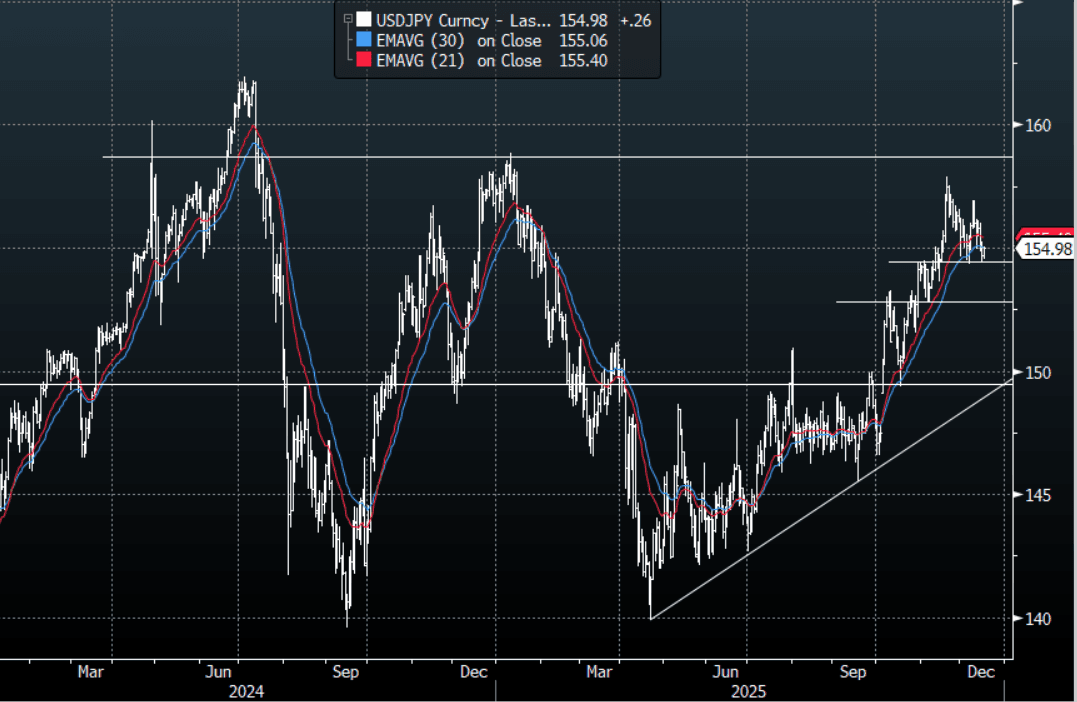

JPY: USD/JPY - Chops Around Above 154.50

The USD/JPY range today has been 154.52 - 155.03 in the Asia-Pac session, it is currently trading around {USDJPY Curncy}. The pair chopped around in a 50 point range without really going anywhere in Asia. The market is pricing in a hike by the BOJ for this week, for the time being this is keeping the JPY contained and confined to a wider 154.00-157.00 range having capped its upward momentum. Technically USD/JPY is in an uptrend, the first big support is back toward the 152.50-154.50 area. In today's Asian session, look for resistance back toward the 155.00-155.30 area initially, should this hold look for a retest of the 154.30-50 area at some point a break of which could signal a deeper pullback. A break above 155.20-30 and the price could move back toward 155.70-156.00.

- MNI AU - MNI BOJ Preview: Hike Fully Priced For This Week: Executive Summary The BOJ is widely expected to raise the policy rate by 25bp to 0.75% at the December 18-19 meeting, with Governor Ueda's recent remarks signaling increased confidence in the outlook for growth, inflation and wage momentum. Ueda has indicated the BOJ will assess the "pros and cons of raising the policy interest rate," while Policy Board members say conditions for a hike are "gradually falling into place," though confirmation of spring wage momentum remains key.

- Beyond December, attention will focus on guidance around the neutral rate, which Ueda has described as "1-2.5%," signaling that policy normalisation is likely to continue gradually rather than end at 1%.

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.75($950m), 156.00($760m). Upcoming Close Strikes : 157.00($4.15b Dec 18 ), 158.00($4.98b Dec 18 ), 159.00($6.46b Dec 18 ) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 101 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Mixed Trends, Japan Down On China Concerns, Philippines Rebounds

Asia Pac stocks are mixed so far in Monday trade. Japan and China stocks sit weaker, while South Korea and Taiwan are higher. In South East Asia, the Philippines is the standout up over 3% (after making fresh multi year lows in recent dealings). US equity futures are tracking higher, led by Nasdaq futures, up close to 0.70% (Eminis are around +0.45% firmer). Focus is on crypto for broader risk trends, with Bitcoin up +1.65% so far today and likely aiding the US equity futures moves.

- Japan stocks are down modestly, the NKY off around 0.35%, while the Topix is off by 0.55% at the time of writing. The NKY is still above 50k at this stage. Near term focus is on China-Japan tensions. This is weighing on tourism and retail related stocks, which benefit from China visitors. Via BBG: "Yuyuantantian, a social media account linked to China’s state broadcaster and frequently used to signal official policy, published a commentary this weekend warning that Beijing “has made full preparations for substantive retaliation.” This comes after new Japan PM Takaichi made comments regarding Taiwan recently. Q3 GDP in Japan printed above expectations, but still fell in the quarter. The underlying resilience of business spending will be welcome though.

- Hong Kong's market is softer, the HSI down 0.80%, while HSTECH is down 1.2%, and looking poorer from a technical standpoint. The CSI 300 on the Mainland is off close to 0.70%.

- South Korea's Kospi is up over 1.6%, with dips supported near 4000. The Taiex is up around 0.60%. Last Friday saw close to $2bn in outflows from both markets by offshore investors. Today's better risk tone in US equity futures may be helping at the margin.

- The Philippines bourse is up a little over 3%, putting the index back to 5750/55. On Friday the index did make fresh lows back to 2020, so may be seeing some dip buyers emerge. Domestic fundamentals remain focused on fallout from the corruption scandal. From the weekend and via BBG: " More than half a million people took part in a rally organized by an influential church in Manila, calling for accountability in the Philippine government over a widening corruption scandal."

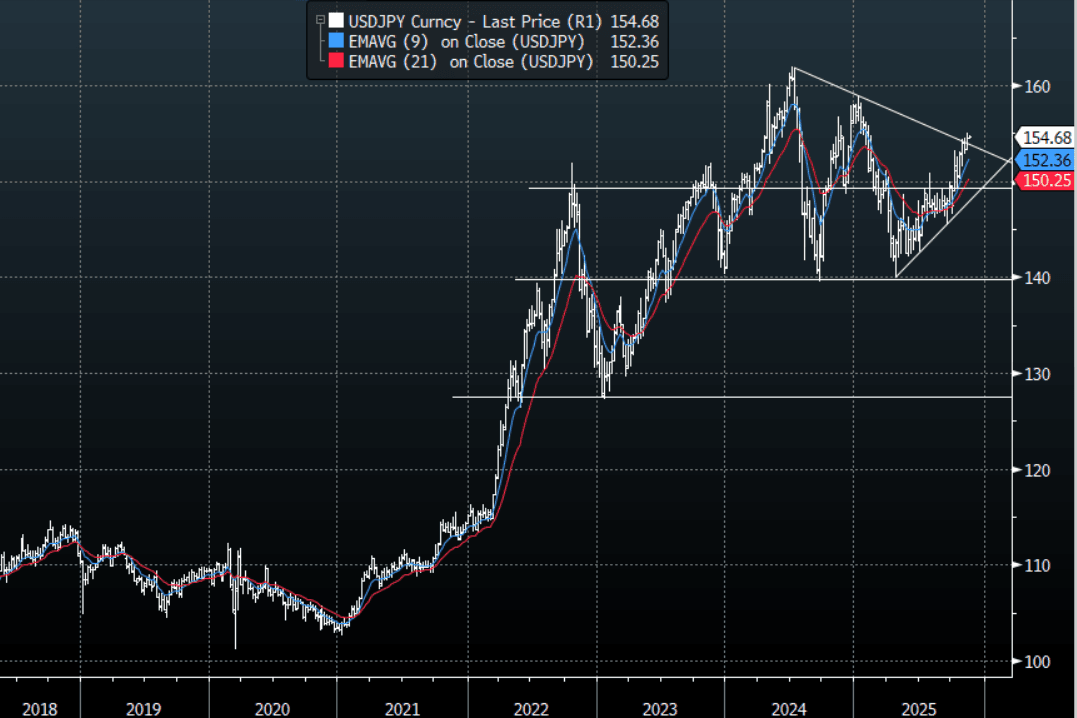

JPY: Asia-Pac: USD/JPY Looking To Mount Another Challenge Of 155.00

The USD/JPY range today has been 154.42 - 154.79 in the Asia-Pac session, it is currently trading around 154.70, +0.10%. The pair has traded better bid together with USD/Asia across the board in the Asian session. Usd/Jpy seems to remain well supported on dips as the market remains wary of the new leadership policies and a US December rate cut comes into doubt. The price action points to a renewed challenge to the resistance toward 155.00, a sustained break above here and it could start to pick up momentum to the topside again potentially targeting another push toward 160.

- "Japan Plans Bigger Extra Budget This Fiscal Year”: Media Reports. "The Finance Ministry plans an economic package worth about ¥17 trillion ($110 billion), the Nikkei reported on Saturday, without identifying its sources. The supplementary budget to fund the spending is expected to reach about ¥14 trillion, exceeding last year’s ¥13.9 trillion compiled under former Prime Minister Shigeru Ishiba, the report said." - BBG

- "JAPAN ECONOMY MINISTER KIUCHI ON JULY-SEPT GDP: NO CHANGE TO OUR VIEW ECONOMY GRADUALLY RECOVERING, WILL COMPILE ECONOMIC STIMULUS PLAN SWIFTLY" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.39b), 154.70($400m). Upcoming Close Strikes : 155.00($1.31b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 85 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Modestly Cheaper Ahead Of Tomorrow's RBA Minutes & Wed's WPI

ACGBs (YM -2.5 & XM -4.0) are weaker on a data-light session.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +33bps.

- The bills strip is -2 to -3 across contracts.

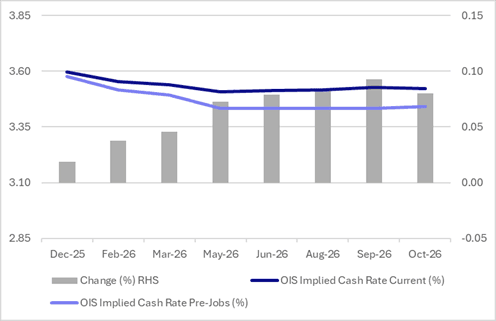

- Interest rate expectations in Australia out to mid-2026 have firmed just shy of 10bps over the past week. The key driver of this move was October’s employment data. The labour market normalised, with unemployment returning to 4.3% after September’s 4.5% spike. OIS pricing implies just a 1% probability of a 25bp December cut (9% pre-data), with cumulative easing of 9bps priced by mid-2026 (down from 17bps pre-data). (see chart)

- Even still, as previously noted, markets may still be overestimating the likelihood of further cuts, given that rising annual inflation has historically ended RBA easing cycles.

- Tomorrow, the local calendar will see RBA Minutes of the Nov. Policy Meeting ahead of the Wage Price Index on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-Jobs

Source: Bloomberg Finance LP / MNI