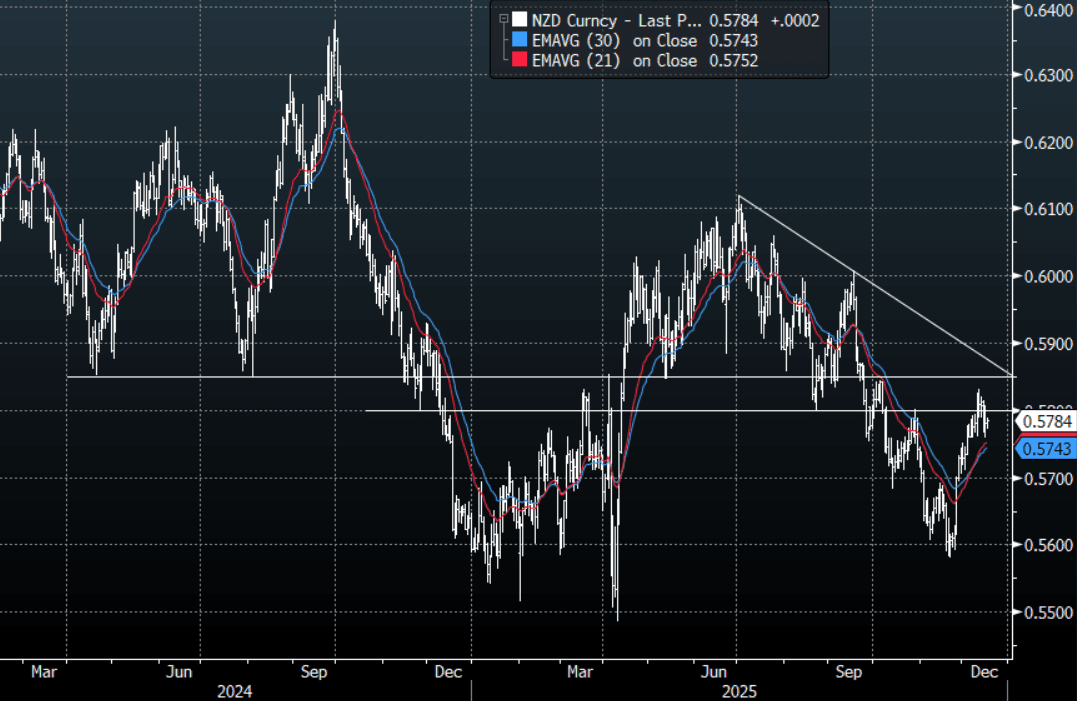

NZD: NZD/USD - Unchanged, Consolidating Above 0.5750

The NZD/USD had a range today of 0.5771-0.5789 in the Asia-Pac session, going into the London open trading around {NZD Curncy}. The NZD traded sideways in a quiet session, consolidating its gains above 0.5700-0.5750. On the day, I suspect this sort of price action could continue as the pair settles into a range, support is back toward 0.5740-0.5760 and resistance is around 0.5810-30.

- MNI AU - Q3 Current Account Deficit, As % Of GDP, Continues Improvement: The Q3 headline current account deficit widened to -NZD8.365bn, from, -NZD1.297bn in Q2, but this is part of the typical seasonal norms. In seasonally adjusted terms we were slightly wider in Q3 at -NZD3.8bn. As a percent of GDP, the deficit was -3.5% in YTD terms, slightly wider than the -3.4% forecast but still an improvement on the Q2 outcome of -3.7%. The deficit trend as a share of GDP continues to improve, we were at -9.0% of GDP at the end of 2022.

- MNI AU - Further Weakness In Whole Milk Prices, Back To Mid 2024 Levels: Overnight the GDT whole milk auction price fell sharply, down 5.7% on the prior outcome to $3161/mt. This is the lowest level since mid 2024 for the twice monthly auction outcome. The Q3 official terms of trade print for NZ showed a 2.1%q/q fall. We were still up 7.2% in y/y terms. Export prices are moving off earlier 2025 highs, consistent with lower whole milk auction price outcomes.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5780(NZD344m), 0.5800(NZD502m), 0.5850(NZD328m). Upcoming Close Strikes : 0.5630(NZD594m Dec 19), 0.5690(NZD531m Dec 18 ), 0.5860(NZD471m Dec 18 ) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 42 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Little Changed, Focus On Upcoming Data & Nvidia Results

TYZ5 is trading at 112-17+, +0-00+ from closing levels in today's Asia-Pac session.

- Cash US tsys are 1bp richer to 1bp cheaper, with a steepening bias, in today's Asia-Pac session. On Friday, US tsys finished showing a modest bear-steeper, with benchmark yields 1-4bps higher.

- US equity futures are slightly firmer in today's Asia session. The S&P looked to be rolling over again on Friday night, down almost 1.5% before it found solid demand during the N/Y session and pared back all the day's losses.

- The market will be looking toward the release of some US data this week (September's delayed nonfarm payrolls report for next Thursday) to get a gauge on things and also heavily focused on the upcoming Nvidia results, which will heavily impact the direction of markets this week.

- Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

- Along with the newly-rescheduled data, this week's calendar includes the October FOMC minutes (we're watching for colour on the debate over whether to ease any further) and flash November PMI data.

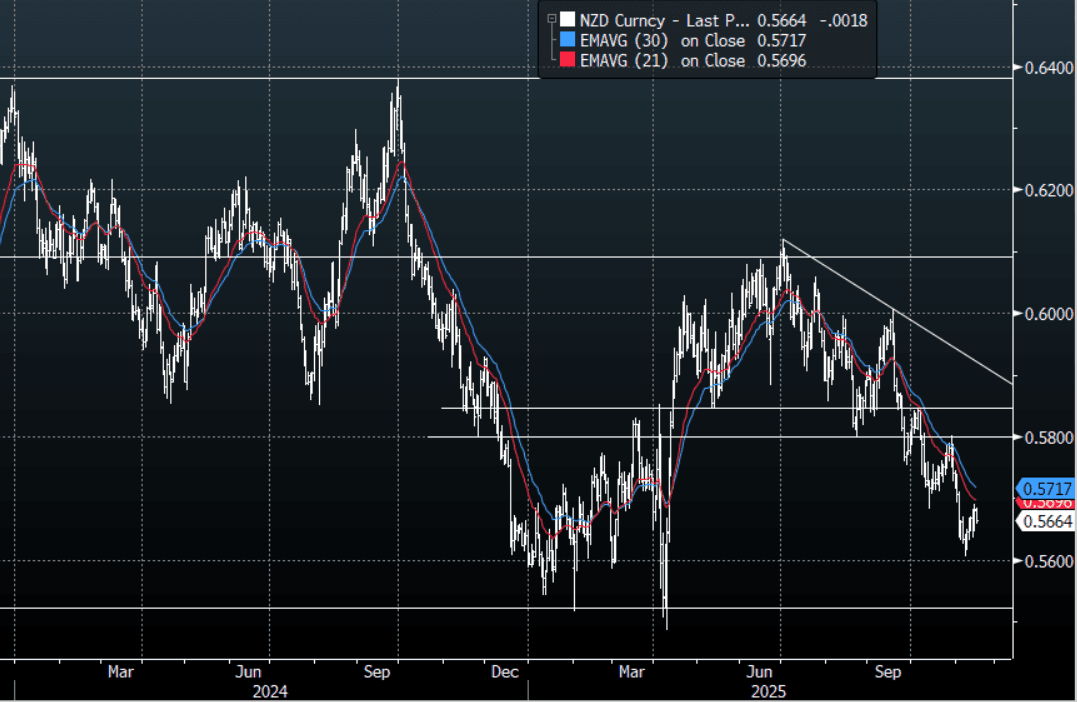

NZD: Asia-Pac: NZD/USD Drifts Back Toward 0.5650 Area

The NZD/USD had a range today of 0.5658 - 0.5681 in the Asia-Pac session, going into the London open trading around 0.5665, -0.30%. The NZD/USD has drifted lower in our session being led by the move higher in USD/Asia. The NZD is one of those currencies in which positioning can become an issue because of the size of the market so when it grinds higher like it did at the back of last week while risk turned lower it is price action worth noting. The place to fade NZD again is closer toward 0.5800 should we see that area again.

- Bloomberg reports: “Nomura Likes Long NZD/USD on Expectation RBNZ Will Hold Rates. The Reserve Bank of New Zealand will refrain from lowering borrowing costs at its meeting on Nov. 26, even though the market is pricing in a reduction, according to Nomura strategists. “The market has been pricing in too aggressive an easing path for the RBNZ,” they wrote in a Friday note. “The RBNZ has hinted that it sees the activity outlook as having bottomed and that prior easing will start to have a more positive impact on economic momentum.”

- MNI AU - Oct Services PMI Up But Still Sub 50, Pointing To Tepid Recovery: The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remained under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior. The outcome doesn't point to a sharp turn higher in early Q4 economic momentum. BNZ noted (via BBG): "Sector continues to struggle for forward momentum with the sub-component gauges all below long-term averages and making for "dreary reading".

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5675(NZD300m Nov 20), 0.5730(NZD434m Nov 19), 0.5835(NZD300m Nov19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 35 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends, Japan Down On China Concerns, Philippines Rebounds

Asia Pac stocks are mixed so far in Monday trade. Japan and China stocks sit weaker, while South Korea and Taiwan are higher. In South East Asia, the Philippines is the standout up over 3% (after making fresh multi year lows in recent dealings). US equity futures are tracking higher, led by Nasdaq futures, up close to 0.70% (Eminis are around +0.45% firmer). Focus is on crypto for broader risk trends, with Bitcoin up +1.65% so far today and likely aiding the US equity futures moves.

- Japan stocks are down modestly, the NKY off around 0.35%, while the Topix is off by 0.55% at the time of writing. The NKY is still above 50k at this stage. Near term focus is on China-Japan tensions. This is weighing on tourism and retail related stocks, which benefit from China visitors. Via BBG: "Yuyuantantian, a social media account linked to China’s state broadcaster and frequently used to signal official policy, published a commentary this weekend warning that Beijing “has made full preparations for substantive retaliation.” This comes after new Japan PM Takaichi made comments regarding Taiwan recently. Q3 GDP in Japan printed above expectations, but still fell in the quarter. The underlying resilience of business spending will be welcome though.

- Hong Kong's market is softer, the HSI down 0.80%, while HSTECH is down 1.2%, and looking poorer from a technical standpoint. The CSI 300 on the Mainland is off close to 0.70%.

- South Korea's Kospi is up over 1.6%, with dips supported near 4000. The Taiex is up around 0.60%. Last Friday saw close to $2bn in outflows from both markets by offshore investors. Today's better risk tone in US equity futures may be helping at the margin.

- The Philippines bourse is up a little over 3%, putting the index back to 5750/55. On Friday the index did make fresh lows back to 2020, so may be seeing some dip buyers emerge. Domestic fundamentals remain focused on fallout from the corruption scandal. From the weekend and via BBG: " More than half a million people took part in a rally organized by an influential church in Manila, calling for accountability in the Philippine government over a widening corruption scandal."