. Utility bill relief is expected in Q3 of this year, while policy initiatives are also steeping up to curb food inflation.

- Y/Y momentum by segment was similar to April trends. Housing is the lower y/y pace at 1.5%, while other segments are either close to the 2% pace, or higher.

Fig 1: Tokyo CPI Y/Y - Core Measures Continue To Accelerate

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI: MNI JAPAN MAR FACTORY OUTPUT -1.1% M/M; FEB +2.3%

- MNI JAPAN MAR FACTORY OUTPUT -1.1% M/M; FEB +2.3%

- JAPAN MAR FACTORY OUTPUT POST 1ST M/M DROP IN 2 MONTHS

OIL: Trade Worries Continue To Weigh On Crude As April Survey Data Fall

Oil prices fell sharply on Tuesday as continued uncertainty over the progress of US trade negotiations especially with China and concerns over increased OPEC output weighed. It has worried about the impact on global energy demand since US tariffs were announced and data are starting to confirm these fears. April US consumer confidence was sharply lower yesterday following Monday’s drop in the Dallas Fed index. China’s PMI out today will also be monitored closely. The USD index was 0.2% higher.

- WTI fell 3.1% to $60.14/bbl, close to the intraday low, and still above support at $58.29. The bear trigger is at $54.67. It is now down 15.2% in April and 14.3% this year. The benchmark has started today a bit higher at $60.24.

- Brent was 2.8% lower at $63.28/bbl after briefly falling below $63 to reach $62.93. It is now down 14.8% this month. This reinforces the downward trend in the benchmark but it continued to hold above initial support at $61.51/bbl. The bear trigger is at $58.00. Initial resistance is at $68.67, 50-day EMA.

- Bloomberg reported that there was a US crude inventory build of 3.8mn barrels last week, according to people familiar with the API data. Products continued to destock with gasoline down 3.1mn and distillate 2.5mn. The official EIA data is out on Wednesday.

JGBS: Trading To Resume After Yesterday's Holiday

In post-Tokyo trade on Monday, JGB futures closed weaker, -9 compared to settlement levels, ahead of yesterday’s holiday.

- Overnight, US yields finished at the lows of the session with the 10-year 4bps lower at 4.17% and the 2-year down 4bps to 3.65%. For the 2-year, it was the lowest since October, while the 10-year is at its lowest since April 4.

- President Trump is speaking in the White House in the first 100 days—details to come.

- The JOLTS report saw a second month with lower-than-expected job openings, and this time by a greater extent in March. However, layoffs fell to their lowest since June and quit rates surprisingly increased.

- US consumer confidence dropped for a 5th consecutive month in April following the November peak per the Conference Board's survey, with the Composite to 86.0 (88.0 expected, 93.9 prior upwardly revised from 92.9) - the lowest since May 2020.

- Focus now turns to Wednesday's ADP private jobs data, GDP, Chicago PMI, PCE and Home Sales.

- Today, the local calendar will see Industrial Production and Retail Sales. The BoJ is scheduled to hold its MPM today and tomorrow, during which it will also release its latest Outlook Report. The BoJ is widely expected to leave its benchmark interest rate unchanged at 0.5%.