JPY: Asia Wrap - Risk Drifting Lower, The JPY Benefits

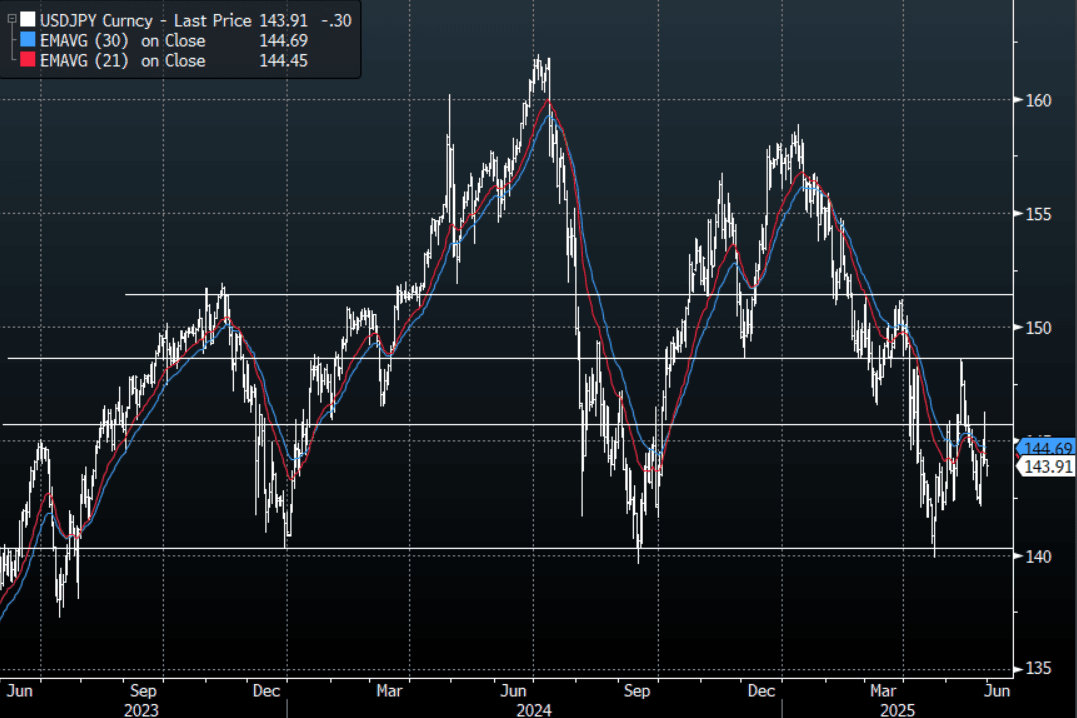

The Asia-Pac USD/JPY range has been 143.44 - 144.21, Asia is currently trading around 143.90. USD/JPY has remained offered in our session as the market's focus returns to selling the USD once more as US Stocks drift lower.

- (JAPAN DATA) Tokyo CPI Core Measures Continue To Firm : May Tokyo CPI saw core measures print firmer than expected. Headline rose 3.4% y/y, in line with consensus estimates, which was also the prior outcome (revised down from 3.5% originally reported).

- The continued upward momentum in the core outcomes should, at face value, add to BoJ confidence around achieving its inflation target sustainably. BoJ Governor Ueda continues to hint at progress on this front, but the inflation goal has not yet been reached.

- UEDA: “SET SHORT-TERM POLICY RATE TO HIT INFLATION TARGET, UNREALIZED JGB LOSSES WON'T AFFECT REVENUE" - BBG

- US Stocks came under some pressure as the WSJ reports Trump is actively looking for alternative ways to impose his agenda should the appeal fail, this saw some renewed demand for safe currencies like the JPY.

- The market was very quick to reinstate short USD/JPY positions overnight as the “sell America” trade gains in popularity.

- The market seems very confident of a move lower in USD/JPY but with positioning quite large now the price action of the last couple of days highlights the increased risks of pullbacks. Resistance around the 146.00 area held perfectly and the JPY bulls would be quite relieved as well as vindicated by the price action. The next pivotal trigger points look to be below 140.00 on the downside and above 146.50 on the topside.

Options : Close significant option expiries for NY cut, based on DTCC data: 143.00($3.39b May 30), 140.00($2.78b May 30). Upcoming Close Strikes : 147.50($475m June 2), 147.75($476m June 3)

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Asia Wrap - Quiet Session

TYM5 has traded a little higher with a range of 112-04 to 112-09 during the Asia-Pacific session. It last changed hands at 112-06, up 0-01 from the previous close.

- The US 10-year yield is a little lower, dealing around 4.16%, down from its close around 4.1716%.

- The US 2-year yield is unchanged, dealing around 3.65%.

- US President Trump has spoken at a rally in Michigan, which marks his first 100 days in office. The speech was big on rhetoric, but policy related areas of interest for the market remained light.

- “The trade deficit widened to a record in March, and consumer spending slowed, contributing to the GDP growth slowdown.”(per BBG)

- MNI Economist re GDP - “Domestic demand should look somewhat more robust but will be clouded by question marks over the extent to which areas of strength were driven by tariff front-running”.

- Month End flow will continue to be a key driver tonight.

- The 10-year Yield, has put in a lower high around 4.40% and has broken through the recent support around 4.25%. The next support is towards the 4.10 area which should find supply once more.

- Data/Events : ADP private jobs data, GDP, Chicago PMI, PCE and Home Sales.

AUD: A$ Outperforms Following Slightly Higher Q1 CPI Print, US GDP Out Later

AUDUSD jumped on the moderately higher-than-expected Q1 CPI data that included upward revisions to Q4 and Aussie is now outperforming the rest of the G10, despite mixed equities and lower commodity prices. It reached a low of 0.6379 before the data and then jumped to 0.6407 following the print but has struggled to hold the break above 64c and is currently around 0.6398 to be up 0.2% today. The USD index is little changed.

- AUDNZD has trended higher through most of the session and is now +0.3% to 1.0792, close to today’s peak.

- AUDJPY is up 0.2% to 91.09, close to the intraday high of 91.22. AUDEUR rose to 0.5634 following Australia’s inflation data and is now +0.3% to 0.5624. AUDGBP is also 0.3% higher at 0.4777 off the peak of 0.4781.

- Equities are mixed with the ASX up 0.2% but Hang Seng down 0.4% and S&P e-mini -0.5%. Oil continues to sell off with WTI -0.9% to $59.90. Copper is down 1.2% and iron ore is around $98/t.

- Later US Q1 GDP & employment costs, March core PCE prices, April MNI Chicago PMI & ADP employment print. Also preliminary April euro area CPI, Q1 GDP including Germany, France & Italy, German March retail sales & unemployment are released. BoE’s Lombardelli speaks.

JGBS: Slightly Mixed After Domestic Data Drop

At the Tokyo lunch break, JGB futures are little changed, +1 compared to the settlement levels.

- March preliminary industrial production was below market forecasts, down 1.1%m/m, versus -0.4% expected. In y/y terms, we came in at -0.3% versus 0.8% forecast (0.1% was the prior outcome). The y/y trend hasn't been able to see much upside traction for a number of years now. The current y/y pace is slightly above averages for 2023/24, but only marginally.

- Retail sales were slightly below market forecasts. We were -1.2%m/m, against a 0.7% forecast, with Feb revised to a 0.4% gain. In y/y terms, we rose 3.1%, against a 3.5% forecast and 1.3% in Feb. The y/y trend is around mid-range of the past 12 months, as we have oscillated between flat to +5%. The authorities remain focused on driving sustained/positive real household spending growth, aided by positive real wages growth. The next round of labour earnings data is due next Friday.

- Cash US tsys are slightly mixed, with a flattening bias, in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are mixed, with benchmark yields 1bp lower (5-year) to 1bp higher (30-year). The benchmark 10-year yield is 0.3bp higher at 1.321% versus the cycle high of 1.596%.

- Swap rates are 1-2bps lower. Swap spreads are mixed.