MNI EUROPEAN MARKETS ANALYSIS: Rupee Rebounds On Intervention

- Oil had one of its biggest one day jumps this month as the US President ordered a total blockade of all Venezuelan sanctioned oil tankers. Prior to the news, WTI had for four consecutive days, only to jump by +1.5% initially.

- Equity markets brushed off the US finish and were boosted in the region by the debut of a Chinese tech / AI company MetaX Integrated Circuits which jumped over 600% on debut, mirroring that of another Chinese tech Moore Threads recently. The debut shows that the demand for China AI / tech companies is strong in the face of geopolitical tensions with the US.

- The Indian Rupee delivered strong gains in morning trade as the RBI intervened aggressively in the underperforming currency, seeing gains of 0.75% in rupee terms.

- Ahead markets turn their attention to UK CPI and PPI, EU HICP final and in the US Fed Speakers from Waller, Williams and Bostic.

MARKETS

US TSYS: Bonds Weaker on Equity Rebound, TYH6 Below Key Tech Level

US bond futures headed lower in the afternoon as equities across the region delivered strong gains. The 10-Yr is down -04 to 112-12+. The losses take TYH6 back below the 100-day EMA of 112-14. Downside resistance now is the 200-day EMA of 111-30.

Cash is weak also with yields +1.3bps to +2.8bps higher across the curve.

- The 2-Yr is up +1.3bps to 3.502%

- The 5-Yr is up +1.8bps to 3.716%

- The 10-yr is up +2.3bps to 4.17%

- The 30-Yr is up +2.8bps to 4.844%

Fed Speakers Wednesday will be watched carefully by markets with Waller, Williams and Bostic speaking with investors also looking ahead to Thursday's November CPI release.

Geopolitics could have a say in the outlook for risk sentiment as the US President orders the blockade of sanctioned oil tankers in Venezuela as US equity futures trend downwards.

Tonight sees a US$69bn 17-week bill auction and a US$13bn 20-Yr re-opening.

JGBS: Multiple Weights On JGB Futures, 10yr JGB Yield Eyeing 2.00% Upside Test

JGB futures have softened post the lunch time break in Japan. We were last 133.18, -.25 versus settlement levels. Session lows rest at 133.14. Note earlier lows in Dec were around 133.11. A clean under 133.00 would see projection levels targeted next (SUP 2: 132.78 - 2.0% Lower Bollinger Band and SUP 2: 132.78 - 2.0% Lower Bollinger Band).

- Weights on futures have BoJ buying in the 5-10yr tenor as part of its weekly ops (¥846.6bn purchased for this segment, versus ¥491.3bn last week). We also had a lower bid to cover ratio on the 1yr debt auction (3.01, versus 3.706 prior). Lower US Tsy futures (with cash Tsy yields up 1-2.5bps) has also likely been a headwind.

- In the cash JGB space, yields have firmed as the afternoon session progressed. The 10yr up 2bps to 1.98%, at fresh cycle highs. The 1yr is up over 2bps last 0.86%.

- Earlier data was supportive for the Japan outlook, but shouldn't shift BoJ thinking. Export growth is trending higher, while core machine orders surged in Oct, suggesting a positive Q4 capex backdrop.

- Tomorrow on the local calendar we just have weekly offshore investment flows. Then Friday delivers the BoJ outcome. A 25bps hike is widely expected and close to fully priced. See our full preview here.

MNI BoJ Preview-Dec 2025: Hike Fully Priced

EXECUTIVE SUMMARY:

- The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18–19 meeting, with Governor Ueda’s recent remarks signalling increased confidence in the outlook for growth, inflation and wage momentum.

- Ueda has indicated the BOJ will assess the “pros and cons of raising the policy interest rate,” while Policy Board members say conditions for a hike are “gradually falling into place,” though confirmation of spring wage momentum remains key.

- Market pricing has shifted as the Takaichi administration appears willing to tolerate a hike despite its reflationary stance, with analysts arguing that monetary tightening can “substitute for fiscal easing” amid rising JGB yields.

- Some caution remains, with analysts noting that limited wage data ahead of the meeting could prompt the BOJ to delay a hike until more information emerges later in December or January.

- Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as “1–2.5%,” signalling that policy normalisation is likely to continue gradually rather than end at 1%.

FOR THE FULL PUBLICATION PLEASE USE THE FOLLOWING LINK:BOJ Preview - Dec 2025.pdf

JAPAN DATA: Export Pick Up Consistent With Broader Asia Trends, Aided By Chips

Japan Nov trade data was slightly better than forecast. Exports rose 6.1%y/y (5.0% projected and 3.6% prior), while imports were +1.3%y/y (against a 3.0% forecast). This saw the trade surplus print at ¥322.3bn, against a ¥72.6bn forecast and -¥226.1bn prior outcome. In seasonally adjusted terms the surplus was ¥62.9bn, also well above market forecasts. The pick up in export growth will be welcome by the authorities/BOJ, with concerns earlier in the year higher US tariff levels would weigh on external demand.

- The improvement in Japan export growth is consistent with other export orientated Asian economies, with growth ticking up into year end. Taiwan remains the standout though.

- Japan exports were firmer to the US, up 8.8%y/y (from -3.1%y/y prior), while to the EU posted a 19.6%y/y rise (exports to China fell 2.4%y/y). Automobile exports to the U.S. increased 1.5%, rebounding from a 7.5% decline in October. Aggregate chip exports were firm at 13%, after a 15.8% rise in Oct.

- In volume terms exports to the US were up 14%y/y, to the EU 16%y/y, but negative to China and Asia.

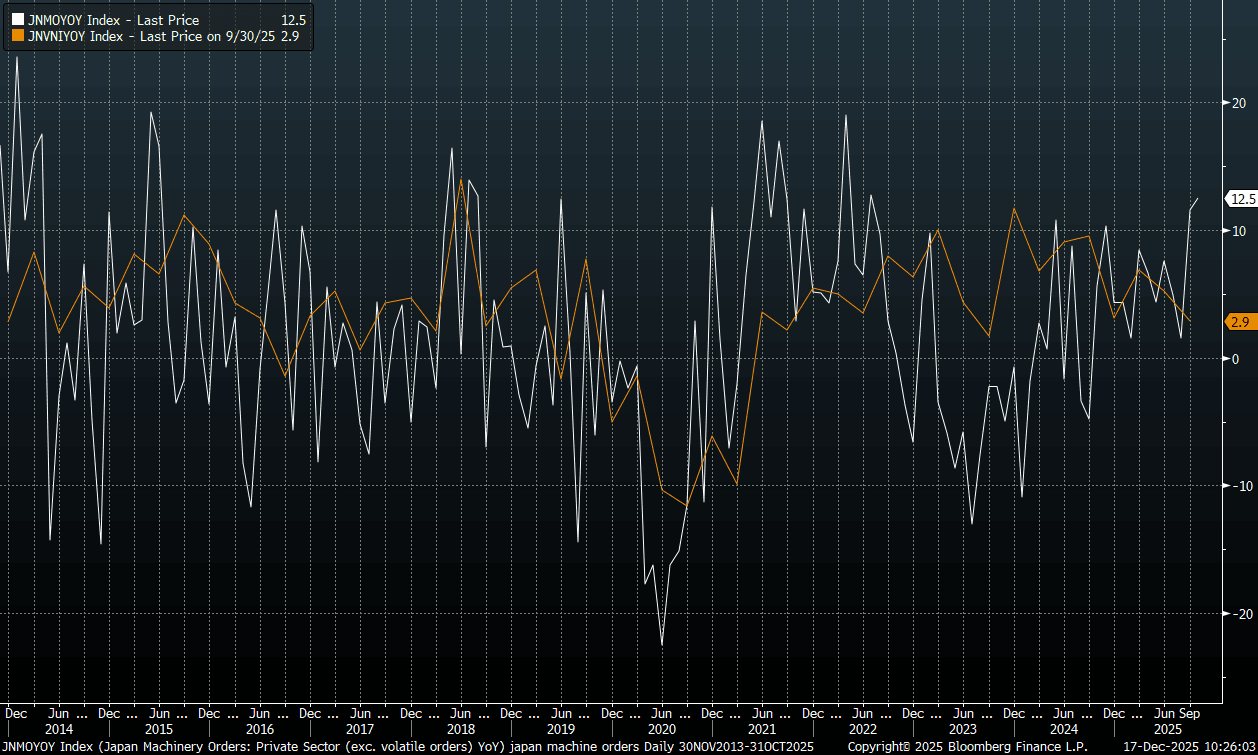

JAPAN DATA: Machine Orders Well Above Forecasts, Bodes Well For Capex Spend

Japan core machine orders for Oct were notably above forecasts. In m/m terms we rose 7.0%, against a -1.8% forecast, while y/y we rose 12.5%, versus a 3.6% forecast. This leaves the y/y pace at fresh highs back to 2022. The chart below plots the machine order print against capex y/y (ex software). The positive trend for machine orders bodes well for the capex outlook. Business/capex spending has been an important source of growth for Japan, although we saw a dip in Q3.

Fig 1: Japan Core Machine Orders & Capex Y/Y (Ex Software)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Slightly Cheaper, MYEFO Out, Little Reaction

ACGBs (YM -2.0 & XM -1.0) are little changed on a data-light day.

- Today’s auction result for the Oct-36 bond extended the recent trend of firm pricing for ACGBs, with the weighted average yield printing 0.33bps through prevailing mids. Moreover, demand was robust, as reflected by a cover ratio of 3.7100x.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session.

- Australia’s mid-year budget update shows the government continuing to run sizeable deficits over the forecast period, despite tighter spending controls and expectations of stronger revenue from an economic recovery. The underlying cash deficit is projected at A$36.8 billion, or 1.3% of GDP, in the year to June 2026, with deficits narrowing only gradually to around 1.1% of GDP per year by fiscal 2029. The government highlighted A$20 billion in savings identified in the MYEFO and said it will constrain average real spending growth to 1.7% over the seven years to 2028–29, well below the 30-year average of 3.3%.

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at +58bps.

- The bills strip pricing is -1 to -3 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 100% by June and 160% by December 2026.

- Tomorrow, the local calendar will see Consumer Inflation Expectation.

BONDS: NZGBS: Quiet Session Despite A Few Headlines, Q3 GDP Tomorrow

NZGBs remain little changed after a relatively quiet session of trading despite a few headlines.

- The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. As a percentage of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve; we were at -9.0% of GDP at the end of 2022.

- (Bloomberg) NZ needs higher capital standards than its peers because of higher risks in a small economy, RBNZ Governor Anna Breman said on a conference call Wednesday in Wellington after the central bank announced changes to bank capital settings.

- NZ-US and NZ-AU 10-year yield differentials are little changed on the day despite the above announcements.

- Swap rates are little changed.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for February, while November 2026 assigns 44bps.

- Tomorrow, the local calendar will see Q3 GDP.

Bloomberg Finance LP

FOREX: USD - BBDXY Pushes Higher In Asia

The BBDXY has had a range today of 1204.77 - 1206.60 in the Asia-Pac session; it is currently trading around {BBDXY Index}. The USD broke below 1204 in reaction to the US data overnight, but it could not follow through and has recouped all of yesterday's losses and more. On the day I am a little confused, perhaps some patience is needed for a look back towards the 1208-110 area and above here the more important 1213-1216 area where sellers should remerge initially. Can this 1204 area provide some support again if not a move below here would target 1198-1200.

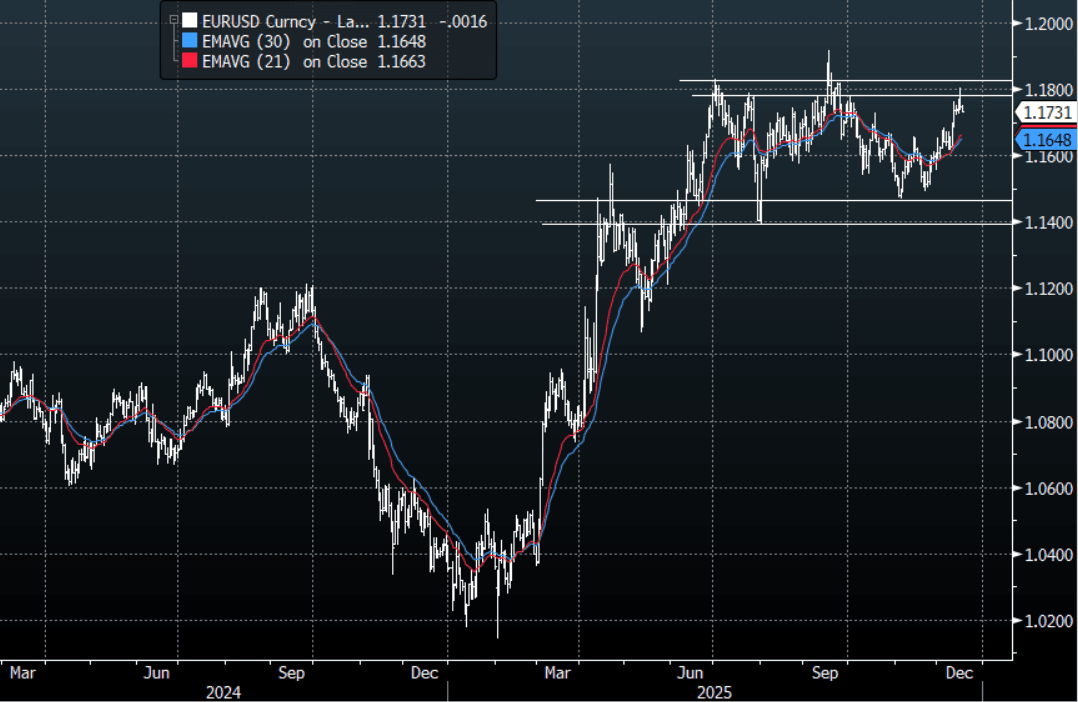

- EUR/USD - Asian range 1.1737-1.1752, Asia is currently trading {EURUSD Curncy}. The pair did not like it back up towards 1.1800 and very quickly rejected the move higher. On the day, first support is toward 1.1680-1710 initially, looking for the pair to consolidate before finding a base to attempt another move higher again.

- GBP/USD - Asian range 1.3407-1.3427, Asia is currently dealing around {GBPUSD Curncy}. The pair stalled back toward the 1.3450 level overnight. On the day GBP has initial support around the 1.3340-1.3370 area, if this does not hold look for a pullback to the more important 1.3260/90 area. I continue to watch for signs of GBP potentially topping out, which for the moment looks a lost cause.

- Cross asset : SPX -0.05%, Gold $4325, US 10-Year 4.16%, BBDXY 1205, Crude Oil $55.97

- Data/Events : Germany IFO, Spain Total Mortgage Lending, EZ CPI/Labour Costs YoY

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

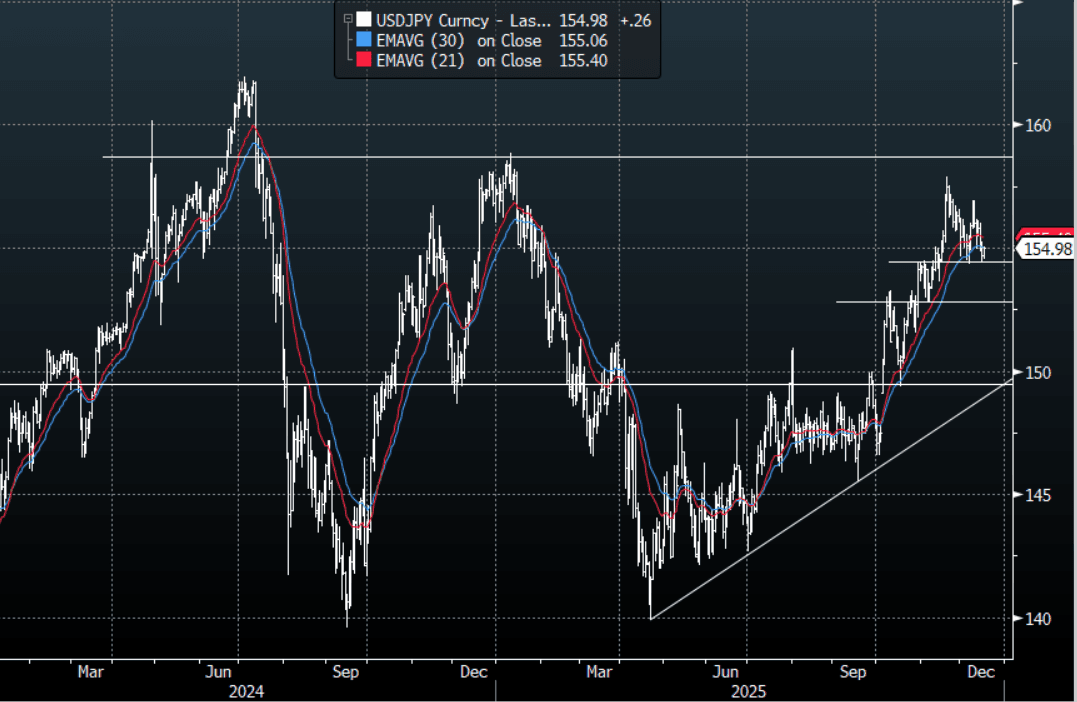

JPY: USD/JPY - Chops Around Above 154.50

The USD/JPY range today has been 154.52 - 155.03 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. The pair chopped around in a 50 point range without really going anywhere in Asia. The market is pricing in a hike by the BOJ for this week, for the time being this is keeping the JPY contained and confined to a wider 154.00-157.00 range having capped its upward momentum. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. In today's Asian session, look for resistance back toward the 155.00-155.30 area initially, should this hold look for a retest of the 154.30-50 area at some point a break of which could signal a deeper pullback. A break above 155.20-30 and the price could move back toward 155.70-156.00.

- MNI AU - MNI BOJ Preview: Hike Fully Priced For This Week: Executive Summary The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18-19 meeting, with Governor Ueda's recent remarks signaling increased confidence in the outlook for growth, inflation and wage momentum. Ueda has indicated the BOJ will assess the "pros and cons of raising the policy interest rate," while Policy Board members say conditions for a hike are "gradually falling into place," though confirmation of spring wage momentum remains key.

- Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as "1-2.5%," signaling that policy normalisation is likely to continue gradually rather than end at 1%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.75($950m), 156.00($760m). Upcoming Close Strikes : 157.00($4.15b Dec 18 ), 158.00($4.98b Dec 18 ), 159.00($6.46b Dec 18 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 101 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

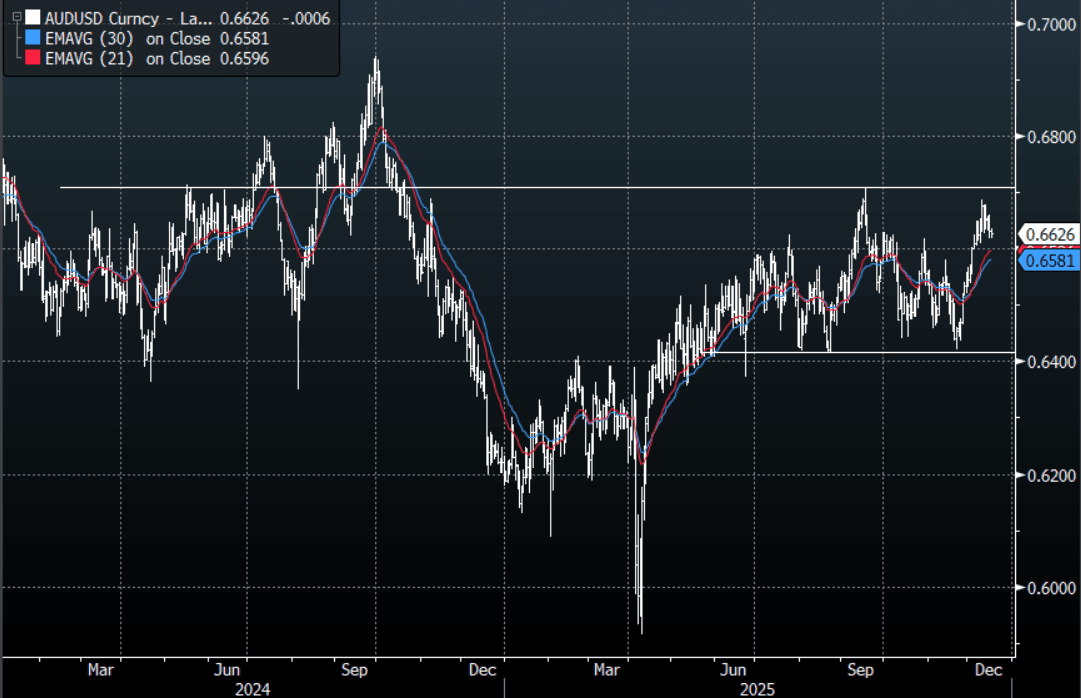

AUD/USD - Consolidating Above 0.6600-0.6630

The AUD/USD has had a range today of 0.6619 - 0.6635 in the Asia- Pac session, it is currently trading around {AUDUSD Curncy}. The AUD slipped lower as risk took a turn for the worst in Asia on the US blockade of Venezuela, risk has since pared back those losses but the USD has remained bid for now. The AUD price action remains constructive and while the AUD remains above 0.6500-0.6550 I suspect dips could continue to be supported. On the day, while the 0.6600-0.6630 area continues to provide support I would probably be skewed long looking for a move back toward the 0.6660-80 resistance. If this support area does not hold it could signal a deeper pullback toward the 0.6550 area.

- "AUSTRALIA NOV. WESTPAC LEADING INDEX FALLS 0.04% M/M" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6590(AUD680m), 0.6700(AUD655m). Upcoming Close Strikes : 0.6550(AUD1.07b Dec 18 ), 0.6675(AUD1.1b Dec 19), 0.6700(AUD1.57b Dec 19) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

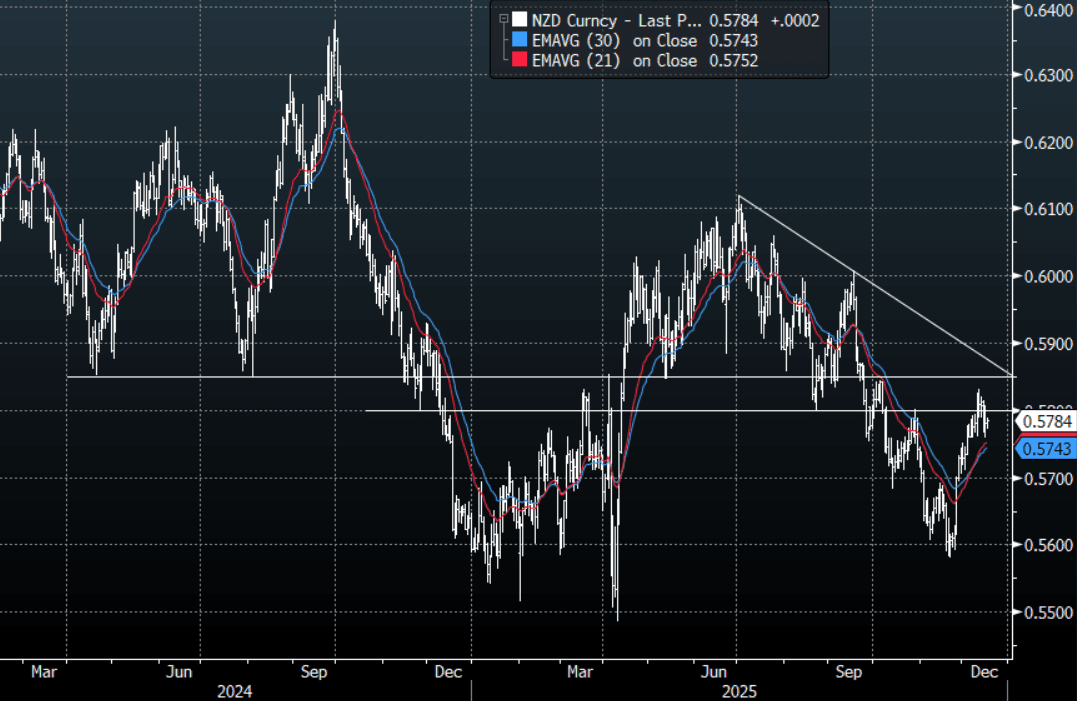

NZD/USD - Unchanged, Consolidating Above 0.5750

The NZD/USD had a range today of 0.5771-0.5789 in the Asia-Pac session, going into the London open trading around {NZD Curncy}. The NZD traded sideways in a quiet session, consolidating its gains above 0.5700-0.5750. On the day, I suspect this sort of price action could continue as the pair settles into a range, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30.

- MNI AU - Q3 Current Account Deficit, As % Of GDP, Continues Improvement: The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

- MNI AU - Further Weakness In Whole Milk Prices, Back To Mid 2024 Levels: Overnight the GDT whole milk auction price fell sharply, down 5.7% on the prior outcome to $3161/mt. This is the lowest level since mid 2024 for the twice monthly auction outcome. The Q3 official terms of trade print for NZ showed a 2.1%q/q fall. We were still up 7.2% in y/y terms. Export prices are moving off earlier 2025 highs, consistent with lower whole milk auction price outcomes.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5780(NZD344m), 0.5800(NZD502m), 0.5850(NZD328m). Upcoming Close Strikes : 0.5630(NZD594m Dec 19), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Chinese AI Chip Co. Debut Gives Tech Stocks a Boost

Asia's equity markets are higher today with China's bourses up as tech stocks rebounded and hopes of further interest rate cuts in the US prevail. The NIKKEI was up as it awaits the decision this week by the BOJ on interest rates with it widely expected that rates will rise by 25bps. China's bourses were buoyed by the market debut of AI chipmaker MetaX Integrated Circuits on the Shanghai exchange. MetaX shares jumped by over 600% on their first day of trading, following a similar stellar performance by rival Moore Threads earlier in the month. This highlights investor enthusiasm for homegrown Chinese technology companies amid geopolitical tensions with the US. The optimism for the tech sector in China spilled over into Korea with key tech stocks in Korea up between 1-3%.

- The NIKKEI feels like it is treading water ahead of the BOJ but remains up a mere +0.08% today, whilst the KOSPI found real support for tech stocks and is up +0.80%.

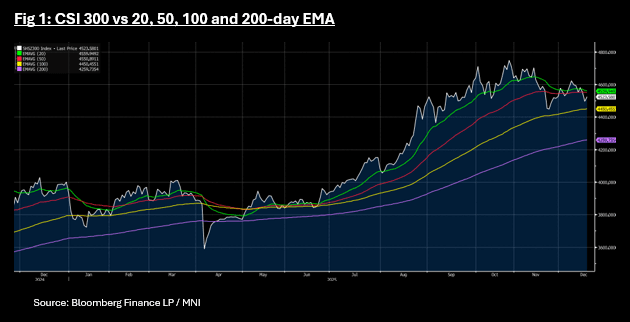

- China's major bourses were all up between +0.20% + 0.60% with the CSI 300 the outperformer. The gains for the CSI 300 to 4,523 sees it at the mid-point of the topside resistance from the 50-day EMA of 4,550 and the downside resistance from the 100-day EMA at 4,450.

- India's NIFTY 50 has opened flat after two days of falls as investors look for signals for US interest rates whilst commodity prices remain pressured.

- SE Asia's bourses were mixed with the Jakarta Comp up +0.20% and the FTSE Malay KLCI down -0.50%.

ASIA STOCKS: Equity Outflows Accelerate - Taiwan -$3.8bn Last Two Days

Asian markets saw an increase in equity outflow pressures yesterday. Tech sensitive plays, particularly Taiwan, saw the brunt of the selling pressure. For Taiwan, offshore investors have sold just over $3.8bn of local stocks in the last two sessions. For South Korea we have seen just over $1.6bn in net selling. Tech/AI valuation concerns continues to see tech equity indices struggle, although the MSCI IT index posted a small rise for Tuesday. The Kospi is up modestly in the first part of Wednesday trade, but offshore investors are still net sellers per the NBUY function on BBG.

- In SEA, we saw net selling as well across the board, as broader equity sentiment was challenged yesterday. Today's focus will rest with central bank decisions in Indonesia and Thailand. The BoT is expected to cut, while BI is seen on hold, albeit in close run decision (with some analysts seeing a cut).

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -939 | -837 | -5654 |

| Taiwan (USDmn) | -2117 | -3238 | -7912 |

| India (USDmn)* | 64 | -591 | -17686 |

| Indonesia (USDmn) | -56 | 55 | -1602 |

| Thailand (USDmn) | -11 | -16 | -3273 |

| Malaysia (USDmn) | -33 | -97 | -4806 |

| Philippines (USDmn) | -7 | -44 | -844 |

| Total (USDmn) | -3098 | -4769 | -41777 |

| * Data Up To Dec 15 |

Source: Bloomberg Finance L.P./MNI

Oil Up Strongly on Venezuela Orders

- Oil spiked in Wednesday morning trade in Asia as President Trump said he was ordering a 'total and complete blockade of all sanctioned oil tankers' going into and leaving Venezuela.

- "Venezuela is completely surrounded by the largest Armada ever assembled in the History of South America," Trump wrote on social media Tuesday. "It will only get bigger, and the shock to them will be like nothing they have ever seen before (per BBG)

- Trump said he was also designating the regime of Venezuelan President Nicolas Maduro as a "Foreign Terrorist Organization" according to his Truth Social post.

- WTI was up +1.52% this morning on the news to US$56.02 before falling back and stabilizing at US$55.96.

- Today's moves is one the largest one day jump since the beginning of December.

- The latest move by the US administration is a major escalation against Venezuela, the holders of some of the largest oil reserves on the planet.

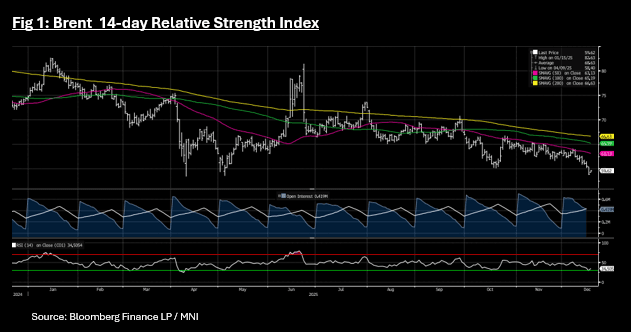

- Brent is up by +1.33% to US$59.61 as it moves back above oversold on the 14-day Relative Strength Index.

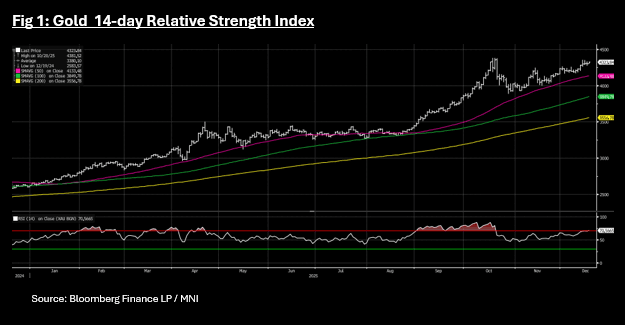

Gold Reaches Overbought on RSI

- As equities perform better today, gold now turns its attention to US inflation data out Thursday whilst monitoring events in Venezuela as the US President orders a blockade of their sanctioned oil tankers.

- With a raft of data to come including CPI for November, the future path for interest rates is most important to gold. Weaker than expected non farm payrolls surprisingly didn't give gold a boost overnight given its correlations to interest rate expectations. Some market observers suggesting that near term data may be disregarded given its delay in release during the government shutdown.

- Gold is up +0.50% today to US$4.323.68 and is now just under 1% below the October high of US$4,356.

- Moves higher today take gold into overbought territory where it spent much of September and October when trade war fears were at their peak. However if the idea that gold may be impacted less than normal by US data holds true, then growing geo-political risks and equity volatility could mean that the risk is that gold could remain overbought for some time.

INR: USD/INR Slumps On Heavy Intervention, 91.00 May Be Short Term Peak

Spot USD/INR sits up from earlier lows (90.10), last 90.3540, still up 0.75% in rupee terms. Session highs rest at 91.08, before strong intervention drove the pair lower not long after the open. In terms of levels to be mindful of, the 20-day EMA is back around 89.93, while the 50-day is further south at 89.225. Recent highs rest just of 91.10. In the option space, 1 month implied vol is little changed at 4.48%, while the 1 month risk reversal is down a touch, but still close to recent highs, last 0.28.

- In the near term, the market may see moves above the 91.00 level in spot USD/INR as a near term top. However, we have had similar episodes throughout 2025, like through Sep/Oct, where the pair couldn't get above 88.80/90, before ultimately breaking higher.

- A more sustained rally in INR is likely to require clarity around US-India trade, as well as a better portfolio inflow backdrop, which could come in Q1 next year.

- Rtrs notes: "The intervention on Wednesday matched Reserve Bank of India's actions in October and November, when it stepped in aggressively on three occasions to disrupt persistent one-way moves in the rupee. Unlike previous episodes, when intervention occurred before the local market opened, dollar sales on Wednesday came shortly after onshore trading began, said a banker, who requested anonymity as he is not authorized to speak to the media."

CHINA: More of the Same for Policy in 2026

- An article in the China Securities Journal assess policy in 2025 describing it as 'supportive' suggesting that since the beginning of the year various policy tools have worked together to guide financial institutions to increase their support for the real economy, whilst 'anchoring the goal of stable financial markets.

- Looking at the potential for policy in 2026, the article points to more of the same with the continuation of the current 'moderately loose' monetary policy, adhere to precise policy implementation whilst using flexible tools like RRR cuts and interest rate cuts to promote overall social financing costs.

- On social financing costs, the article points to overall social financing costs being at historical lows with lower loan interest rates thanks to cuts in the 7-day reverse repo rate, whilst lower housing provident fund loan rates are lower also. The weighted average interest rates for new corporate loans was 30bps lower than a year ago.

- The recent Central Economic Work Conference clearly stated that various policy tools, such as reserve requirement ratio (RRR) cuts and interest rate cuts, will be used flexibly and efficiently in what appears to leave room for further RRR and interest rate cuts in 2026.

- The focus on financing costs and banks willingness to lend will support the government's goal of improving domestic demand and target innovative industries viewed as important to the future development of the economy.

- It appears from this article that there is no imminent change to come, rather more of the same as the economy remains on track to achieve the 5% GDP growth target.

- Instead, it appears now that the already 'supportive' policy provides a backstop and could be altered if needed.

- Going forward we continue to monitor social financing costs and lending data as a key insight for future direction of policy.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 17/12/2025 | 0700/0700 | *** | Producer Prices | |

| 17/12/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 17/12/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 17/12/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final | |

| 17/12/2025 | 1000/1100 | *** | EZ HICP Final (2dp) | |

| 17/12/2025 | 1100/1100 | ** | CBI Industrial Trends | |

| 17/12/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 17/12/2025 | 1315/0815 | Fed Governor Christopher Waller | ||

| 17/12/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/12/2025 | 1405/0905 | New York Fed's John Williams | ||

| 17/12/2025 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 17/12/2025 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 17/12/2025 | 1730/1230 | Atlanta Fed's Raphael Bostic | ||

| 17/12/2025 | 1800/1300 | ** | US Treasury Auction Result for 20 Year Bond | |

| 18/12/2025 | 2145/1045 | *** | GDP | |

| 18/12/2025 | - | European Central Bank Meeting | ||

| 18/12/2025 | - | NorgesBank Meeting | ||

| 18/12/2025 | - | Bank of Japan Meeting | ||

| 18/12/2025 | - | Riksbank Meeting | ||

| 18/12/2025 | 0745/0845 | ** | Manufacturing Sentiment | |

| 18/12/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 18/12/2025 | 0900/1000 | *** | Norges Bank Rate Decision | |

| 18/12/2025 | 1000/1100 | ** | EZ Construction Output | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Deposit Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Main Refi Rate | |

| 18/12/2025 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 18/12/2025 | 1330/0830 | *** | Jobless Claims | |

| 18/12/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 18/12/2025 | 1330/0830 | * | Payroll employment | |

| 18/12/2025 | 1330/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1330/0830 | *** | CPI | |

| 18/12/2025 | 1345/1445 | ECB Press Conference |