JAPAN DATA: Export Pick Up Consistent With Broader Asia Trends, Aided By Chips

Japan Nov trade data was slightly better than forecast. Exports rose 6.1%y/y (5.0% projected and 3.6% prior), while imports were +1.3%y/y (against a 3.0% forecast). This saw the trade surplus print at ¥322.3bn, against a ¥72.6bn forecast and -¥226.1bn prior outcome. In seasonally adjusted terms the surplus was ¥62.9bn, also well above market forecasts. The pick up in export growth will be welcome by the authorities/BOJ, with concerns earlier in the year higher US tariff levels would weigh on external demand.

- The improvement in Japan export growth is consistent with other export orientated Asian economies, with growth ticking up into year end. Taiwan remains the standout though.

- Japan exports were firmer to the US, up 8.8%y/y (from -3.1%y/y prior), while to the EU posted a 19.6%y/y rise (exports to China fell 2.4%y/y). Automobile exports to the U.S. increased 1.5%, rebounding from a 7.5% decline in October. Aggregate chip exports were firm at 13%, after a 15.8% rise in Oct.

- In volume terms exports to the US were up 14%y/y, to the EU 16%y/y, but negative to China and Asia.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JAPAN DATA: Q3 GDP Contracts, But Resilient Detail, Particularly Business Spend

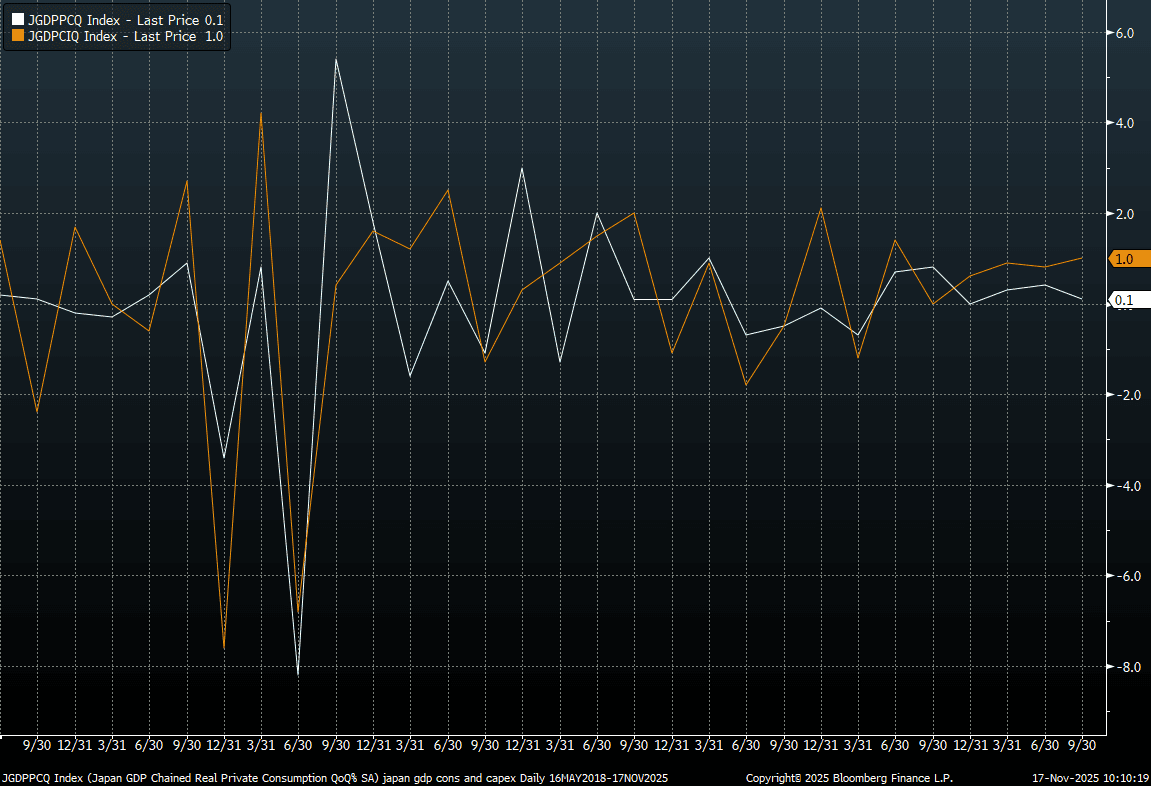

Q3 GDP (preliminary) in Japan was negative q/q, but not as much as the market forecast, thanks to upbeat business spending (+1.0%q/q versus -0.1% forecast). This was the first GDP decline since Q1 2024, but the detail paints a resilient underlying economic backdrop and comes ahead of fresh fiscal stimulus from the new Takaichi government. Today's GDP data should add some confidence, at the margins, the BOJ has in the GDP backdrop (particularly in terms of the drivers). We await Ueda's early Dec speech for details around hike timing.

- The q/q outcome for GDP was -0.4% against a -0.6% forecast. Note Q2 growth was revised to +0.6% from 0.5% originally reported. In annualized terms, growth -1.8%q/q, versus -2.4% forecast and a revised 2.3% gain in Q2. Note business s[ending was also revised up in Q2 to 0.8% from 0.6%q/q. Other components of GDP were close to forecasts, consumption up 0.1%q/q, while inventories were a -0.2ppt drag and net exports also trimmed -0.2ppt off growth.

- Whilst this is just a preliminary GDP print, the detail should be welcomed by the authorities. The q/q trends for private consumption (the white line) and business spending are plotted in the chart below.

- The resilience to strength in business spending, in particular, will be welcome. Via our Tokyo policy team: Private consumption and capital investment, the major components of the economy, are likely to firm in or after the fourth quarter, the official said. Private consumption, particularly non-durable goods, was hit by high prices and scorching weather in Q3, but is undergoing a moderate recovery supported by improving consumer sentiment, the official added.

- This also comes ahead of fresh fiscal stimulus, via BBG: "The Finance Ministry plans an economic package worth about ¥17 trillion ($110 billion), the Nikkei reported on Saturday, without identifying its sources. The supplementary budget to fund the spending is expected to reach about ¥14 trillion, exceeding last year’s ¥13.9 trillion compiled under former Prime Minister Shigeru Ishiba, the report said." - BBG

Fig 1: Japan GDP Components, Q/Q (Consumption (White Line) & Business Spending (Orange Line)

Source: Bloomberg Finance L.P./MNI

CRYPTO: Ethereum - Support Toward $2700 Approaches, Fade Bounces Toward $4000

Ethereum had a range over the weekend of $3025.15 - $3247.15, Asia is trading around $3100, +1.00%. Ethereum has traded under pressure over the weekend, it gapped lower on the Asian open testing the $3000 area before finding some demand. There are lots of commentators saying this will be the low, but in my experience when you have a leveraged asset class it tends to squeeze out weaker hands and inflict maximum pain before it finds a base again. Technically it now looks to be in a short-term bear market and I think rallies could potentially now be faded, the perfect sell-zone is toward the $3800-$4100 area, where I suspect sellers will return if given the chance. Ethereum has had a deep pullback almost 40% off its highs seen August, so at some point I think it should again offer value, technically the support comes in initially around $2600-$2800, then more big support toward the $2000-$2200 area.

Fig 1: Ethereum spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: Westpac Edges Down Q4 Inflation F/C, RBNZ Pricing Still For Nov Cut

Earlier monthly price data for Oct has seen Westpac revise down its Q4 inflation forecast, see below for more detail. Food prices fell 0.3%m/m, after falling 0.4% in Sep. This bought the y/y pace to 4.7%, up from Sep's 4.1% pace, but we have stabilized under 5% in recent months. Westpac cites softer travel and rental for its forecast revision. Note that on Wednesday this week we get Q3 PPI, although this tends not to shift market thinking too much. Note that Q4 CPI in NZ prints on Jan 23 next year.

Westpac: "We’ve revised our forecast for December quarter inflation to +0.3% and +2.8% for the year to December. Those estimates are both down 0.1ppts from our earlier forecast. Our updated forecast reflects information from Stats NZ’s monthly selected prices update. That update showed greater than expected softness in travel costs, which can be volatile on a month-to-month basis and will warrant close attention over the coming months. However, we also saw softness in other areas. Most notably, rental inflation has been very weak. Our updated forecast is close to the RBNZ’s last published forecast from their August MPS for a 0.3% quarterly rise, and 2.7% annual inflation. "

- Note, RBNZ dated OIS pricing is little changed across meetings, post this morning's data (we also had the services PMI, which rose but remain sub 50). 25bps of easing is priced for November, with a cumulative 34bps by February 2026.